做过的题你都能拿分吗?

临近考试,小编相信大家都开始启用“题海”战术,疯狂刷题,可是你现在做过的题,你考场碰到都能做对吗?

同为备考党的我,小编只想说,如果只做过一遍,那怕是有点难。

我相信大家都是从题海战术里走出来的朋友们,这其实就是一个熟能生巧的事情,即时可能你对某个知识点不理解,但是同一个题型你做完3次后,就有一种闭着眼睛我都能认出你的熟悉感,剥掉题干的外壳,其实都是同一个套路。

那么到底哪些题目是有典型考法的,哪些知识点是比较易错的点,这就是大家考前需要拿个小本本记下来的事情。

看到这里,是不是大家都有一种蠢蠢欲动,要赶紧去做笔记的想法?

知道目前大家都在争分多秒学习,贴心的品职教研组的小哥哥、小姐姐们也是熬夜赶工(心疼一下),帮大家整理了CFA三个级别学科的错题本,希望在最后的时候能给大家起到助力的作用。

在接下来的几周里,我们会陆续发放三个级别的高频问答,希望对大家的备考有所帮助。接下来小编就放上我们教研团队精心整理的CFA一级财务报表分析精选问答,希望对大家复习有所帮助哦!

精选问答1

题干

The gain or loss on a sale of a long-lived asset to which the revaluation model has been applied is most likely calculated using sales proceeds less:

A. carrying amount.

B.carrying amount adjusted for impairment.

C. historical cost net of accumulated depreciation.

答案解析

A is correct.

The gain or loss on the sale of long-livedassets is computed as the sales proceeds minus the carrying amount of the assetat the time of sale.

This is true under the cost and revaluation models ofreporting long-lived assets. In the absence of impairment losses, under the cost model, the carrying amount will equal historical cost net of accumulated depreciation.

解题思路

不管是revaluation model还是cost model,处置固定资产的gain/loss就等于处置资产的收入减去资产的账面价值,所以选A。Carrying value是账面价值,是扣掉了折旧和减值之后体现在资产负债表上的那个数,是一个净额的概念,因此不用再调整减值了,B不对。

而C选项的错误在于“historical cost”,题目说的是用revaluation model,revaluation model的账面价值是基于fair value的,所以应该是用fair value扣除折旧。延伸一下,这道题里所说的gain or loss是一个损益表的概念,如果题目考的是cash flow,处置固定资产所得现金流应该属于CFI,Cash flow直接就等于收到的现金。

易错点分析

这道题考点很简单,但是有些同学会问为什么不选B或者为什么不选C,他们是对carrying amount/carrying value这个概念有些混淆。一定要把carryingvalue、book value、historical cost、fair value等概念区分清楚。

Carrying value=book value,是扣除了折旧和减值金额后的净值,至于是基于historical cost扣除还是基于fair value扣除,取决于是cost model还是revaluation model。

精选问答2

题干

Zimt AG wrote down the value of its inventory in 2007 and reversed the write-down in 2008. Compared to the results the company would have reported if the write-down had never occurred, Zimt’s reported 2008:(assume the companies use a periodic inventory system)

A.profit was overstated.

B. cash flow from operations was overstated.

C. year-end inventory balance was overstated.

答案解析

A is correct.

The reversal of the write-down shifted costof sales from 2008 to 2007. The 2007 cost of sales was higher because of the write-down, and the 2008 cost of sales was lower because of the reversal of the write-down.

As a result, the reported 2008 profits were overstated. Inventorybalance in 2008 is the same because the write-down and reversal cancel each other out.

Cash flow from operations is not affected by the non-cash write-down, but the higher profits in 2008 likely resulted in higher taxes and thus lower cash flow from operations.

