NO.PZ2020010801000037

问题如下:

You are interested in understanding the determinants of the yield spread of corporate bonds above a maturity matched sovereign bond. You include three explanatory variables: the leverage defined as the ratio of long-term debt to the book value of assets, a dummy variable for high yield, and a measure of the volatility of the profitability of the issuer. You are interested in testing whether there are nonlinear effects of some of these variables, and so use a RESET test including both the squared and cubic term. The of the original model is 68.6%, and the from the model that includes both additional terms is 68.9%. You have 456 observations. What do you conclude about the specification of the model?

选项:

解释:

The RESET test examines whether the two additional explanatory variables that squared and cubed fitted values have zero coefficients. It is implemented using an F-test:

The F-test examines the difference between the in the two models. The critical value for an is 3.01 (F.INV. RT(0.05,2,450) in Excel). The value of the test statistic is 2.17, which is less than the critical value, and so the null that the coefficient on the squared and cubic terms is 0 is not rejected.

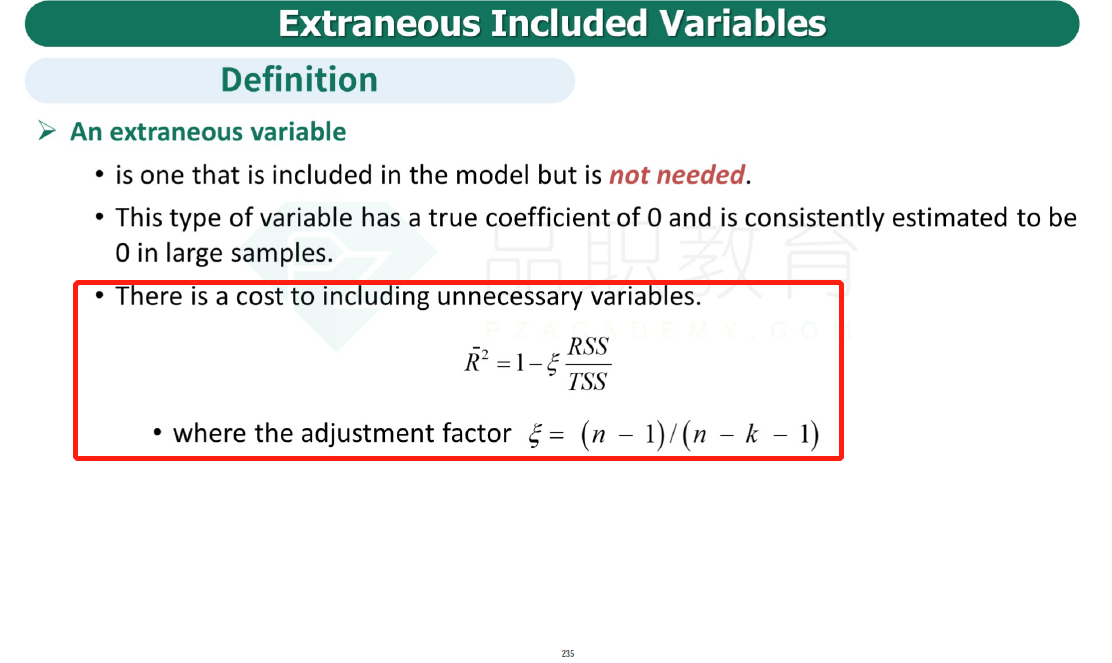

我用这个公式算加入两个变量后的R是68.69%>加入前的68.53%,为什么不能这么做,而需要用假设检验?