NO.PZ201812020100000406

问题如下:

Based on Exhibit 1, which of the portfolios will best immunize SD&R’s single liability?

选项:

A.Portfolio 1

B.Portfolio 2

C.Portfolio 3

解释:

B is correct.

In the case of a single liability, immunization is achieved by matching the bond portfolio’s Macaulay duration with the horizon date. DFC has a single liability of $500 million due in nine years. Portfolio 2 has a Macaulay duration of 8.9, which is closer to 9 than that of either Portfolio 1 or 3. Therefore, Portfolio 2 will best immunize the portfolio against the liability.

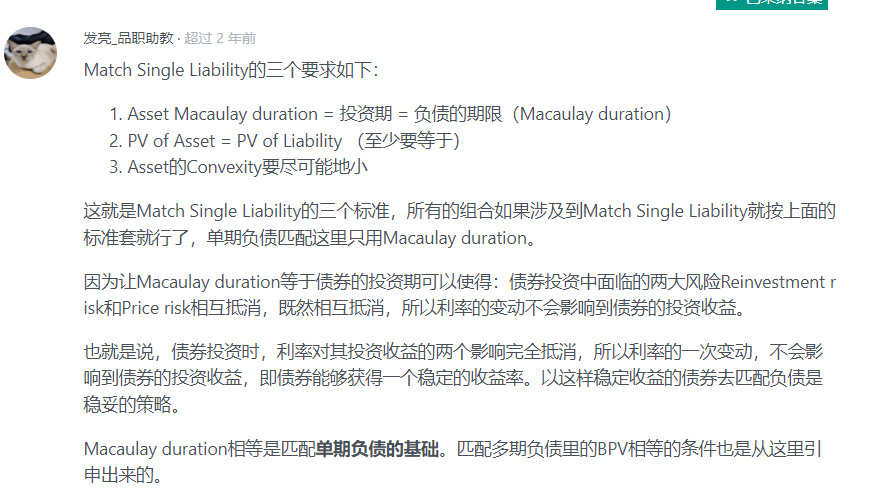

之前老师回答过别人的问题,我在这里还有一个多小疑问,如果是Match Multiple Liability,也是Match Macaulay Duration吗?关于Match Duration 究竟要Match Macaulay Duration还是Match effective duration我有点记不清了,麻烦老师帮忙解答,谢谢!