解题思路

这道题比较绕,题干中对比的对象是发生减值的情况和没有发生减值的情况。

![]() 情况1:2007年存货减值,2008年减值回转。

情况1:2007年存货减值,2008年减值回转。

![]() 情况2:2007年没有减值,那么2008年自然不会回转,也就是什么都没发生。

情况2:2007年没有减值,那么2008年自然不会回转,也就是什么都没发生。

题目问的是与情况2相比,情况1的2008年财报会怎么样。我们可以按照时间线看一下,情况1中,2007年Z公司对存货进行了减值,那么存货的账面价值会减少,同时要在损益表中体现出这个减值金额,会计准则规定存货减值要通过增加当期COGS体现在损益表中,所以2007年的存货账面价值减少,COGS增加,NI减少。

2008年减值回转,那么存货的账面价值上升,同样的,减值回转也要通过COGS体现在I/S中,也就是2008年的COGS变低,NI增加。A选项说profit高估,与情况2相比,情况1的2008年的NI确实更高,所以A正确。

B选项说CFO高估,这是不对的,因为存货跌价只是会计上的处理,并不会发生实际现金流的流出,所以不影响CFO。C选项说2008年末的存货账面价值高估了,实际上2007年减值,2008年回转,一减一增,最后的存货账面价值是跟发生减值之前一样的,所以并没有被高估。

易错点分析

![]() 首先要知道存货的减值是通过COGS影响损益表的,减值对公司来说是损失,所以COGS增加,NI减少。相反的,回转的话对公司来说是收益,所以COGS减少,NI增加。

首先要知道存货的减值是通过COGS影响损益表的,减值对公司来说是损失,所以COGS增加,NI减少。相反的,回转的话对公司来说是收益,所以COGS减少,NI增加。

![]() 其次,存货的减值会影响NI,但是不影响现金流,因为跌价只是降低了存货的账面价值,并没有真正的现金流出。

其次,存货的减值会影响NI,但是不影响现金流,因为跌价只是降低了存货的账面价值,并没有真正的现金流出。

![]() 做这种作比较类型的题目时,一定要注意审题,明确到底是谁跟谁比。

做这种作比较类型的题目时,一定要注意审题,明确到底是谁跟谁比。

精选问答3

题干

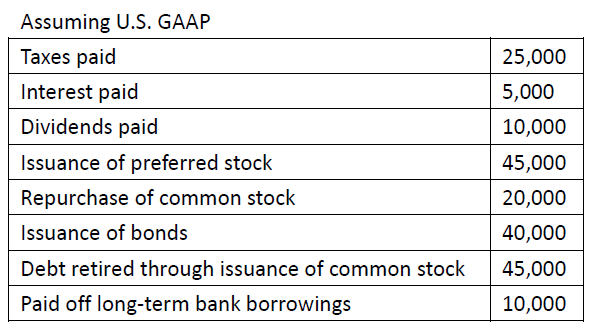

Cash flow from financing activities is:

A.$45,000.

B. $55,000.

C. $75,000.

答案解析

CFF=Issuance of preferred stock + issuance of bonds - principal payments on bank borrowings - repurchase of common stock -dividends paid = 45,000 + 40,000 - 10,000 - 20,000 - 10,000 = $45,000

解题思路

这道题考的是CFF的计算,题目难点在于很多同学不明白表格倒数第二行的“debt retired through issuance of common stock”是什么意思,这一项的业务是通过发行股票减少债务,类似于债转股、可转换优先股转换为普通股等,是没有现金流产生的,因此在计算CFF的时候不用考虑这一项。

计算CFF应该用CFF的流入减去CFF的流出,表格几项中,属于CFF的有Dividends paid 、Issuance of preferred stock、Repurchase of commonstock、issuance of bonds和Paid off long-term bank borrowings,其中发行优先股和发行债券都会有现金流的流入,而其余几项是现金流流出,直接相减即可得到答案。

易错点分析

![]() 计算很简单,主要是有一个比较陌生的名词容易让大家望而却步,可以通过这道题了解一下。

计算很简单,主要是有一个比较陌生的名词容易让大家望而却步,可以通过这道题了解一下。

![]() 其次就是要注意题目是under USGAAP,Dividends paid属于CFF,而taxes paid和interest paid属于CFO。

其次就是要注意题目是under USGAAP,Dividends paid属于CFF,而taxes paid和interest paid属于CFO。

精选问答4

题干

Inventory cost is least likely to include:

A. production-related storage costs.

B. costs incurred as a result of normal waste of materials.

C. transportation costs of shipping inventory to customers.

答案解析

C is correct.

