NO.PZ201602060100001001

问题如下:

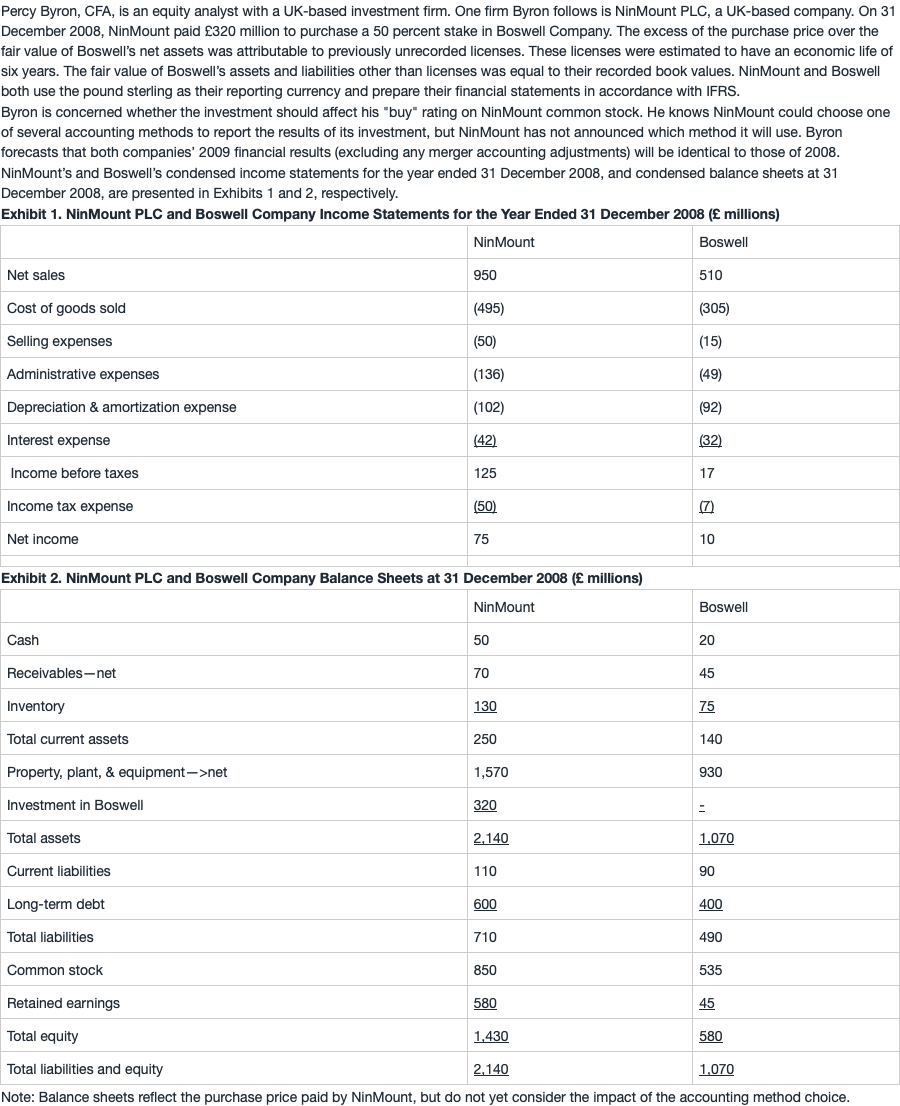

NinMount’s current ratio on 31 December 2018 most likely will be highest if the results of the acquisition are reported using:

选项:

A.

the equity method.

B.

consolidation with full goodwill.

C.

consolidation with partial goodwill.

解释:

A is correct.

The current ratio using the equity method of accounting is Current assets/Current liabilities = £250/£110 = 2.27. Using consolidation (either full or partial goodwill), the current ratio = £390/£200 = 1.95. Therefore, the current ratio is highest using the equity method.

考点 : 不同合并会计报表方法对会计比率的影响 。

解析 :

current ratio =Current assets/Current liabilities

equity method不影响current asset和current liability, current ratio = £250/£110 = 2.27.

consolidation需要合并子公司的全部资产和负债 , current ratio=£390/£200 = 1.95

这道题没有goodwill,但要注意:不管有没有goodwill,partial goodwill与full goodwill的方式都不影响current asset的金额,因为goodwill属于长期资产。

因此,选项A正确。

※ 没有goodwill的原因:

题干中的信息: 超出net fair value的部分是由于要购买unrecorded licenses , 其他资产和负债的fair value=book value。这句话可以得到两个结论:

1. 子公司有一个未记账的资产,而在合并报表中,这项资产应该计入资产负债表。它的价值是并购对价超过子公司净资产fair value的部分。

相当于是NinMount公司花320买了Boswell公司一半的identifiable assets(包括已入账的也包括未入账的)。如果要买全部的identifiable assets则要花640:其中580是为了买已入账的identifiable assets,剩下的60根据题目信息,都是为了买这个unrecorded license。

2. 该项投资不产生goodwill,因为goodwill的定义是并购对价超过子公司net identifiable asset的部分,这个net identifiable asset既包含入账的资产,也包含之前没有记账但合并时应该记账的资产。因此本题并购的对价等于所购买的子公司的net identifiable asset,即没有goodwill。

解答部分:Net identifiable asset中580是怎么来的?