NO.PZ2015121801000040

问题如下:

With respect to capital market theory, which of the following asset characteristics is least likely to impact the variance of an investor’s equally weighted portfolio?

选项:

A.Return on the asset.

B.Standard deviation of the asset.

C.Covariances of the asset with the other assets in the portfolio.

解释:

A is correct.

The asset’s returns are not used to calculate the portfolio’s variance [only the assets’weights, standard deviations (or variances), and covariances (or correlations) are used].

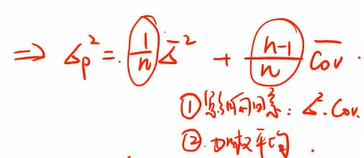

如题。。。。。。。。。。。。。。

当n趋近于无穷大的时候,方差前面的系数1/n趋近于0,所以说影响因素近乎只有协方差。

当n趋近于无穷大的时候,方差前面的系数1/n趋近于0,所以说影响因素近乎只有协方差。