NO.PZ201512020300000806

问题如下:

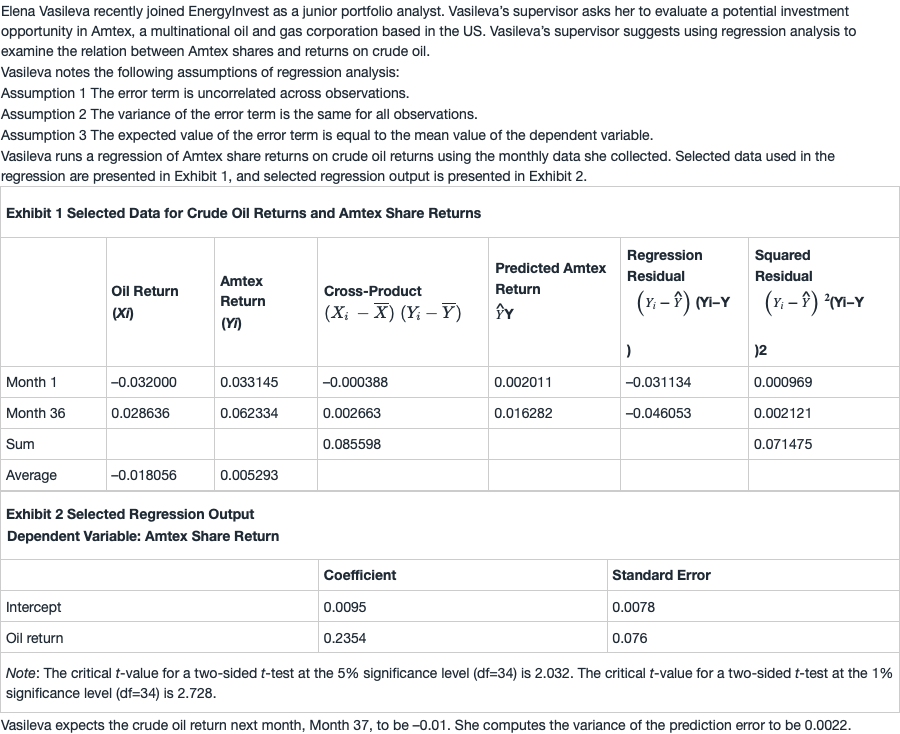

Using information from Exhibit 2, Vasileva should compute the 95% prediction interval for Amtex share return for month 37 to be:

选项:

A.–0.0882 to 0.1025.

–0.0835 to 0.1072.

0.0027 to 0.0116.

解释:

A is correct. The 95% prediction iinterval for the dependent variable given a certain value of the independent variable is calculated as:

Prediction interval =

and the predicted value

Therefore:

Predicted value = 0.0095 + (0.2354 × (–0.01)) = 0.0071

The lower limit for the prediction interval = 0.0071 – (2.032 × 0.0469) = –0.0882

The upper limit for the prediction interval = 0.0071 + (2.032 × 0.0469) = 0.1025

如果题目问求95% interval of slope (oil return),就直接用表格中0.2354+/-1.96*0.046来算吗? 如何判断题目问的到底是95% of Y 还是表格中的 oil return (b1)呢?表格中b1和Y都叫做oil return