NO.PZ201812020100000408

问题如下:

Which of the custom benchmark’s characteristics violates the requirements for an appropriate benchmark portfolio?

选项:

A.Characteristic 1

B.Characteristic 2

C.Characteristic 3

解释:

B is correct.

The use of an index as a widely accepted benchmark requires clear, transparent rules for security inclusion and weighting, investability, daily valuation, availability of past returns, and turnover. Because the custom benchmark is valued weekly rather than daily, this characteristic would be inconsistent with an appropriate benchmark.

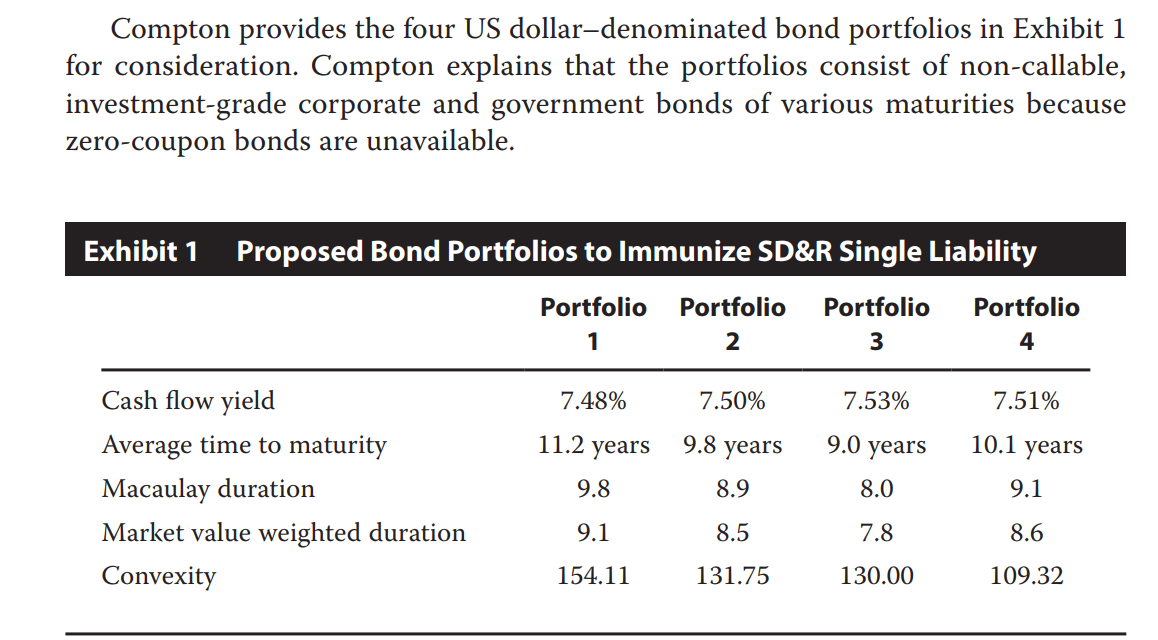

Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. 文中提到了这句 那么A选项没有国债 总感觉不对,请老师解答