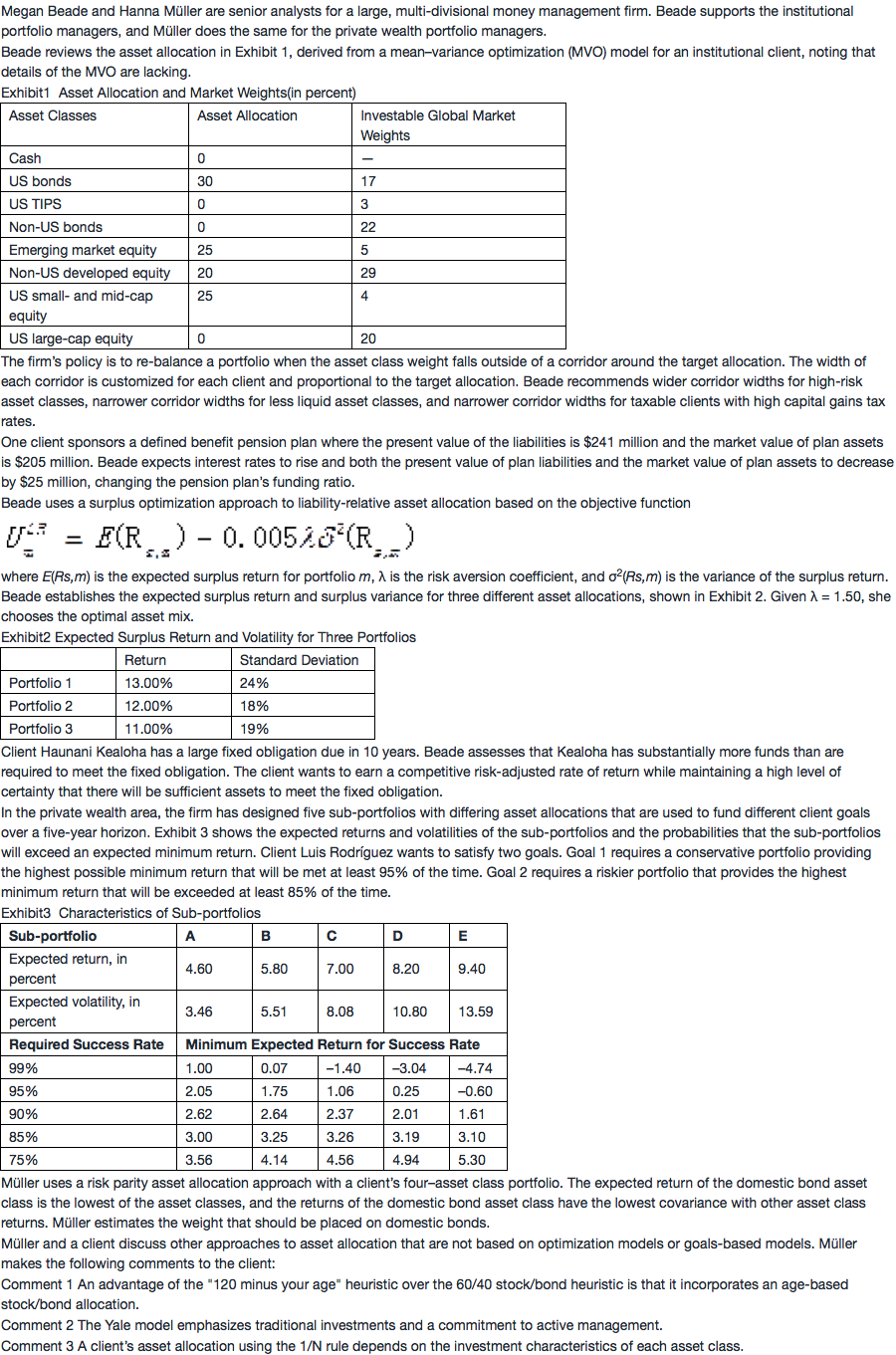

NO.PZ201803130100000105

问题如下:

The asset allocation approach most appropriate for client Kealoha is best described as:

选项:

A.a surplus optimization approach.

B.an integrated asset–liability approach.

C.a hedging/return-seeking portfolios approach.

解释:

C is correct.

The hedging/return-seeking portfolios approach is best for this client. Beade should construct two portfolios, one that includes riskless bonds that will pay of the fixed obligation in 10 years and the other a risky portfolio that earns a competitive risk-adjusted return. This approach is a simple two step process of hedging the fixed obligation and then investing the balance of the assets in a return-seeking portfolio.

选项A _surplus optimization, 为何不正确?

Surplus也能保证obligation和return seeking两个目标啊!