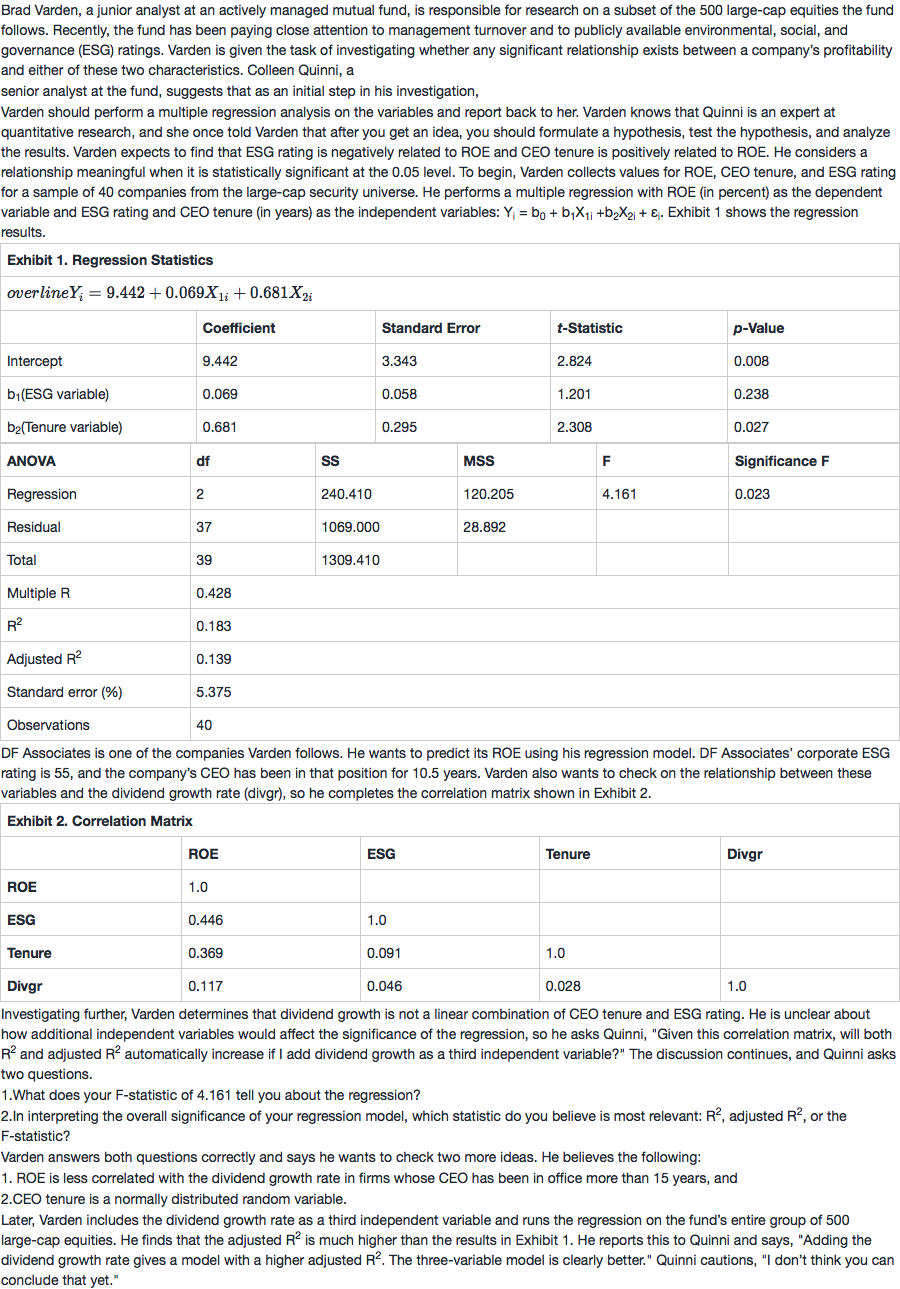

问题如下:

9.The best rationale for Quinni’s caution about the three-variable model is that the:

选项:

A.

dependent variable is defined differently.

B.

sample sizes are different in the two models.

C.

dividend growth rate is positively correlated with the other independent variables.

解释:

B is correct. If we use adjusted R2 to compare regression models, it is important that the dependent variable be defined the same way in both models and that the sample sizes used to estimate the models are the same. Varden’s first model was based on 40 observations, whereas the second model was based on 500.

这道题考点是什么?样本容量变大然后怎么了?