Transportation costs incurred to shipinventory to customers are an expense and may not be capitalized in inventory.(Transportation costs incurred to bring inventory to the business location canbe capitalized in inventory.)

Storage costs required as part of production, aswell as costs incurred as a result of normal waste of materials, can becapitalized in inventory. (Costs incurred as a result of abnormal waste must be expensed.)

解题思路

为了使得存货达到可销售状态而花费的成本计为存货的成本,包括purchase cost,生产过程中的storage cost、normal waste等。达到销售状态之后花费的成本,属于period cost,包括abnormal costs,除production-related以外的storage cost,管理费用和销售费用等。如果是把货物运送到仓库,那么就是属于存货成本的一部分,但是把货物送到顾客手中的成本应该计为费用。

易错点分析

![]() 很多同学会忽略A选项中的“production-related”,如果只是产成品的储藏成本,那么应该计入当期费用,但是为了生产存货而必须发生的储藏成本是要计入存货的成本中的。

很多同学会忽略A选项中的“production-related”,如果只是产成品的储藏成本,那么应该计入当期费用,但是为了生产存货而必须发生的储藏成本是要计入存货的成本中的。

![]() 涉及到shipping cost的时候一定要看清是发生在哪个阶段,是把货物运送到仓库发生的成本还是把存货送给客户时发生的成本。

涉及到shipping cost的时候一定要看清是发生在哪个阶段,是把货物运送到仓库发生的成本还是把存货送给客户时发生的成本。

精选问答5

题干

If inventory unit costs are increasing from period-to-period, a LIFO liquidation is most likely to result in an increasein:

A. gross profit.

B. LIFO reserve.

C. inventory carrying amounts.

答案解析

A is correct.

When the number of units sold exceeds the number of units purchased, a company using LIFO will experience a LIFO liquidation.

If inventory unit costs have been rising from period-to-period anda LIFO liquidation occurs, it will produce an increase in gross profit as a result of the lower inventory carrying amounts of the liquidated units (lower cost per unit of the liquidated units).

解题思路

题目的意思是,当物价上涨的时候,如果有LIFO liquidation的现象会导致下列哪个增加。想要知道LIFO liquidation导致的结果,就要先了解LIFO liquidation的意思。

当物价上涨,使用LIFO时,后进来的存货先出去,所以COGS会更大,此时公司如果不希望COGS偏大,它就会购买少于销售量的存货,比如销售了100件存货,但只购入40件,这样一来,有60件的成本就按之前先购入的价格比较低的存货来计算,所以也叫“挖过去便宜的存货”,那么COGS就下降,gross profit增加,但是这种增加是不可持续的。

LIFO reserve是INVF -INVL,就是LIFO和FIFO两种不同方法计量下存货的差额。美国准则下允许FIFO和LIFO,但是国际准则不允许LIFO,那么为了方便报表使用者可以把不同公司进行比较,就要把使用LIFO公司的存货调整成FIFO,需要用LIFO reserve来调整。

使用LIFO liquidation把旧的存货都清算掉,公司的存货会减少,就会消除LIFO和FIFO不同方法下存货的差异,因此LIFO reserve会减少。

易错点分析

这道题并不是难题,很多人做错的原因还是因为LIFO liquidation的定义不够了解,只要知道LIFO liquidation是“挖以前便宜的存货”,题目就能做对。有的同学问如果是物价下降的情形会怎样,这也说明这位同学不知道LIFO liquidation是企业在干什么。使用LIFO方法的企业才能用LIFO liquidation,而且目的是做高利润,当市场物价下降时,LIFO本来COGS就低,没必要进行LIFO liquidation。

精选问答6

题干

Which of the following is most likely classified as a current liability?

