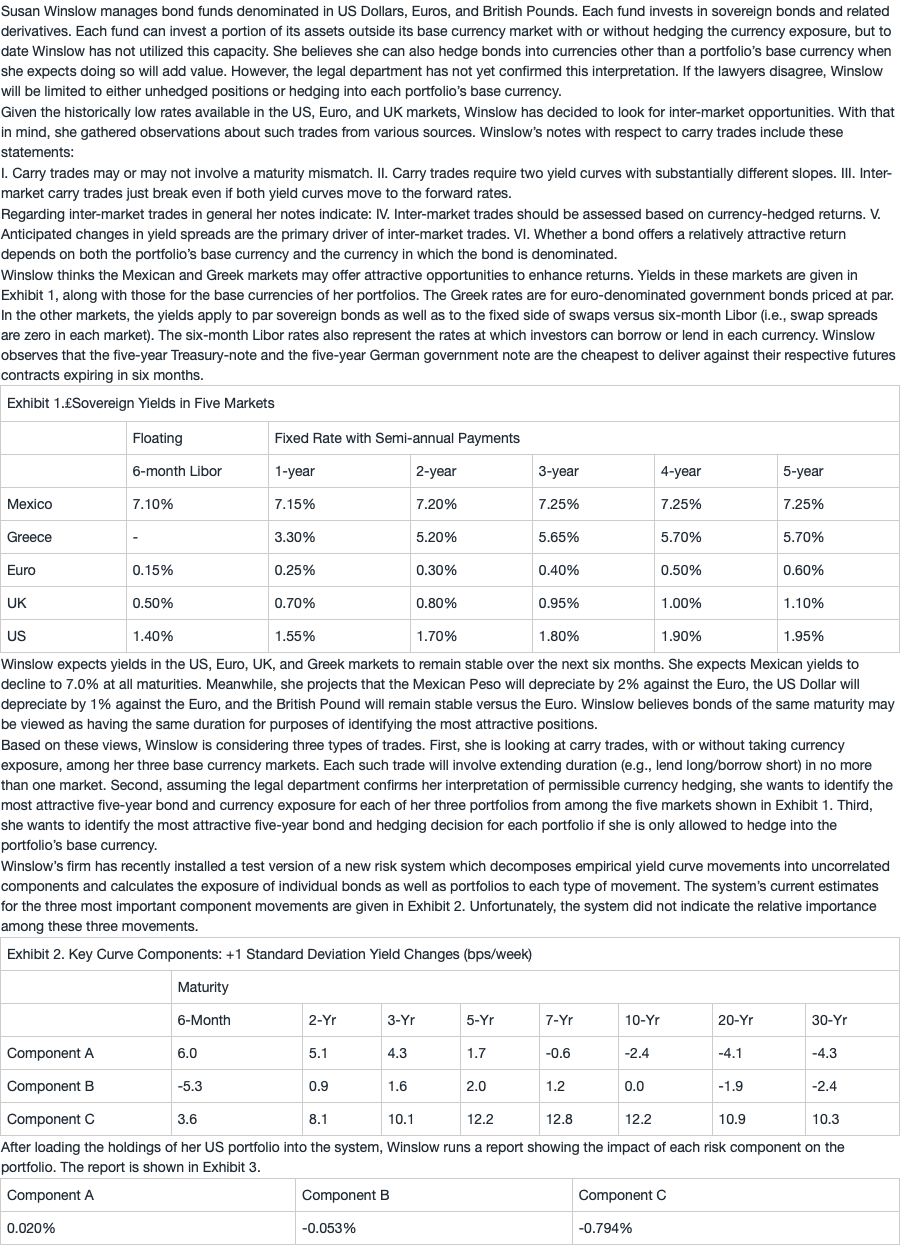

嗨,从没放弃的小努力你好:

Statement IV: Inter-market trades should be assessed based on currency-hedged returns.

这句是说,当我们做国际债券投资时,例如,在一堆国外债券里面选择出收益率最高的债券时,我们需要将所有债券的收益先Hedge成一个Common currency,目的是统一核算标准,这样收益率才有可比较性。

Statement IV完全正确。这道题让选不正确的描述,所以排除A选项。

对应的答案解释为:

Winslow’s Statement IV is correct. Inter-market trades should be assessed on the basis of returns hedged into a common currency. Doing so ensures that they are comparable. Neither local currency returns nor unhedged returns are comparable across markets because they involve different currency exposures/risks.

