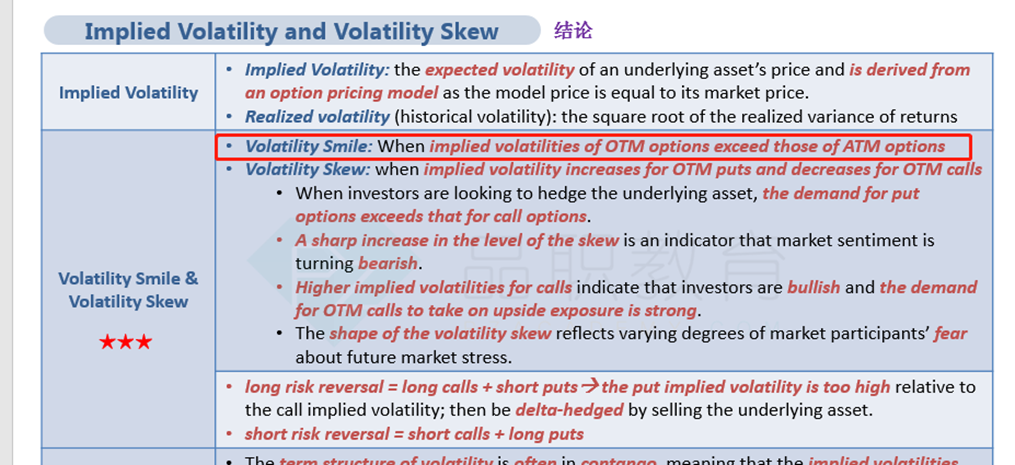

这道题的教材答案解析提到了:out of the money options will typically trade at higher implied volatility levels than at the money options. 请问是如何分析可以得到这个结论的呢?

伯恩_品职助教 · 2022年02月11日

嗨,爱思考的PZer你好:

同学你好,这个是在衍生品中学习过的哦。要注意学科之间的联系哦。

原因我大概给你说下吧,1987 年股市崩盘后,期权定价开始出现波动微笑。它们事先并未出现在美国市场,这表明市场结构更符合 Black-Scholes 模型的预测。 1987 年之后,交易员意识到可能会发生极端事件,并且市场存在显着偏差。期权定价需要考虑极端事件的可能性。因此,在现实世界中,隐含波动率会随着期权移动更多的 ITM 或 OTM 而增加或减少

Volatility smiles started occurring in options pricing after the 1987 stock market crash. They were not present in U.S. markets beforehand, indicating a market structure more in line with what the Black-Scholes model predicts. After 1987, traders realized that extreme events could happen and that markets have a significant skew. The possibility for extreme events needed to be factored into options pricing. Therefore, in the real world, implied volatility increases or decreases as options move more ITM or OTM

----------------------------------------------努力的时光都是限量版,加油!