问题如下:

2. At a significance level of 1%, which of the following is the best interpretation of the regression coefficients with regard to explaining ROE?

选项: ESG is significant, but tenure is not.

Tenure is significant, but ESG is not.

C.Neither ESG nor tenure is significant.

解释:

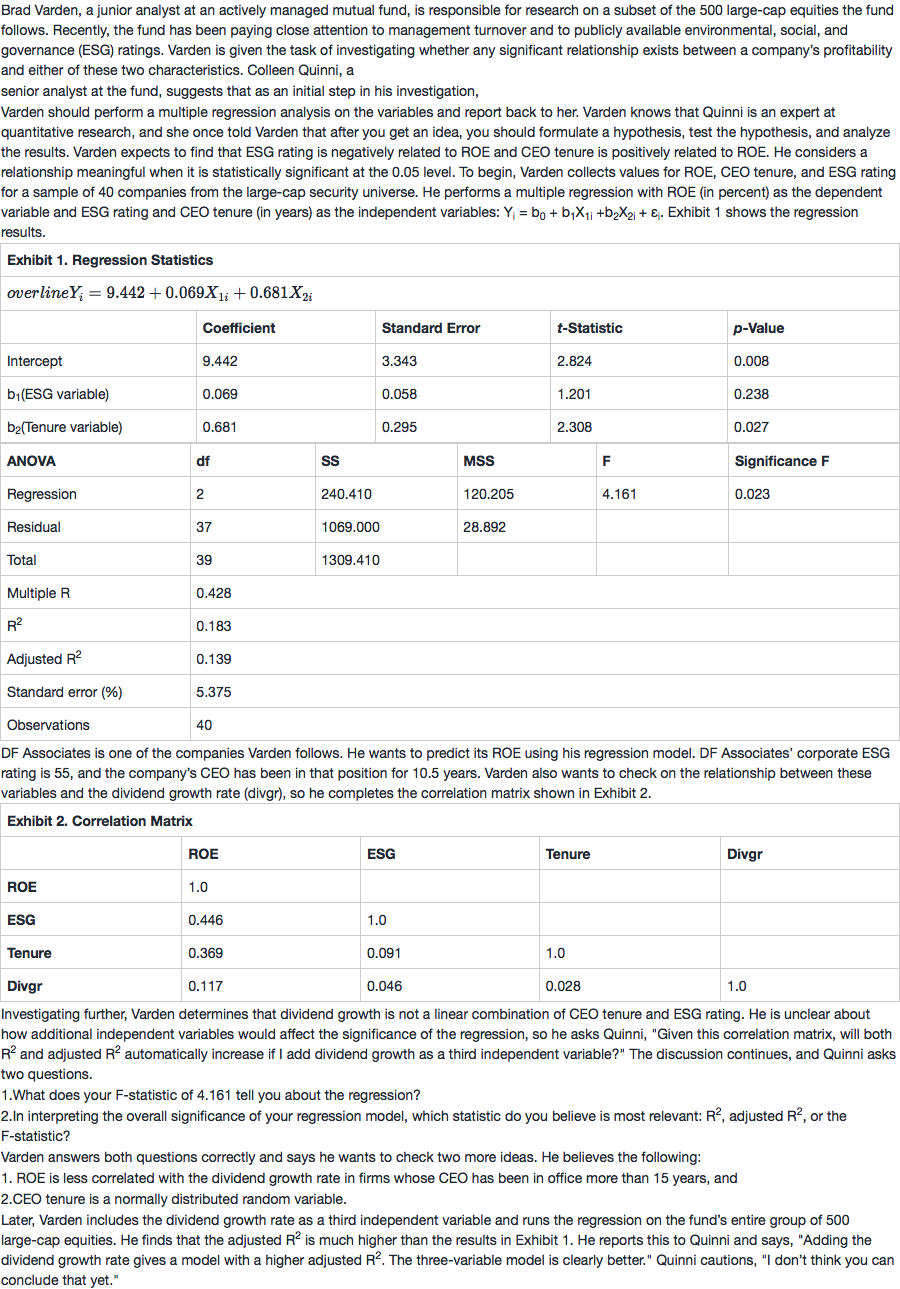

C is correct. The t-statistic for tenure is 2.308, indicating significance at the 0.027 level but not the 0.01 level. The t-statistic for ESG is 1.201, with a p-value of 0.238, which means we fail to reject the null hypothesis for ESG at the 0.01 significance level.

老师好, 这里题目要看这两个东西是否是显著的 所以原假设是该两个变量不显著 Ha是该两个变量是显著的是吗? Ha 一般是题目研究的东西 对吗? 谢谢。