其中:

Inter-market trades should be assessed on the basis of returns hedged into a common currency.

这句是说,需要将国外的债券收益,Hedge成Common currency,然后才能进行比较。

例如,现在有EUR债券收益2.5%,GBP债券收益3.2%,MXN债券收益3.7%,USD债券收益4.5%;

我们需要在里面找到收益最高的债券,显然这些债券的收益都是以不同的货币计价的,是不可比的,因此我们需要将他们Hedge成一个Common currency,然后才能进行比较。例如,将以上所有债券的收益Hedge成EUR,然后再进行比较。

Doing so ensures that they are comparable.Neither local currency returns nor unhedged returns are comparable across markets because they involve different currency exposures/risks.

这句是说,Hedge的目的是可以实现收益可比。以当地货币计价的收益(Local currency returns),以及未Hedge的收益,这些收益是不可比的,因为他们本身就含有不同的货币风险。

所以,我们只有先Hedge成Common currency,把货币风险消除掉之后,不同国家的债券收益才可以比较。

Statement V:Anticipated changes in yield spreads are the primary driver of inter-market trades.

这句是说,预期的利率变动,是我们在债券投资时的首要考虑因素。这点完全正确。

例如,我们预期US利率稳定,UK利率下降1%,EUR利率上升1%;那显然,我们投资UK债券最好。因为UK利率下降,我们投资UK债券可以赚取很高的Capital gain。

虽然投资债券还有其他的收益来源:Coupon的收益,以及Roll down return的收益;但是和利率变动带来的Capital gain相比,Coupon收益与Roll down reutn的收益规模太小了。

因此,在国际市场债券投资时,利率之间的相对变化时首要考虑因素。

Statement V也正确,因此本题不选。

这个Statement对应的答案解释为:

The primary driver of inter-market trades is anticipated changes in yield differentials. Over horizons most relevant for active bond management, the capital gains/losses arising from yield movements generally dominate the income component of return (i.e., carry) and rolling down the curve. Hence, expectations with respect to yield movements are the primary driver of inter-market trade decisions.

其中The primary driver of inter-market trades is anticipated changes in yield differentials,他是说Inter-market trade首要考虑的因素(首要收益来源)就是预期的利率变动(Yield differentials)。

Over horizons most relevant for active bond management, the capital gains/losses arising from yield movements generally dominate the income component of return (i.e., carry) and rolling down the curve.

这句是说,在债券的主动管理投资策略里,利率变动带来的Capital gain or loss,这种收益的规模,要远远的大于(Dominate)Coupon和Rolldown return收益的规模。

Hence, expectations with respect to yield movements are the primary driver of inter-market trade decisions.

这句说,因此,Inter-market trade decision的首要决定因素是yield movements。

Statement VI:Whether a bond offers a relatively attractive return depends on both the portfolio’s base currency and the currency in which the bond is denominated.

这句是说,债券是否能够提供较高的收益,要取决于组合的Base currency,以及债券的计价货币。

这点错误,债券的收益是否有吸引力,与组合的Base currency无关。

例如,现在有UK债券、EUR债券、MXN债券、USD债券。我们为了比较他们的收益,将他们都Hedge成USD,收益的排序是:

UK债 > EUR债 > MXN债 > USD债,这样的排序,无论是对UK-Based portfolio,还是对CNY-Based portfolio,还是对JPY-based portfolio,都适用。

也就说,一旦Hedge成Common currency之后,债券的排序定死,他们的吸引力与Portfolio的Base currency无关。

同时,债券的吸引力与债券的计价货币有关。因为将UK债Hedge成USD,和将EUR债Hedge成USD的收益不同,因此债券的吸引力与债券计价的Currency有关。

对于的答案为:

Due to covered interest arbitrage, the relative attractiveness of bonds does not depend on the currency into which they are hedged for comparison.

这句是说,根据Covered interest arbitragey,我们将债券Hedge成Common currency进行比较时,债券的吸引力与Hedge成哪种货币无关。完全正确。

也就是为了比较,我们Hedge成USD也行,Hedge成CNY也行,Hedge成EUR也行,一旦Hedge成Common currency之后,债券的收益排序就是定死的了。与Hedge成哪个Common currency无关。

Hence, the ranking of bonds does not depend on the base currency of the portfolio.

这句是说,Hedge成Common currency之后,债券的吸引力与Portfolio的Base currency无关。上面已解释。

----------------------------------------------

虽然现在很辛苦,但努力过的感觉真的很好,加油!