问题如下:

Which of the following statements about the

liquidity in crisis situations is NOT correct?

选项:

A.When estimating the liquidity risks in crisis, model assumptions used in the normal markets are not appropriate.

B. To estimate the liquidity risk in crisis, we

could modify the parameters that account for crisis features, such as high

bid-ask spread and large losses.

We should estimate crisis liquidity based on

the normal market LaR.

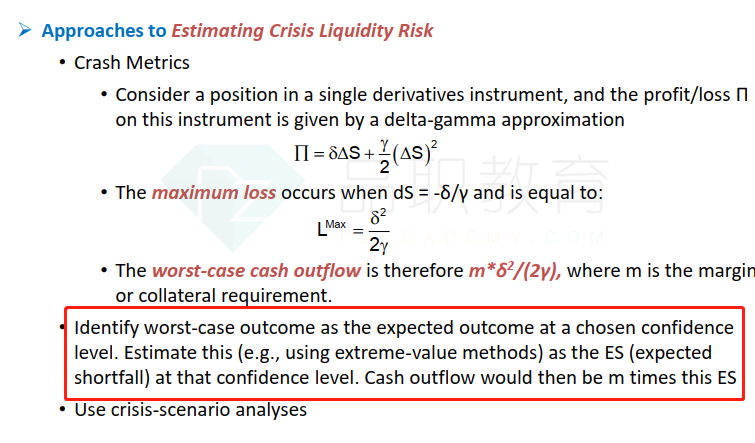

When estimating crisis liquidity risk, we can identify worst-case outcome as the expected outcome at a chosen confidence level.

解释:

考点:对Liquidity in Crisis Situations的理解

答案:C选项描述错误,本题选C

解析:

不能从Normal market的LaR来估算危机情景下的Liquidity risk,两个情景相互独立。

请问一下,D选项如何理解