问题如下图:

选项:

A.

B.

C.

D.

解释:

老师,此题具体是巴1的哪个考点?

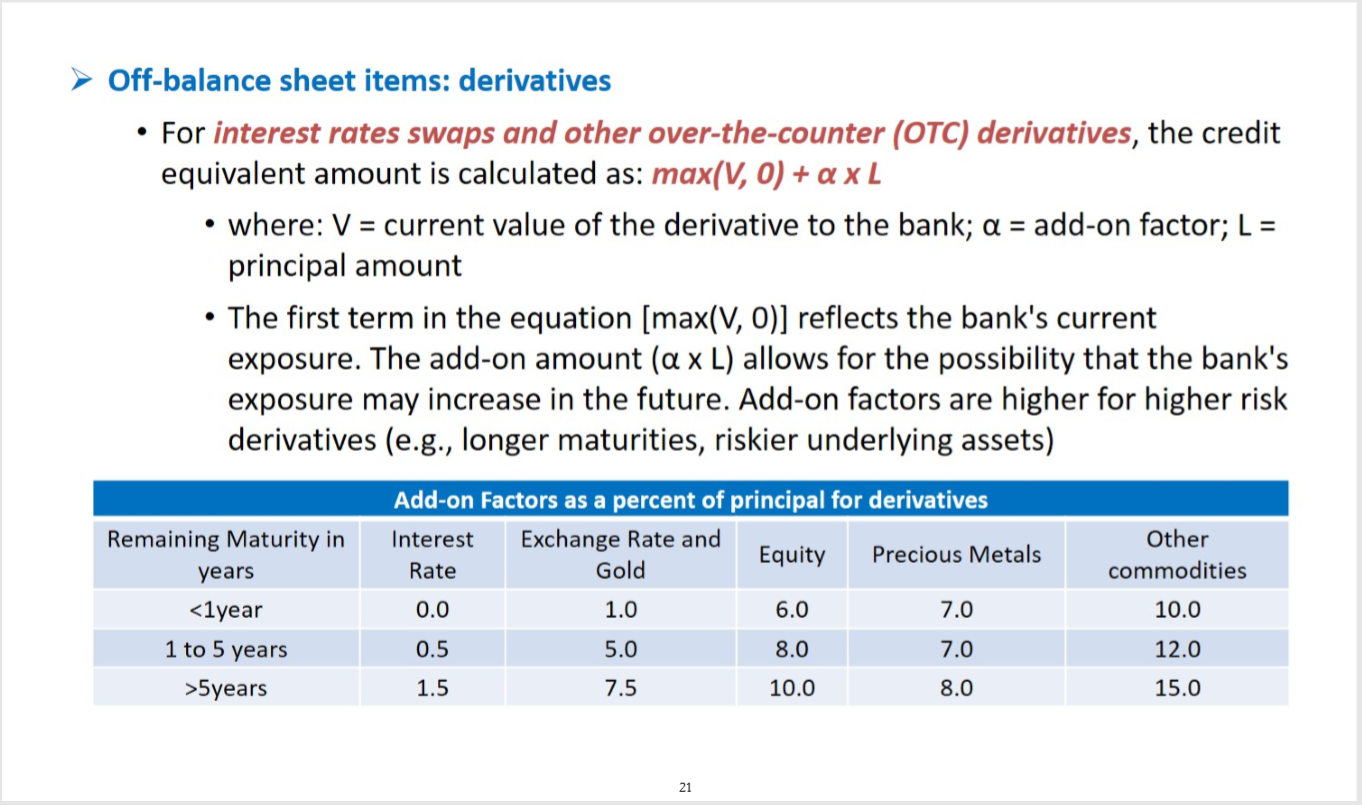

NO.PZ2016072602000048 问题如下 Therivatives book of internationbank contains $300 millionofnotionvalue of interest rate swaps with $100 million eahavingremaining maturity of 0.5, 1.5 an2.5 years. Their market value is $30 million.The bookalso h$300 million of foreign exchange swaps with a similmaturity profile ana market value of -$10 million.All counterpartiesare private corporations, so the risk weight is 100 percent. Calculate the cretequivalent amount unr the originalexposure metho A.$18.5million B.$42 million C.$35 million $26 million A is correct. Unrtheoriginexposure metho it woulbe:CEA=0.5%x 100+1%× 100+2%×100+2%×100+5%×100 +8%×100 = $18.5 million 如题

NO.PZ2016072602000048 问题如下 Therivatives book of internationbank contains $300 millionofnotionvalue of interest rate swaps with $100 million eahavingremaining maturity of 0.5, 1.5 an2.5 years. Their market value is $30 million.The bookalso h$300 million of foreign exchange swaps with a similmaturity profile ana market value of -$10 million.All counterpartiesare private corporations, so the risk weight is 100 percent. Calculate the cretequivalent amount unr the originalexposure metho A.$18.5million B.$42 million C.$35 million $26 million A is correct. Unrtheoriginexposure metho it woulbe:CEA=0.5%x 100+1%× 100+2%×100+2%×100+5%×100 +8%×100 = $18.5 million 1+1*int(m-1)取整不是3吗。。m-1=1.5 离2最近,1+2=3

NO.PZ2016072602000048 问题如下 Therivatives book of internationbank contains $300 millionofnotionvalue of interest rate swaps with $100 million eahavingremaining maturity of 0.5, 1.5 an2.5 years. Their market value is $30 million.The bookalso h$300 million of foreign exchange swaps with a similmaturity profile ana market value of -$10 million.All counterpartiesare private corporations, so the risk weight is 100 percent. Calculate the cretequivalent amount unr the originalexposure metho A.$18.5million B.$42 million C.$35 million $26 million A is correct. Unrtheoriginexposure metho it woulbe:CEA=0.5%x 100+1%× 100+2%×100+2%×100+5%×100 +8%×100 = $18.5 million int【m-a】是什么意思,两个int【x】计算下来都是1?

NO.PZ2016072602000048 问题如下 Therivatives book of internationbank contains $300 millionofnotionvalue of interest rate swaps with $100 million eahavingremaining maturity of 0.5, 1.5 an2.5 years. Their market value is $30 million.The bookalso h$300 million of foreign exchange swaps with a similmaturity profile ana market value of -$10 million.All counterpartiesare private corporations, so the risk weight is 100 percent. Calculate the cretequivalent amount unr the originalexposure metho A.$18.5million B.$42 million C.$35 million $26 million A is correct. Unrtheoriginexposure metho it woulbe:CEA=0.5%x 100+1%× 100+2%×100+2%×100+5%×100 +8%×100 = $18.5 million 请问该类题目如何具体做呢,这些个系数是从哪里来的,A ON factor?该类题目如何计算VALUE 呢

NO.PZ2016072602000048 问题如下 Therivatives book of internationbank contains $300 millionofnotionvalue of interest rate swaps with $100 million eahavingremaining maturity of 0.5, 1.5 an2.5 years. Their market value is $30 million.The bookalso h$300 million of foreign exchange swaps with a similmaturity profile ana market value of -$10 million.All counterpartiesare private corporations, so the risk weight is 100 percent. Calculate the cretequivalent amount unr the originalexposure metho A.$18.5million B.$42 million C.$35 million $26 million A is correct. Unrtheoriginexposure metho it woulbe:CEA=0.5%x 100+1%× 100+2%×100+2%×100+5%×100 +8%×100 = $18.5 million 请问老师,品职出的这道题和原版书上的题目,哪里有不同啊?为什么这道题不用加上value