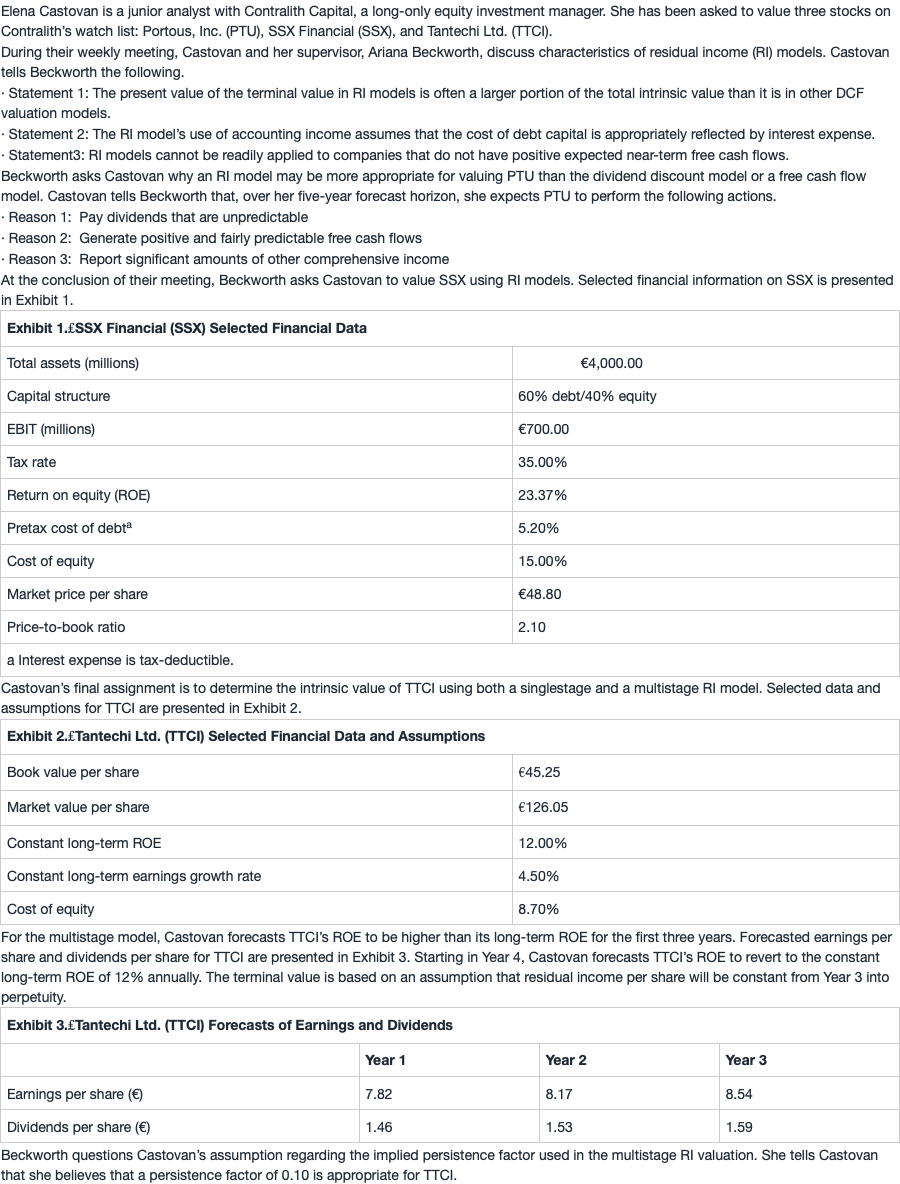

问题如下:

8. Based on Exhibits 2 and 3 and the multistage RI model, Castovan should estimate the intrinsic value of TTCI to be closest to:

选项:

A.€54.88.

B.€83.01.

C.€85.71.

解释:

C is correct.

Residual income per share for the next three years is calculated as follows.

Because Castovan forecasts that residual income per share will be constant into perpetuity, equal to Year 3 residual income per share, the present value of the terminal value is calculated using a persistence factor of 1.

Present value of terminal value =

= =33.78

So, the intrinsic value of TTCI is then calculated as follows.

V0==85.71

第四年开始变化,我在第三年末划一刀,所以第三阶段我是用算成了PVRI4,即用RI4。

请问第四年开始变化,为什么是RI3?