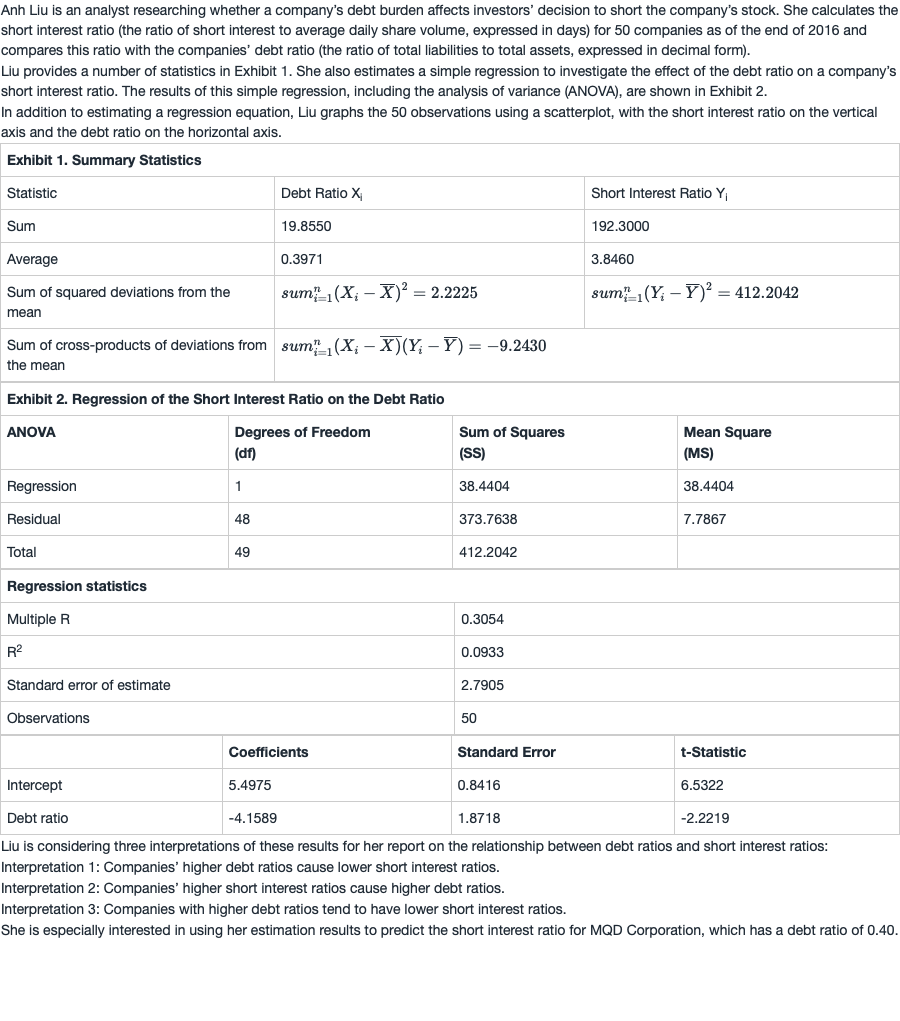

问题如下:

3. Based on Exhibit 1, the correlation between the debt ratio and the short interest ratio is closest to:

选项:

A.−0.3054.

B.0.0933.

C.0.3054.

解释:

A is correct.

The correlation coefficient equals the covariance between

variables X and Y divided by the product of the standard deviations of

variables X and Y, as follows:

老师,在线性回归方程里,自变量X和因变量Y的相关系数,不是等于cov(x,y)/x的方差吗?在计算样本时,成了cov(x,y)/(x的标准差✖y的标准差)了呢