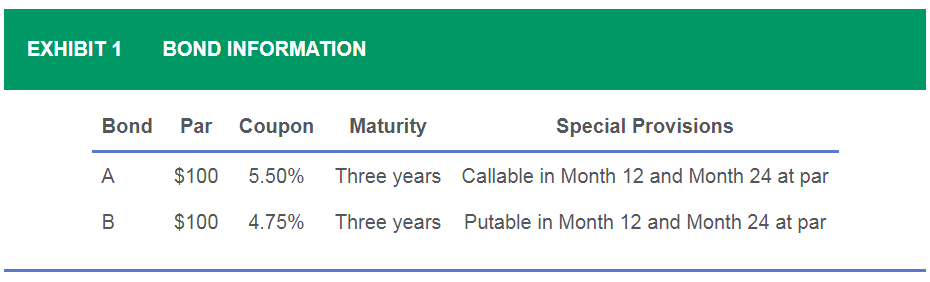

Scenario 2: Interest rate volatility remains at current levels, and the yield curve flattens further, with rates in the zero- to one-year maturity rising and rates in the two-year maturity and above declining.”

Q. If interest rates change as described in Scenario 2, it is most likely that Bond A:

- and Bond B will rise but more rapidly than the straight bond.

- will rise less rapidly than the straight bond and Bond B will rise more rapidly than the straight bond.

- and Bond B will rise but less rapidly than the straight bond.

长短期利率变化方向不同,对callable bond和putable bond的影响是?请结合这题目讲一下,同一个bond利率变化不同,不同类型含权债券的影响应该不一样吧?为什么答案是3