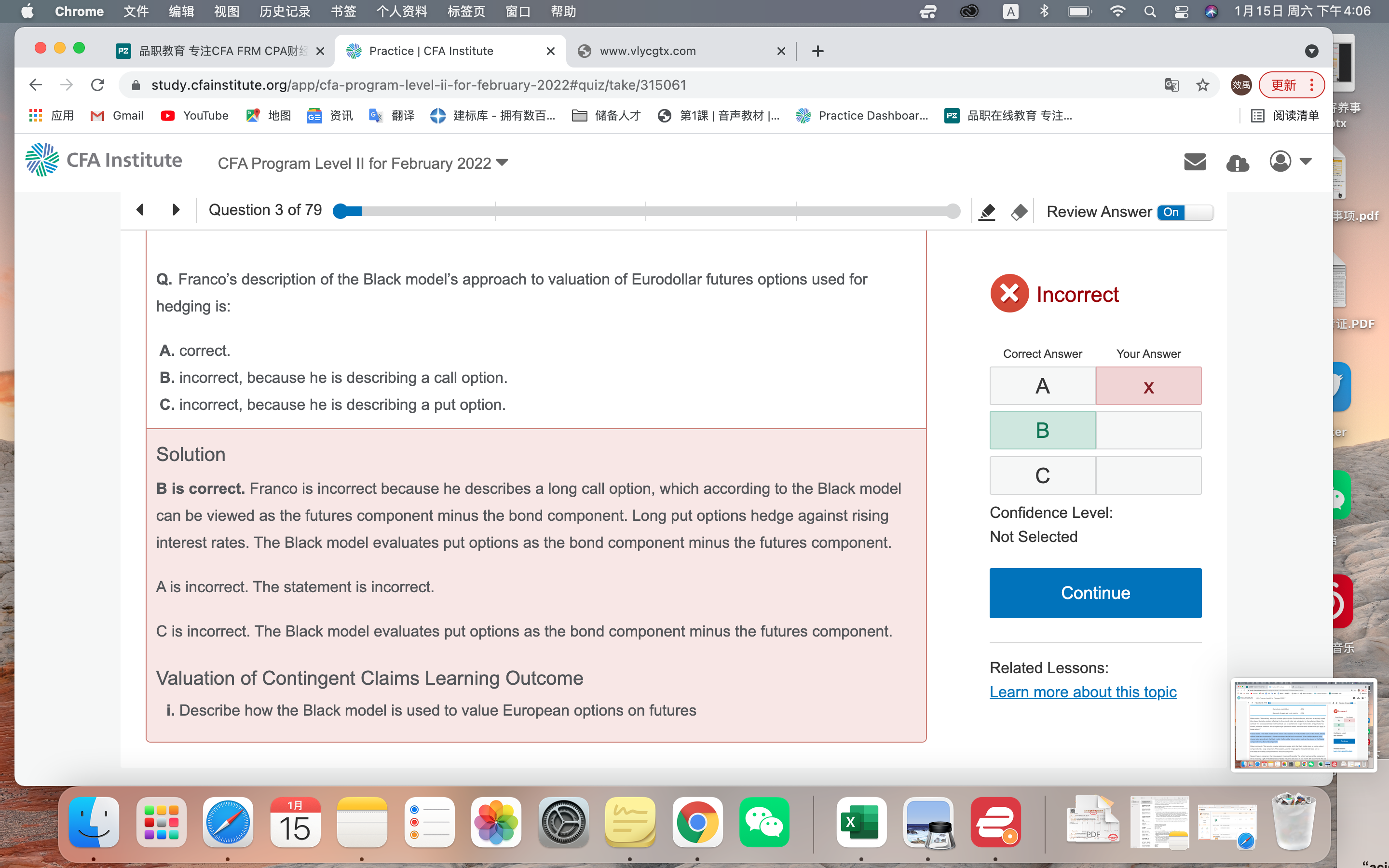

我知道Long call是可以用long future/spot + short bond合成,但是我们讲black on future的时候画图不也是long future+ short bond吗?请老师解释一下这道题,以及正确的black on future该怎么描述?

lynn_品职助教 · 2022年01月16日

嗨,从没放弃的小努力你好:

black on future的确也是long future + short bond,但是black model 需要对标准的BSM进行变形,剔除拿不到的期间收益。

“The Black model can be used to value options on the Eurodollar future. In this model, futures options have two components: a futures component adjusted for dividends and a bond component. When hedging against rising interest rates, according to the Black model, the Eurodollar futures option used can be viewed as the futures component adjusted for dividends minus the bond component.”

----------------------------------------------努力的时光都是限量版,加油!

Resapanda · 2022年01月23日

所以这道题应该说描述确实错了,但是错的点不是选项说的那样,是这样吗?