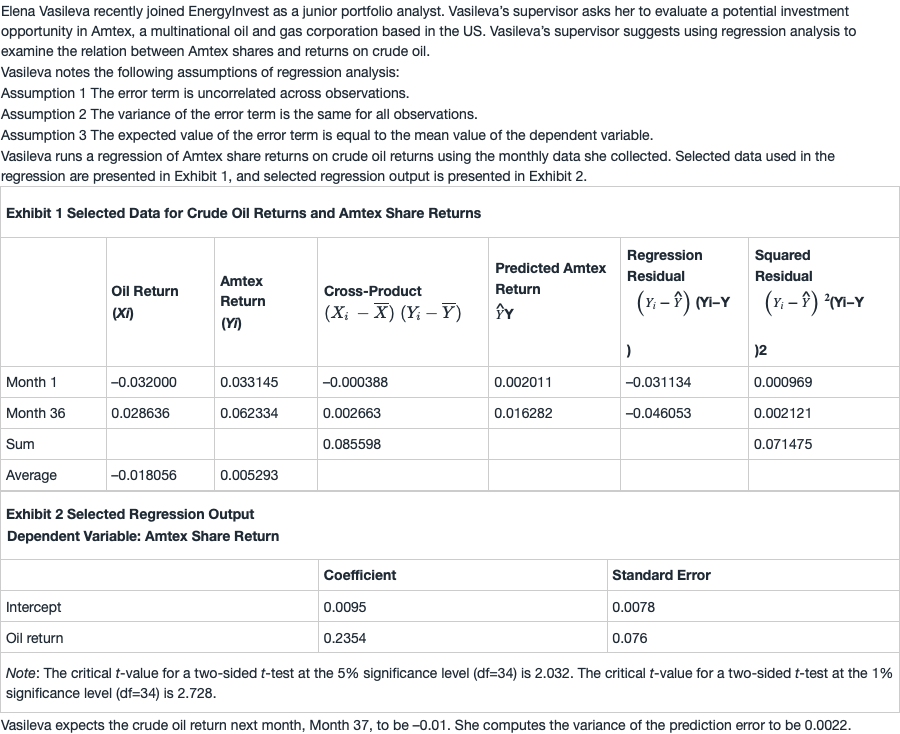

问题如下:

Using information from Exhibit 2, Vasileva should compute the 95% prediction interval for Amtex share return for month 37 to be:

选项:

A.–0.0882 to 0.1025.

–0.0835 to 0.1072.

0.0027 to 0.0116.

解释:

A is correct.

能否给详细过程?

NO.PZ201512020300000806 如果题目问求95% intervof slope (oil return),就直接用表格中0.2354+/-1.96*0.046来算吗? 如何判断题目问的到底是95% of Y 还是表格中的 oil return (b1)呢?表格中b1和Y都叫做oil return

NO.PZ201512020300000806 –0.0835 to 0.1072. 0.0027 to 0.0116. A is correct. The 95% prection iintervfor the pennt variable given a certain value of the inpennt variable is calculateas: Prection interv= Y^±tcsf\wihat{Y}\pm{t_{c}s_f}Y ±tcsf anthe prectevalue Y^=b^0+b^1Xi\wihat{Y}=\wihat{b}_0+\wihat{b}_1X_iY =b 0+b 1Xi Therefore: Prectevalue = 0.0095 + (0.2354 × (–0.01)) = 0.0071 sf=0.00220.5=0.0469s_f={0.0022}^{0.5}=0.0469sf=0.00220.5=0.0469 tc=2.032t_c=2.032tc=2.032 The lower limit for the prection interv= 0.0071 – (2.032 × 0.0469) = –0.0882 The upper limit for the prection interv= 0.0071 + (2.032 × 0.0469) = 0.1025 2.032怎么来的,谢谢

计算过程可以给下吗?

计算过程可以给一下吗 没算对

为什么不用=35的2.03要用=34的 2.032 样本不是变成37个了吗?