A. Payment received for a product due to be delivered at least one year after the balance sheet date

B. Payments for merchandise due at least one year after the balance sheet date but still within a normal operating cycle

C. Payment on debt due in six months for which the company has the unconditional right to defer settlement for at least one year after the balance sheet date

答案解析

B is correct.

Payments due within one operating cycle ofthe business, even if they will be settled more than one year after the balance sheet date, are classified as current liabilities.

Payment received in advance of the delivery of a good or service creates an obligation or liability. If the obligation is to be fulfilled at least one year after the balance sheet date,it is recorded as a non-current liability, such as deferred revenue or deferred income.

Payments that the company has the unconditional right to defer for at least one year after the balance sheet may be classified as non-current liabilities.

解题思路

这道题考的是current liability的定义。

有的同学会问:“为什么不选C,长短期的界限不是一年么?”这一题考得比较细,通常来讲长短期是以一年为界限的,但有时需要看它的实质。比如虽然大于一年,但是还在一个经营周期内,这样的负债也算是current的,因为每个公司的性质不一样,有的公司的运营周期会比较长,可能会长于一年,比如造飞机或者轮船的公司,一个业务从接单、到交割、到最后收款要好几年。

再比如,有的负债期限虽然小于1年,但公司可以无条件的往后推迟偿还,那就应该算non-current的。

A选项说的是产品的交付周期超过一年的预收款,在没有其他说明条件的情况下,我们就以一年为界,所以A选项应该被划为non-currentliability。

B选项说负债期限虽然超过了一年,但是还在一个正常的经营周期内,这就是我们上面所说的情形,属于currentliability,所以B选项正确。

C 选项说的是负债虽然6个月就到期,但是公司有权无条件延期,这种情况的负债本质是non-current liability,所以C也不对。

易错点分析

这道题的AB选项都比较常规,C选项这种情形大家可能没见过,可以通过这道题了解一下。另外,碰到不熟悉的问题一定要多读几遍,揣摩出题人到底想考察什么,有时候选项也能给我们提示。

比如这道题,如果出题人只是想考current和non-current的分界是一年的话是不是太简单了,我们从三个选项的内容也能看出来这道题是想考current的实质,而不仅仅是通常的以一年为界限的一个理解。

精选问答7

题干

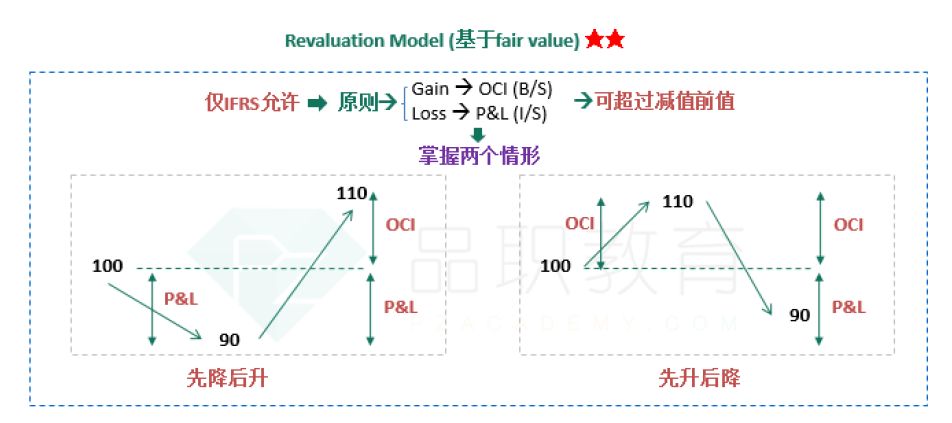

Under the revaluation model for property, plant, and equipment and the fair model for investment property:

A. fair value of the asset must be able to be measured reliably.

B. net income is affected by all changes in the fair value of the asset.

C. net income is never affected if the asset increases in value from its carrying amount.

答案解析

A is correct.

