NO.PZ2019103001000052

问题如下:

Silvia Abram and Walter Edgarton are analysts with Cefrino Investments, which sponsors the Cefrino Sovereign Bond Fund (the Fund). Abram and Edgarton recently attended an investment committee meeting where interest rate expectations for the next 12 months were discussed. The Fund’s mandate allows its duration to fluctuate ±0.30 per year from the benchmark duration. The Fund’s duration is currently equal to its benchmark. Although the Fund is presently invested entirely in annual coupon sovereign bonds, its investment policy also allows investments in mortgage-backed securities (MBS) and call options on government bond futures. The Fund’s current holdings of on-the-run bonds are presented in Exhibit 1.

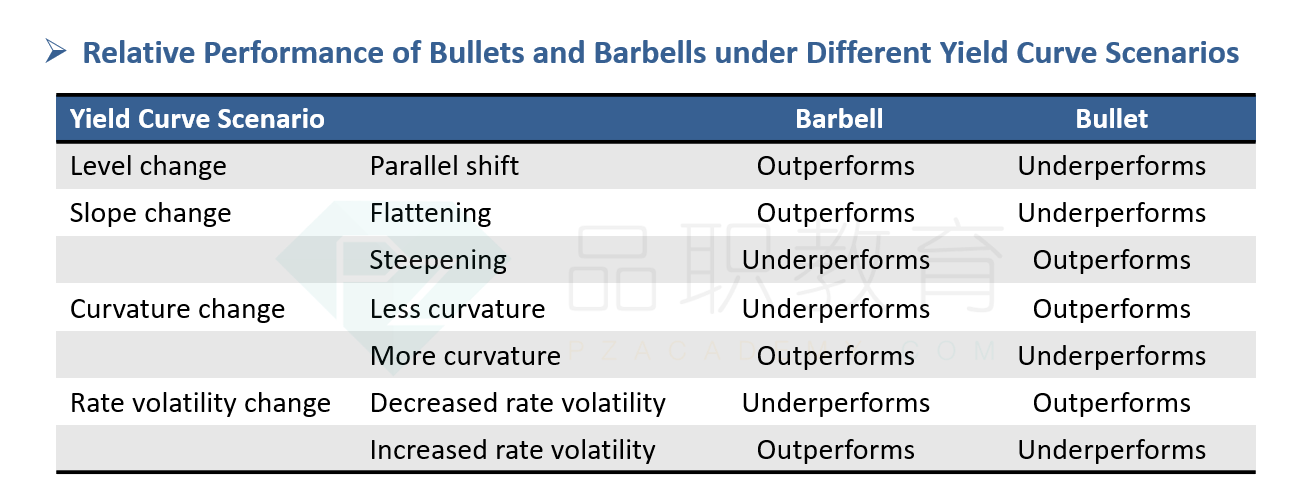

Over the next 12 months, Abram expects a stable yield curve; however, Edgarton expects a steepening yield curve, with short-term yields rising by 1.00% and long-term yields rising by more than 1.00%.

Based on Edgarton’s expectation for the yield curve over the next 12 months, the Fund’s return relative to the benchmark would most likely increase by:

选项:

A. riding the yield curve

B. implementing a barbell structure.

C. shortening the portfolio duration relative to the benchmark.

解释:

C is correct.

If interest rates rise and the yield curve steepens as Edgarton expects, then shortening the Fund’s duration from a neutral position to one that is shorter than the benchmark will improve the portfolio’s return relative to the benchmark. This duration management strategy will avoid losses from long-term interest rate increases.