(1)题目重点“operational Risk Capital”是不是就是书上的“Economic Capital”,两者是一样的吧?

(2)Hedge Fund不包含“active share ”(书上的定义是“ the measure of that percentage of the portfolio that differs from the benchmark index”),怎么理解不包含“active share”?

(3)Pension Plan 不包含“Operational Risk Capital”,怎么理解,不需要包含“操作风险资本”吗?谢谢!

Muckroth Investment Management Case Scenario

Dierdre O’Callahan is a senior risk manager at Muckroth Investment Management, a global investment firm headquartered in Dublin, Ireland. O’Callahan’s team is responsible for tracking and estimating portfolio risk for the firm’s various investment strategies and for communicating risk exposures to Muckroth’s portfolio managers, investment committee, and chief risk officer. O’Callahan’s team also offers risk consulting services to the firm’s institutional investor clients.

When assessing portfolio risk, O’Callahan makes frequent use of value at risk (VaR) in addition to other measures, such as volatility, sensitivity risk, and scenario risk. O’Callahan believes that VaR is an appropriate risk measure in this application for the following reasons:

Reason 1The reliability of VaR can be easily verified through a process known as backtesting.

Reason 2VaR takes portfolio liquidity into account when some of the assets are relatively illiquid.

Reason 3VaR effectively accounts for an increase in asset correlations during times of market stress.

Michelle Ryan is a senior portfolio manager on the Muckroth Alpha Fund. Ryan and O’Callahan are reviewing the VaR report O’Callahan prepared for this fund to ensure that the fund is within the risk parameters established by the firm and communicated to investors. The Alpha Fund has assets under management of €315 million and has an expected annualized return of 10.4% with a volatility of 17.52%. The report describes VaR in both percentage and euro terms. It uses the parametric method of VaR at the 5% level (1.65 standard deviations), assuming 250 trading days per year.

After reviewing the current VaR report, Ryan asks O’Callahan to calculate how much the VaR estimate would change if she were to reduce the portfolio weight of Bordeaux Industries stock in the Alpha Fund from 6% to 2% of the portfolio and then use the proceeds to establish a new 4% position in Riga Bank & Trust. O’Callahan tells Ryan that there are several extensions of VaR analysis that she can run.

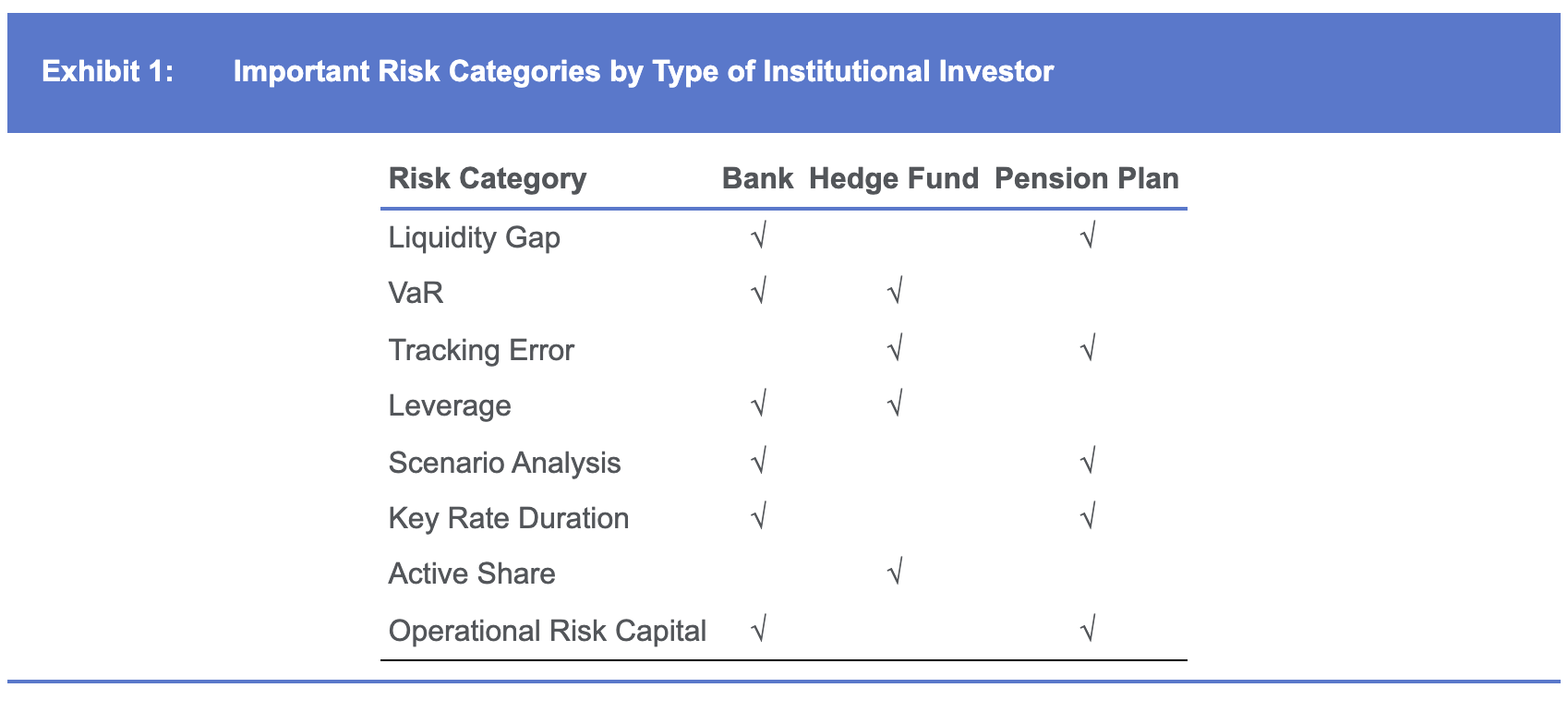

Axiomada, a prospective institutional client, is impressed by Muckroth’s investment track record and would like to learn more about the consulting services Muckroth offers to monitor risk. Representatives from Axiomada set up a meeting with O’Callahan to discuss how Muckroth considers important risk categories facing institutional investors. O’Callahan provides Axiomada with a risk management document Muckroth has prepared for institutional clients that includes Exhibit 1. Exhibit 1 illustrates how Muckroth considers a variety of different risk categories depending on the type of institutional investor.

Q:In Exhibit 1 provided to Axiomada, for which institutional investor type does Muckroth most likely accurately list important risk categories?

A. Bank

B. Hedge fund

C. Pension plan

Solution

A is correct. The Muckroth team is accurately describing risk considerations facing a bank, which include liquidity gap, VaR, leverage, key rate duration, operational risk capital, and scenario analysis.

B is incorrect. Hedge funds would not be focused on categories such as tracking error or active shares, which are more traditional asset manager metrics, and instead would be focused on categories such as sensitivities, scenario analysis, gross exposure, and drawdown.

C is incorrect. Pension plans are less likely to focus on items such as operational risk capital and would include VaR (surplus at risk), interest rate and curve risk, glide path, and liability hedging exposures instead of return-generating exposures.

Measuring and Managing Market Risk Learning Outcome

- Describe risk measures used by banks, asset managers, pension funds, and insurers