问题如下:

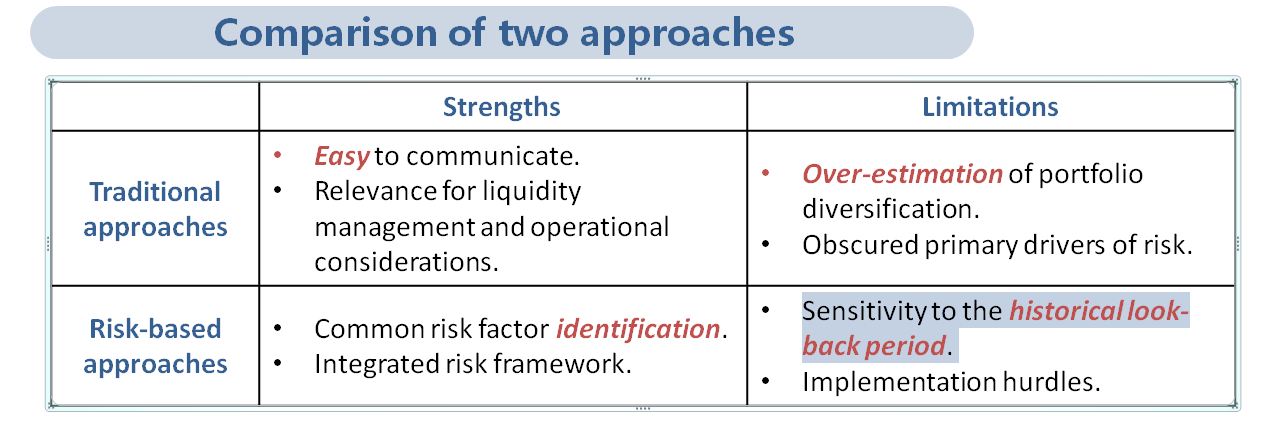

What of the following is the drawback of risk-based approach to asset classification?

选项:

A.It overestimates the portfolio diversification.

It is sensitive to historical look-back period.

It has united risk factor identification.

解释:

B is correct.

The major drawback of risk factor based approach is that it depends on the histocial data and the sepecific data period.

老师, 可以解释一下为什么这个approach会对historical look back period 很敏感?