问题如下:

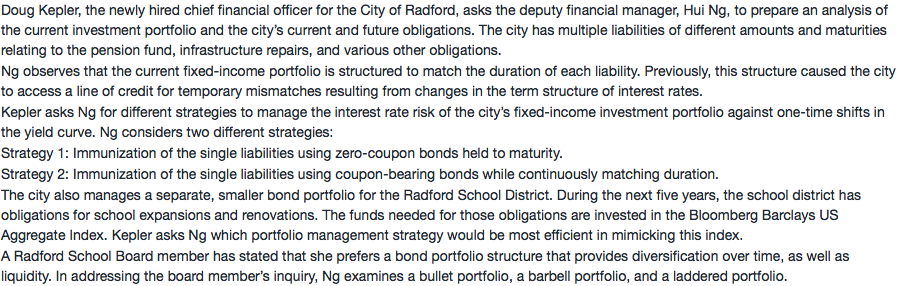

Ng’s response to Kepler’s question about the most efficient portfolio management strategy should be:

选项:

A.full replication.

B.active management.

C.an enhanced indexing strategy

解释:

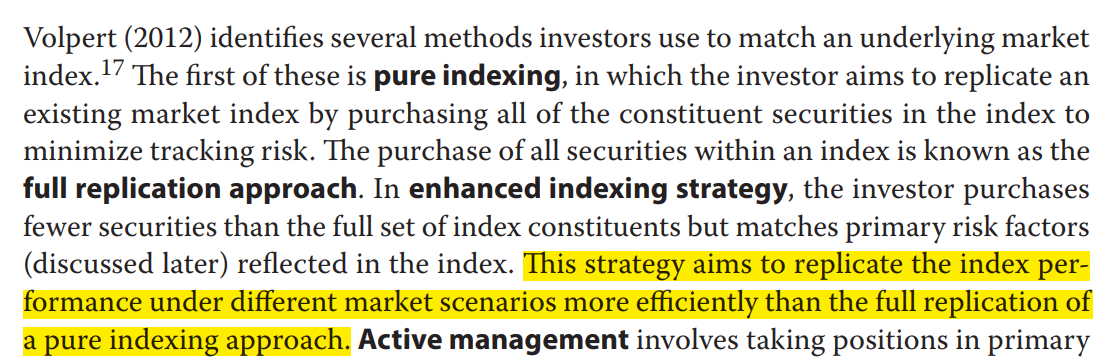

C is correct.

Under an enhanced indexing strategy, the index is replicated with fewer than the full set of index constituents but still matches the original index’s primary risk factors. This strategy replicates the index performance under different market scenarios more efficiently than the full replication of a pure indexing approach.

老师 题目中说 Kepler asks Ng which portfolio management strategy would be most efficient in mimicking this index.那么最有效的模拟方式不是就是 full replicated么?