做过的题你都能拿分吗?

临近考试,小编相信大家都开始启用“题海”战术,疯狂刷题,可是你现在做过的题,你考场碰到都能做对吗?

同为备考党的我,小编只想说,如果只做过一遍,那怕是有点难。

我相信大家都是从题海战术里走出来的朋友们,这其实就是一个熟能生巧的事情,即时可能你对某个知识点不理解,但是同一个题型你做完3次后,就有一种闭着眼睛我都能认出你的熟悉感,剥掉题干的外壳,其实都是同一个套路。

那么到底哪些题目是有典型考法的,哪些知识点是比较易错的点,这就是大家考前需要拿个小本本记下来的事情。

看到这里,是不是大家都有一种蠢蠢欲动,要赶紧去做笔记的想法?

知道目前大家都在争分多秒学习,贴心的品职教研组的小哥哥、小姐姐们也是熬夜赶工(心疼一下),帮大家整理了CFA三个级别学科的错题本,希望在最后的时候能给大家起到助力的作用。

在接下来的几周里,我们会陆续发放三个级别的高频问答,希望对大家的备考有所帮助。今天二级放上权益的错题本,大家一起来看看这些题都会做吗?

精选问答1

题干

Jacques prepares to update the valuation of TMT. The company’s expected ROE in 2017 is 34.5% but it is assumed that the firm’s ROE will slowly decline towards the cost of equity thereafter.

As of the beginning of 2015, based upon the information in the below table, use the multistage-stage residual income (RI) model to determine the intrinsic value of the equity of TMT. The intrinsic value per share is closest to:

A 22.72.

B 14.97.

C 78.81.

答案解析

B is correct.

解题思路

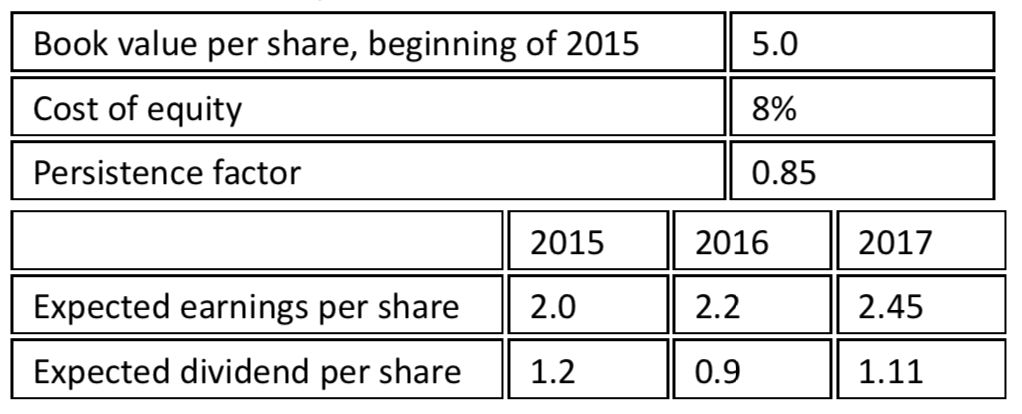

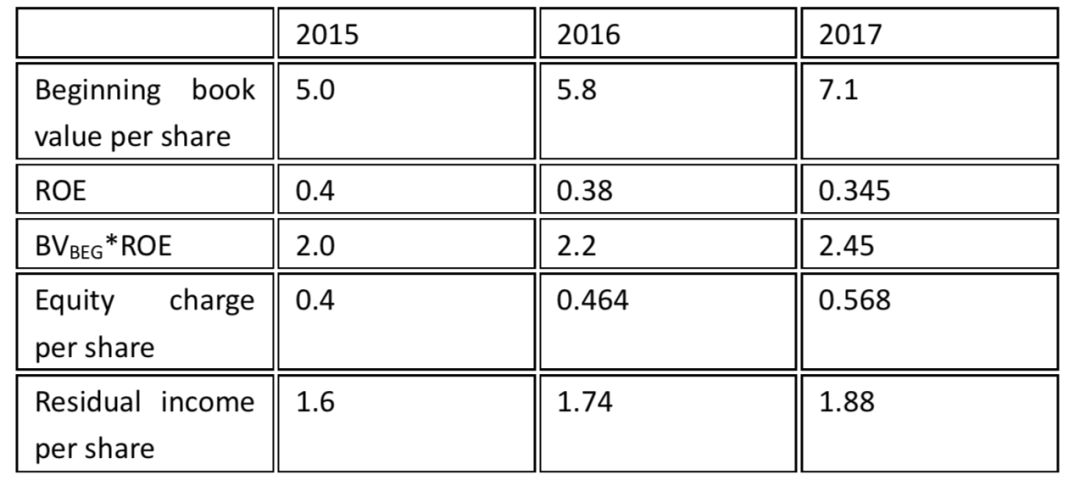

第一步是计算2015 - 2017年的每股剩余收益:

第二步是计算终值:

PV of Terminal Value 2017=RI2017*w/(1+r-w)=1.88*0.85/(1+0.08-0.85)=6.947

第三步计算每股内在价值:

