问题如下:

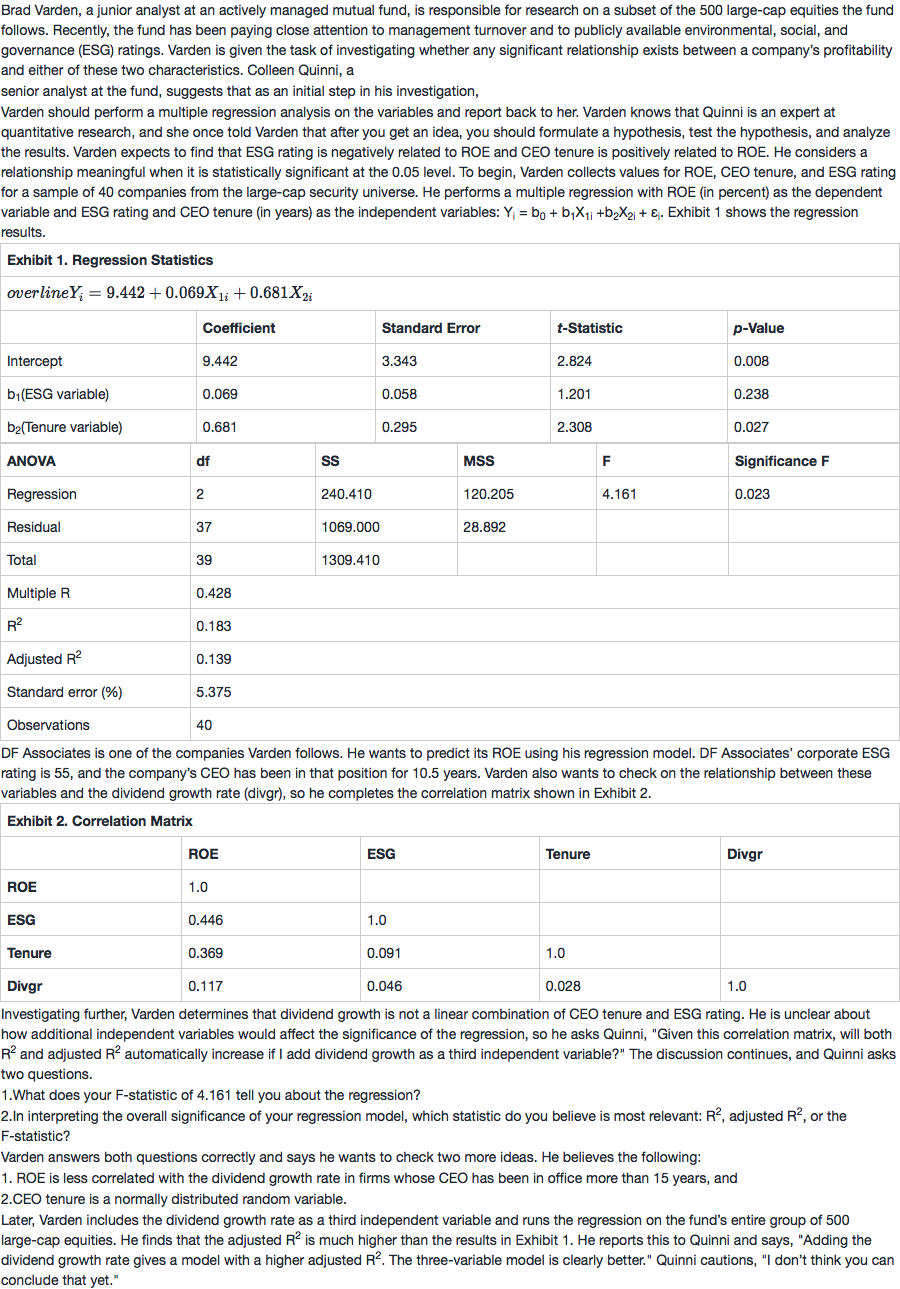

1. Based on Exhibit 1 and given Varden’s expectations, which is the best null hypothesis and conclusion regarding CEO tenure?

选项:

A. b2≤ 0; reject the null hypothesis

B. b2 = 0; cannot reject the null hypothesis

C. b2 ≥ 0; reject the null hypothesis

解释:

A is correct. Varden expects to find that CEO tenure is positively related to the firm’s ROE. If he is correct, the regression coefficient for tenure, b2, will be greater than zero (b2 > 0) and statistically significant. The null hypothesis supposes that the "suspected" condition is not true, so the null hypothesis should state the variable is less than or equal to zero. The t-statistic for tenure is 2.308, significant at the 0.027 level, meeting Varden’s 0.05 significance requirement. Varden should reject the null hypothesis.

如果是用T statistic和critical value做比较,critical value是1.96还是1.65?