NO.PZ202106160300004405

问题如下:

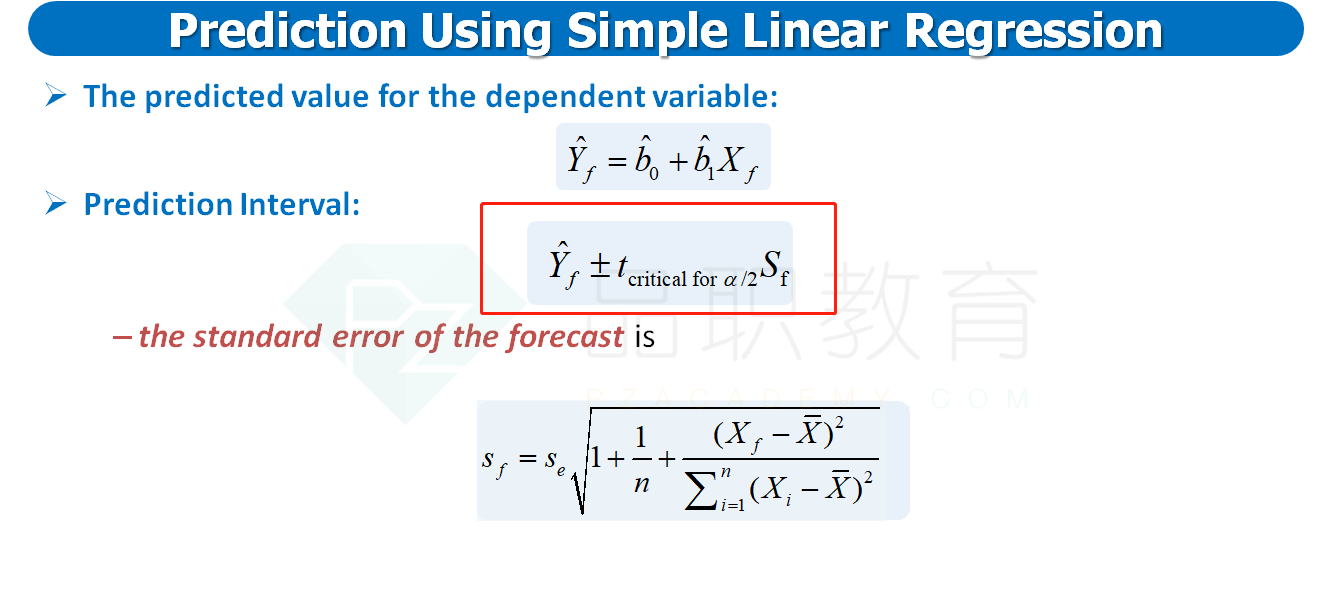

Using information from Exhibit 2, the 99% prediction interval for Amtex share return for Month 37 is best described as:

选项:

A. ±0.0053 B. ±0.0459 C. ±0.1279解释:

C is correct. The predicted share return is 0.0095 + 10.2354 × (-0.01)=0.0071. The lower limit for the prediction interval is 0.0071-(2.728 × 0.0469)=-0.1208, and the upper limit for the prediction interval is 0.0071 + (2.728 × 0.0469) = 0.1350.

A is incorrect because the bounds of the interval should be based on the standard error of the forecast and the critical t-value, not on the mean of the dependent variable.

B is incorrect because bounds of the interval are based on the product of the standard error of the forecast and the critical t-value, not simply the standard error of the forecast.

请问这个是运用Prediction Interval计算公式吗