问题如下:

a. Calculate the time series for the following AR(1) model, taking .

选项:

解释:

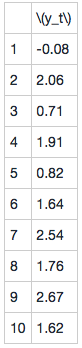

Each value is generated via the formula:

y1 = 0.5 + 0.75 * 0 - 0.58 = -0.08

y2 = 0.5 + 0.75 * (-0.08) + 1.62 = 2.12

and so forth.

这三道题答案框里是在计算什么?是怎么计算的到的?

比如世界 · 2020年03月29日

* 问题详情,请 查看题干

问题如下:

a. Calculate the time series for the following AR(1) model, taking .

选项:

解释:

Each value is generated via the formula:

y1 = 0.5 + 0.75 * 0 - 0.58 = -0.08

y2 = 0.5 + 0.75 * (-0.08) + 1.62 = 2.12

and so forth.

这三道题答案框里是在计算什么?是怎么计算的到的?

NO.PZ202001110100001301问题如下Calculate the time series for the following AR(1) mol, taking y0=0,δ=0.5,an=0.75y_0 = 0, \lta = 0.5, an\phi = 0.75y0=0,δ=0.5,an=0.75.Yt=δ+ϕYt−1+ϵtY_t = \lta + \phi_{Y_{t - 1} + \epsilon_t} Yt=δ+ϕYt−1+ϵtEavalue is generatevia the formula:y1 = 0.5 + 0.75 * 0 - 0.58 = -0.08y2 = 0.5 + 0.75 * (-0.08) + 1.62 = 2.12anso forth.我不理解的是,他有0.5这一项了,y取啥他都不能变成0啊

NO.PZ202001110100001301 这里没有给残差项吧?

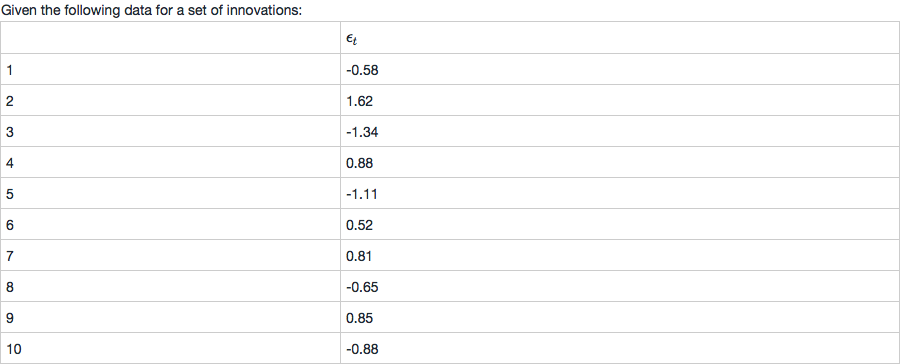

NO.PZ202001110100001301 公式中最后的残差项Et是怎么看表出来的?为什么E1=-0.58,E2=1.62

如果是后面的小问,也是先写出对应的递推公式,再一步步把数字带进去进行计算就行了。

如果是后面的小问,也是先写出对应的递推公式,再一步步把数字带进去进行计算就行了。