V0=5+1.6/(1.080)+1.74/(1.08)2+(1.88+6.947)/(1.08)3=14.97

易错点分析

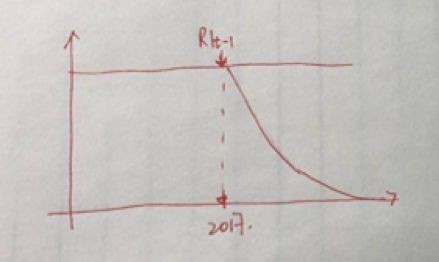

这道题提问的同学相当多,主要的问题在于不清楚RI的第二阶段从哪里开始,也就是这一刀究竟应该切在哪里。题干说ROE will slowly decline towards the cost of equity thereafter。关键词在于“thereafter”,这说明RI是从2017年之后也就是2018年开始下降的,所以这一刀应该切在2017年末,如下图所示:

精选问答2

题干

Jacques is the portfolio manager of AB pension and she recently consider adding PZ Inc. (NewYork Stock Exchange: PZ) to its portfolio. After carefully considering the characteristics of the company and its competitors, she believes the company’s growth rate declines linearly from 12 percent in the first year to 6 percent in the fifth.

PZ’s total dividends paid on 2017 was $0.22.The estimated that the required return is 9 percent. What is the intrinsic value of the stock?

A $10.32.

B $15.40.

C $8.65.

解题思路

C is correct.

解题思路

根据题干信息我们可以使用H模型来计算股票的内在价值,根据 H模型的公式,股票的内在价值为:

易错点分析

H模型的题都不难基本都是代入公式求解即可,但这道题提问很多,主要因为这道题关于增长率下降的说法与平时的题目有所不同,到底是下降了4年还是5年很多同学就弄不明白了。这确实是一个很好的问题。我们翻阅原版书后发现,H模型在原版书里的出题方式只有两种:

1、传统版:currently 14%,and is expected decline linearly during next8 years。

2、decline linearly from 14 percent in the first year to 7 percent inthe ninth. (原版书 22-27那个case)

而这两种计算虽然说法不同,但计算方式都是一样的(H=4),那我们可以来分析一下:这里看上去唯一的区别就是一个是未来下降了8年,另一个是从第一年开始下降,到第9年。第一个说法就不用分析了,直接看第二个。从第一年开始下降,到第9年。

其实这里的第一年应该是第一年初的意思,如果这样解释似乎一切就合理了,从第一年初下降到第9年初,所以一共下降的了8年,H=4。说回这道题也是一样,从第一年初下降到第五年初,那么下降了4年,因此H=2。

精选问答3

题干

An equity index is established in 2001 for a country that has relatively recently established a market economy. The index vendor constructed returns for the five years prior to 2001 based on theinitial group of companies constituting the index in 2001.

Over 2004 to 2006 aseries of military confrontations concerning a disputed border disrupted the economy and financial markets. The dispute is conclusively arbitrated at the end of 2006. In total, ten years of equity market return history is available as of the beginning of 2007.

The geometric mean return relative to 10-year government bond returns over 10 years is 2 percent per year. The forward dividend yield on the index is 1 percent. Stock returns over 2004 to 2006 reflect the setbacks but economists predict the country will be on a path of a4 percent real GDP growth rate by 2009.

Earnings in the public corporate sectorare expected to grow at a 5percent per year real growth rate. Consistent with that, the market P/E ratio is expected to grow at 1 percent per year.

Although inflation is currently high at 6 percent per year, the long-term forecast is for an inflation rate of 4 percent per year. Although the yield curve has usually been upward sloping, currently the government yield curve is inverted;at the short-end, yields are 9 percent and at 10-year maturities, yields are 7percent.

In the current interest rate environment, using a required return estimate based on the short-term government bond rate and a historical equity risk premium defined in terms of a short-term government bond rate would be expected to:

A bias long-term required return on equity estimates upwards.

B bias long-term required return on equitye stimates downwards.

C have no effect on long-term required return on equity estimates.

答案解析

A is correct.

解题思路

题目要我们基于当前短期国债利率和历史股本风险溢价来估计股东的要求回报率:

根据CAPM的公式:re=rf+beta(rm-rf) 可以看出股东的要求回报率由两个部分组成

![]() 第一部分rf:无风险利率题干要我们基于当前的短期利率,由于当前的短期利率大于长期利率(current yield curve is inverted收益率曲线向下倾斜),因此第一项比较大;

第一部分rf:无风险利率题干要我们基于当前的短期利率,由于当前的短期利率大于长期利率(current yield curve is inverted收益率曲线向下倾斜),因此第一项比较大;

![]() 第二部分ERP:ERP中的无风险利率题目让我们用历史上的短期利率来估计,历史的收益率曲线是向上倾斜(短期低,长期高),因此历史上的短期利率比较小,那么ERP=RM-RF就比较大。因此第二项也比较大。

