NO.PZ2019012201000050

问题如下:

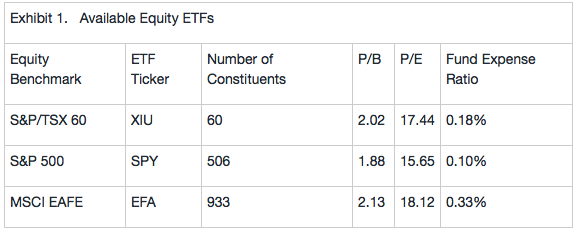

Winthrop and Tong agree

that only the existing equity investments need to be liquidated. Tong suggests

that, as an alternative to direct equity investments, the new equity portfolio

be composed of the exchange-traded funds (ETFs) shown in Exhibit 1.

Based

on Exhibit 1 and assuming a full-replication indexing approach, the tracking

error is expected to be highest for:

选项:

A.XIU

SPY

EFA

解释:

An index that contains a large number of constituents will tend to

create higher tracking error than one with fewer constituents. Based on the

number of constituents in the three indexes (S&P/TSX 60 has 60, S&P 500

has 506, and MSCI EAFE has 933), EFA (the MSCI EAFE ETF) is expected to have

the highest tracking error. Higher expense ratios (XIU: 0.18%; SPY: 0.10%; and EFA:

0.33%) also contribute to lower excess returns and higher tracking error, which

implies that EFA has the highest expected tracking error.

老师,请帮我看下我的这两个理解是否正确:

1.benchmark中的股票数量越多,就越不好跟踪,tracking error就越大;

2.给定benchmark中的股票数量,我们所构建的要跟踪benchmark的那个portfolio中的股票数量约接近benchmark中的股票数量,跟踪的就越好,tracking error就越小。

谢谢!