问题如下:

To what sort of option on the counterparty’s assets can the current exposure of a credit-risky position better be compared?

选项: A. A

short call

B. A

short put

C. A

short knock-in call

D. A

binary option

解释:

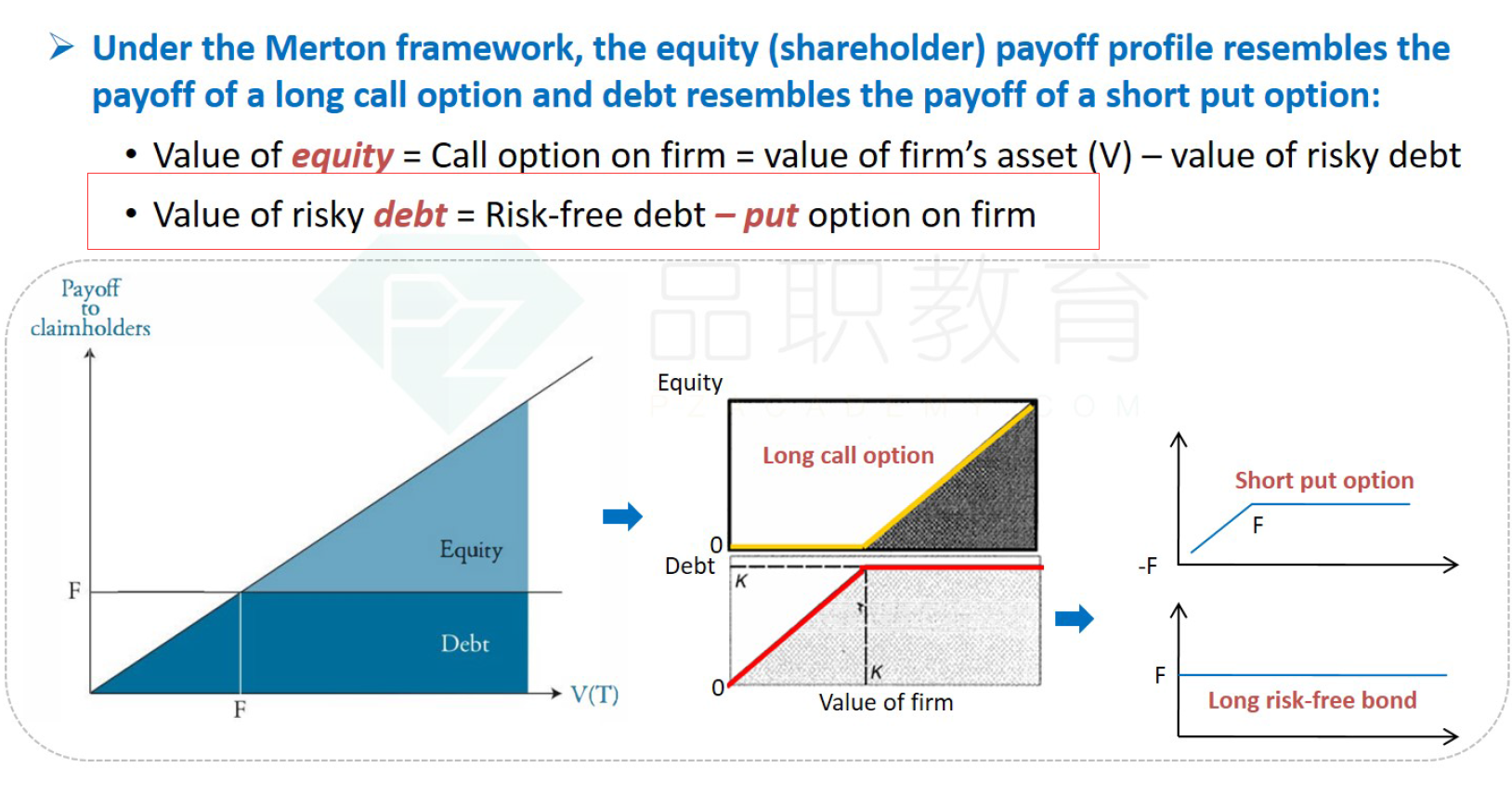

ANSWER: B

The lender is short a put option, since exposure exists only if the value of assets falls below the amount lent.

这道题的题干到底想表达啥。。。。。。