NO.PZ2020042003000049

问题如下:

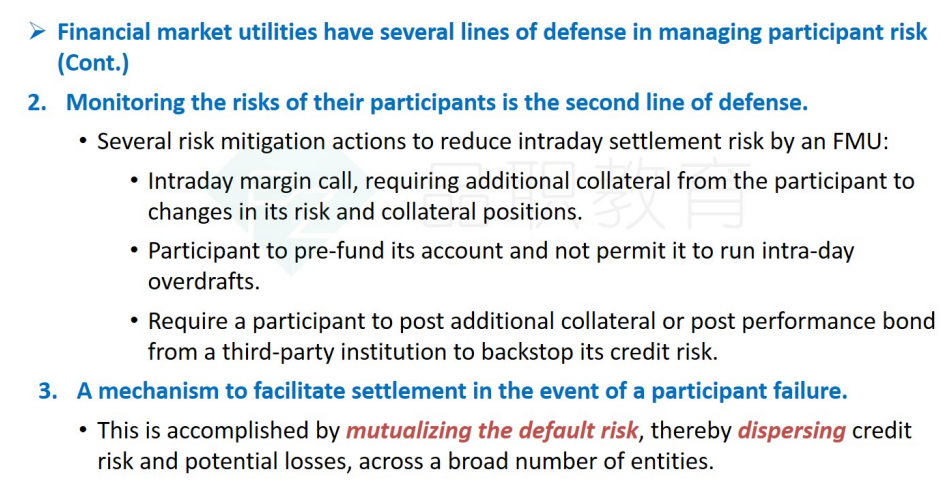

Financial market utilities have several

lines of defense in managing participant risk. The following statements are

about these methods, which of the followings is NOT correct?

选项:

A. FMUs use criteria like size

and creditworthiness to constrain its direct members.

B. FMUs have direct exposure

with first-and second-tier banks

C. FMUs periodically monitor their

participants settlement positions and margin collateral.

D. FMUs mutualize the default risk, thereby

dispersing credit risk and potential losses, across a broad number of entities.

解释:

考点:对Risk Management, Measurement and

Monitoring Tools for FMUs的理解

答案:B

解析:

FMUs只与符合条件的First-tier

bank有直接交易,Second-tier banks的交易与First-tier

banks完成。

麻烦再解答一下d选项