NO.PZ2017092702000155

问题如下:

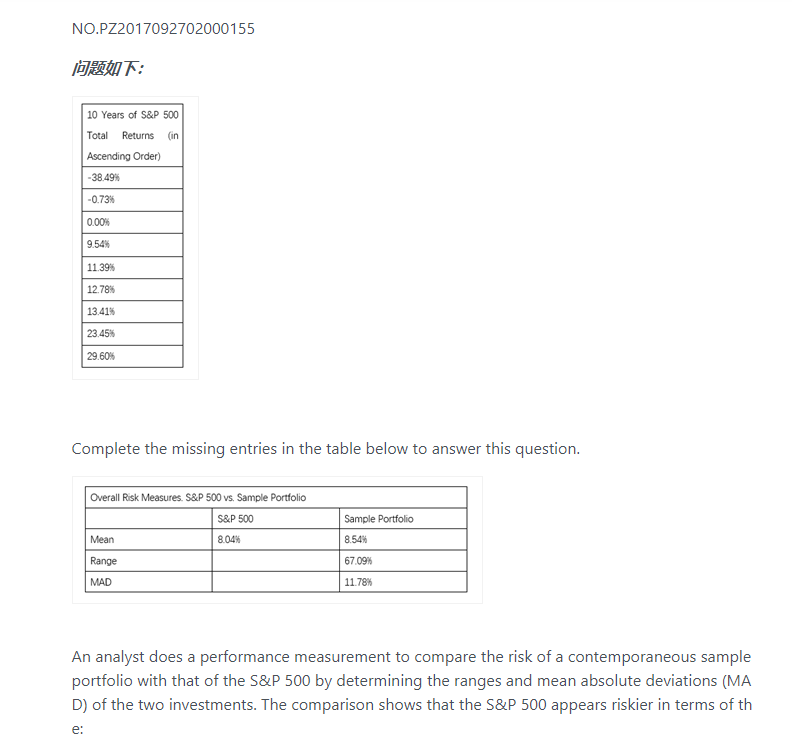

Complete the missing entries in the table below to answer this question.

An analyst does a performance measurement to compare the risk of a contemporaneous sample portfolio with that of the S&P 500 by determining the ranges and mean absolute deviations (MAD) of the two investments. The comparison shows that the S&P 500 appears riskier in terms of the:

选项:

A. range only

B. MAD only.

C. MAD and range.

解释:

C is correct. Both the range and MAD of the S&P 500 are greater than the range and MAD of the sample portfolio. Thus both measures indicate the S&P 500 is riskier. The range for the S&P 500 equals the distance between the lowest and highest

values in the dataset. That distance for the S&P 500 is [29.60% – (–38.49%)] = 68.09%. Given that this range is larger than the range of the sample portfolio at 67.09%, the S&P 500 appears riskier than the sample portfolio. The MAD for the S&P 500 returns equals the sum of the absolute deviations from the mean return divided by the number of observations.

MADS&P500 = 12.67%

Given that the MAD for the S&P 500 is greater than the MAD for the sample portfolio (12.67% versus 11.78%), the S&P 500 appears riskier than the sample portfolio.

A is incorrect because although the S&P 500 is correctly identified as having the larger range, the sample portfolio has a smaller MAD.

B is incorrect because although the S&P 500 is correctly identified as having the larger MAD, the Sample Portfolio has a smaller range.