Under both the revaluation model forproperty, plant, and equipment and the fair model for investment property, the asset’s fair value must be able to be measured reliably.

Under the fair value model, net income is affected by all changes in the asset’s fair value.

Under the revaluation model, any increase in an asset’s value to the extent that it reverses a previous revaluation decrease will be recognized on the incomestatement and increase net income.

解题思路

这道题问的是revaluation model和fair value model的共同点。revaluation model是针对PP&E的,而fair value model是针对投资性房地产的,两者的适用对象不一样,但是共同点是都基于fair value入账。两者的区别还有对fair value涨跌的处理不同。

Revaluationmodel的基本原则是FV的上涨要计入OCI,FV的下跌计入I/S,但是如果是FV先降后升的情况,在FV上涨后要把低于其初始入账价值的上涨部分计入I/S中,超过部分的FV上涨计入OCI。而fair value model的处理相对简单,所有FV的涨跌都计入I/S。

由于这两个model都基于fair value入账,所以资产的fair value都必须能够可靠的计量,A很明显是正确的。对于 revaluation model来说,超过其初始入账价值的FV涨跌反映在OCI里,不通过I/S,所以B不对。C很明显是错的,对于fair value model,所有FV的涨跌都会影响NI,而revaluation model中所有低于初始入账价值的涨跌都计入I/S中,也会影响NI。

易错点分析

这道题如果做错,说明没有掌握这两个model的会计处理方法。Fair value model是国际准则下投资性房地产可以使用的一个会计方法,会计处理很简单。而revaluation model涉及到I/S和OCI两个科目的选择,所以需要考生区分不同的确认情形。

精选问答8

题干

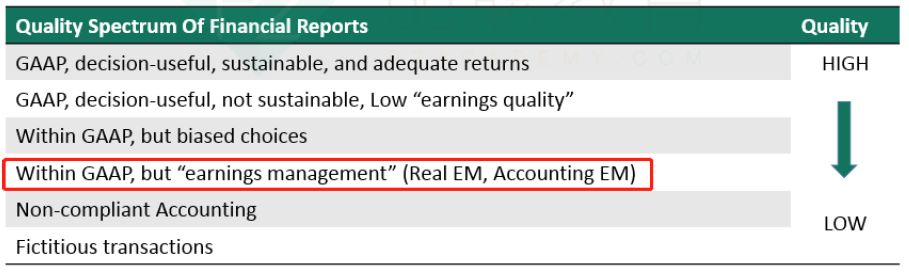

When earnings are increased by deferring research and development (R&D) investments until the next reporting period,this choice is considered:

A. non-compliant accounting.

B. earnings management as a result of areal action.

C. earnings management as a result of an accounting choice

答案解析

B is correct.

Deferring research and development(R&D) investments into the next reporting period is an example of earnings management by taking a real action.

解题思路

这道题的考点是“quality spectrum”。在“Within GAAP,but earnings management”这个level中,教材中提到了两个EM(earningsmanagement)的方法,即real EM和accounting EM。Earnings management指的是主观上的故意选择来影响财务报表上的利润。

earning的操纵有两种方法:一个是“realaction”,主要涉及到费用和收入的确认,比如公司可以通过推迟确认费用或提前确认收入来达到操纵利润的目的,这道题说的推迟确认R&D费用就是一种real action;

第二个方法是改变会计估计来做高利润,这种方法叫“accounting choice”,比如公司通过减少对坏账金额或者减值额的估计来增加利润。

易错点分析

很多同学会选A,也就是公司没有遵守会计准则,那么就需要复习一下quality spectrum的几个level。Earnings management还是属于Within GAAP的,所以A不对。还要区分的就是BC选项的两个概念,这道题考的其实是原版书上的一段话,是一个很小的知识点,可以通过这道题来查缺补漏。