为什么不选d选项

Rt/vt=ro/vo

不应该是这样吗?

问题如下图:

选项:

A.

B.

C.

D.

解释:

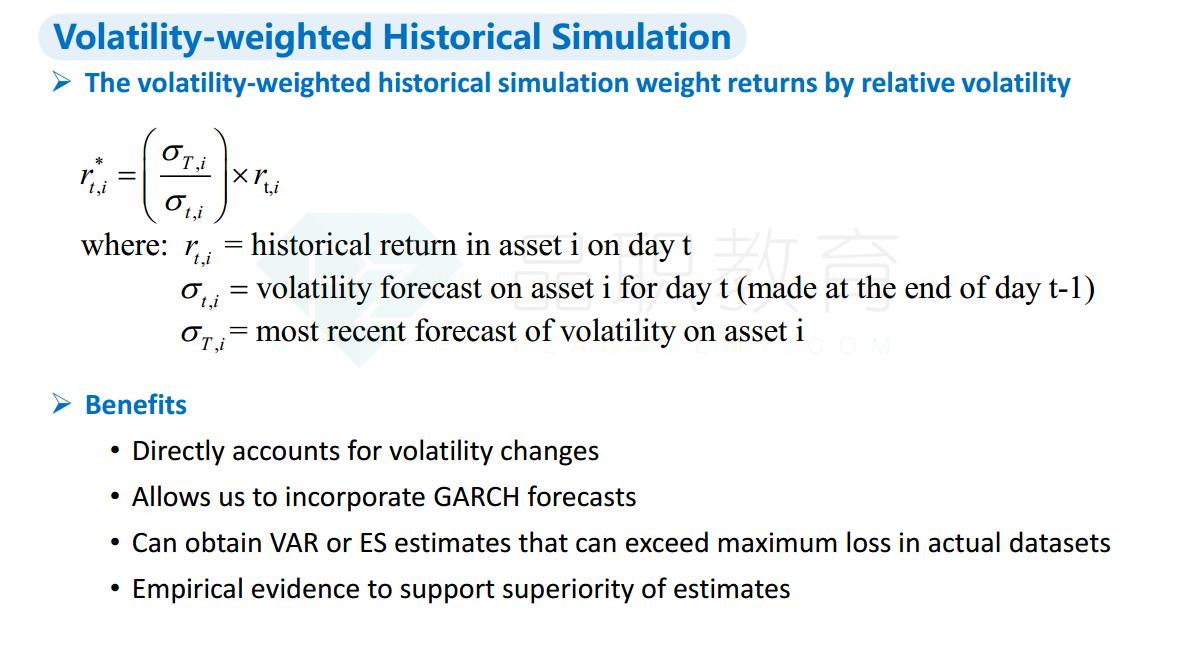

NO.PZ2018122701000013 问题如下 If volatility (0) is the current (toy’s) volatility estimate anvolatility (t) is the volatility estimate on a previous y (t), whibest scribes volatility-weightehistoricsimulation? First contypichistoricsimulation (HS) on return series. Then multiply Vvolatility(0)/volatility(t) First contypichistoricsimulation (HS) on return series. Then multiply Vvolatility(t)/volatility(0) Eahistoricreturn (t) is replaceby: return (t)*volatility (0)/volatility (t). Then contypichistorical simulation (HS) on austereturn series. Eahistoricreturn (t) is replaceby: return (t)*volatility (t)/volatility (0). Then contypichistorical simulation (HS) on austereturn series. C is correct. 考点 : WeighteHistoric Simulation Approaches 解析 : Eahistoricreturn (t) is replaceby: return(t) × volatility(0)/volatility(t). Then contypichistorical simulation (HS) on austereturn series For example, if on the historicy (t), the return(t) w-2.0% anvolatility(t) w10%, while toy’s volatility estimate is 20%, then the austereturn is -2.0% × 20%/10% = - 4.0% . In this way, \"Actureturns in any periot are therefore increase(or crease, penng on whether the current forecast of volatility is greater (or less than) the estimatevolatility for periot. We now calculate the HS P/L using [the austereturns] insteof the originta set, anthen proceeto estimate HS VaRs or ESs in the trationw(i.e., with equweights, etc.). 老师First contypichistoricsimulation (HS) on return series怎么理解?

NO.PZ2018122701000013