问题如下:

1. The inclusion of index returns prior to 2001 would be expected to:

选项:

A.bias the historical equity risk premium estimate upwards.

B.bias the historical equity risk premium estimate downwards.

C.have no effect on the historical equity risk premium estimate.

解释:

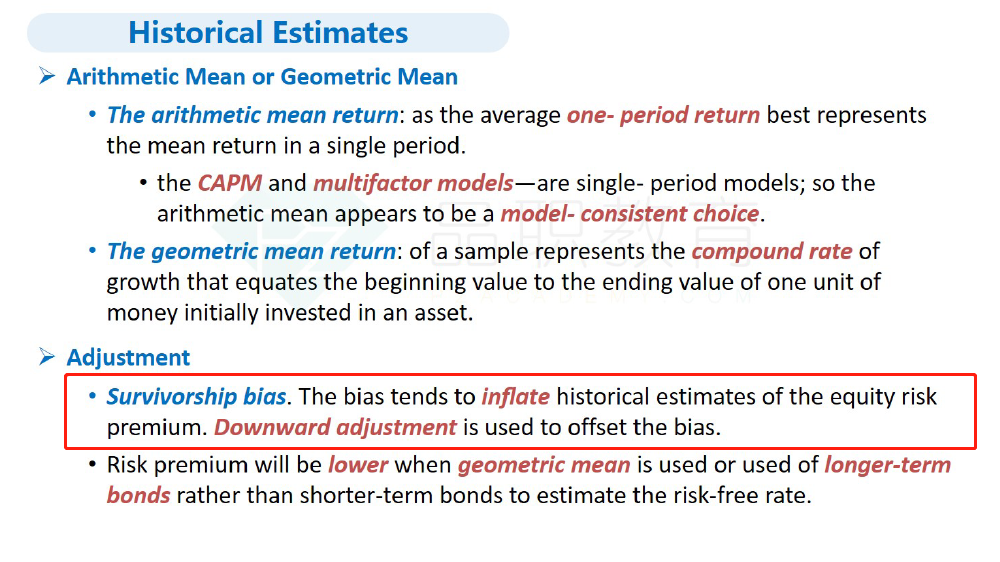

A is correct.

The backfilling of index returns using companies that have survived to the index construction date is expected to introduce a positive survivorship bias into returns.

请问老师这是哪里的知识点?谢谢