NO.PZ201712110200000304

问题如下:

Based on the information in Exhibit 1 and Exhibit 2, the value of the embedded option in Bond 4 is closest to:

选项:

A.nil.

B.0.1906.

C.0.3343.

解释:

C is correct.

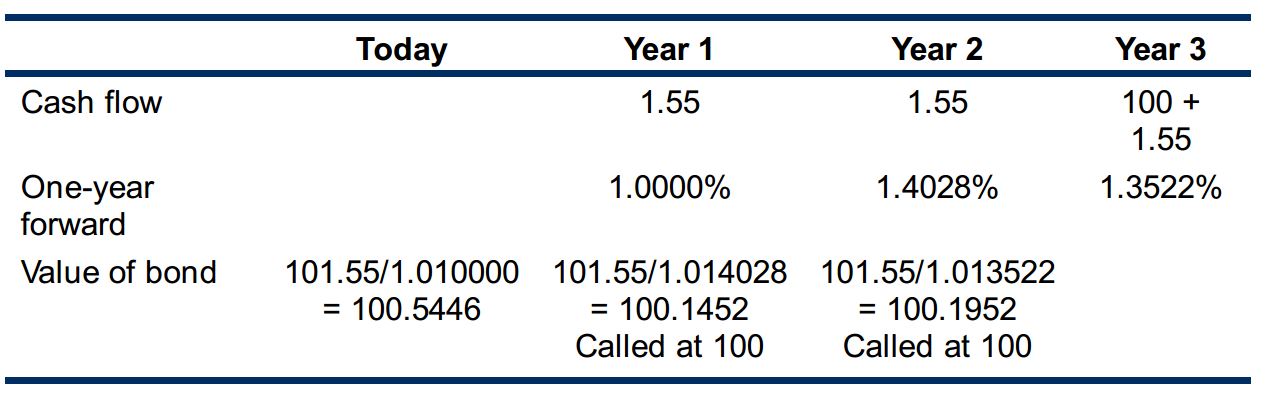

Bond 4 is a callable bond. Value of an issuer call option = Value of straight bond – Value of callable bond. The value of the straight bond may be calculated using the spot rates or the one-year forward rates.

Value of an option-free (straight) bond with a 1.55% coupon using spot rates:

1.55/(1.0100)1 + 1.55/(1.012012)2 + 101.55/(1.012515)3 = 100.8789.

The value of a callable bond (at par) with no lockout period and a 1.55% coupon rate is 100.5446, the value of the call option = 100.8789 – 100.5446 = 0.3343.

因为票面利率是大于forward rate所以每一期都会call,就直接100/第一期的foward rate就可以了吗?