第二部分ERP:ERP中的无风险利率题目让我们用历史上的短期利率来估计,历史的收益率曲线是向上倾斜(短期低,长期高),因此历史上的短期利率比较小,那么ERP=RM-RF就比较大。因此第二项也比较大。

汇总在一起两项都大,那么计算得到的re也就偏高。

选项中long-term required return on equity:因为在美国股权投资都是长期投资,那么股东的要求回报率也是长期的。因此选A。

易错点分析

这道题比较容易错的地方在于CAPM公式中有两个无风险利率RF,而这道题对两个RF又分别进行了定义,一个用历史数据,一个用当前的数据。

这样还没完,它的利率并没有直接给出而是告诉了我们利率曲线的形状,我们需要根据形状来判断RF的高低,其中很多同学不明白“inverted”是利率曲线向下倾斜的意思。再加上题干本身英文表达也很绕,所以这道题被问到的频率相当高。

精选问答4

题干

A supply side estimate of the equity risk premium as presented by The Ibbotson Chen earnings model is closest to:

A 3.2 percent.

B 4.0 percent.

C 4.3 percent.

答案解析

C is correct.

解题思路

根据supply side模型 , 股权风险溢价等于= {[(1 + EINFL)(1 + EGREPS)(1 + EGPE) − 1.0] + EINC}−Expected risk-free return

![]() EINFL = 4 percent per year (long-term forecast of inflation)

EINFL = 4 percent per year (long-term forecast of inflation)

![]() EGREPS = 5 percent per year (growth in realearnings)

EGREPS = 5 percent per year (growth in realearnings)

![]() EGPE = 1 percent per year (growth in market P/E ratio)

EGPE = 1 percent per year (growth in market P/E ratio)

![]() EINC = 1 percent per year (dividend yield or the income portion)

EINC = 1 percent per year (dividend yield or the income portion)

![]() Risk-free return = 7 percent per year (for10-year maturities)

Risk-free return = 7 percent per year (for10-year maturities)

带入公式, 我们可以得到:{[(1.04)(1.05)(1.01) − 1.0] + 0.01} − 0.07 = 0.113 − 0.07 = 0.043or 4.3 percent.

易错点分析

这道题计算本身不难,但提问的人数不少主要是因为几个数据的选择问题:

![]() 预期的真实的GDP增长率为何不用4%?

预期的真实的GDP增长率为何不用4%?

题干说预估的经济增长是on a path of a 4 percent real GDP growth rateby 2009。这句话的意思说明2009年经济增长才达到4%,并不是一个长期预测值。但题目明确给了公司未来real growth rate为5%,因此用5%。

![]() 为何real GDP增长率可以用公司realearning的增长率来代替?

为何real GDP增长率可以用公司realearning的增长率来代替?

在成熟的发达国家市场,整个国家的realGDP增长就等于全体公司real earning的增长,这两个指标是可以互换使用的。原版书也有相同的描述:Expected growth in real earnings per share. This quantity should approximately track the real GDP growth rate.

![]() rf为什么取长期国债的利率?

rf为什么取长期国债的利率?

我们现在估计的是股票市场的风险溢价,股票是一种长期投资产品,因此我们要用长期的数据对它进行估计。

精选问答5

题干

Statement 3: The Fed model concludes that the market is undervalued when the market’s current earnings yield is greater than the 10-year Treasury bond yield.

Statement 4: The Yardeni model includes the consensus five-year earnings growth rate forecast for the market index.

Which of Silveira’s statements concerning the Fed and Yardeni models is correct?

选项A:Statement 3 only

选项B:Statement 4 only

选项C:Both Statement 3 and Statement 4

答案解析

C is correct

解题思路

首先,这两个模型都是在帮助我们判断整个股票市场是被高估还是低估。然后我们分别来看:

Yardeni 模型是基于戈登增长模型推导出来的旨在用来判断整个股票市场是被高估还是被低估,它并不是股票市场收益率的计算公式。这个模型是假设当股票市场的定价处于合理水平时该等式成立。

CEY = CBY – b× LTEG + Residual

CEY:当前市场指数的收益率

CBY:当前穆迪统计的A等级公司债的收益率

LTEG:市场指数5年盈利增长率的预测

系数b:平滑系数

如果我们把市场上的数据(CEY\CBY..)带入该模型发现等式不成立,那么我们就可以据此做出买入或卖出的建议。(公式每一项了解即可,不需要掌握原理)

FED模型比Yardeni 模型还简单,他是假设如果股票是被合理估值的那么它收益率就应该等于长期国债的收益率。如果发现等式不相等就可以据此做出买入或卖出的建议。当市场收益率大于长期国债的收益率,说明当前股票市场被低估了。

易错点分析

这道题大家做不对是可以理解的,这两个模型都是3级重要考点,在二级属于非常偏门的知识点,所以咱们讲义就没有收录进去,但近年协会出题也越来越不按常理出牌。再加上很多同学都有疑问,小编就借此机会把这两个模型简单介绍一下,也算对现有课程的一个补充。

配图来源网络