问题如下图:

选项:

A.

B.

C.

解释:

老师,您好!这题我得出结果是C,我是这样做的:

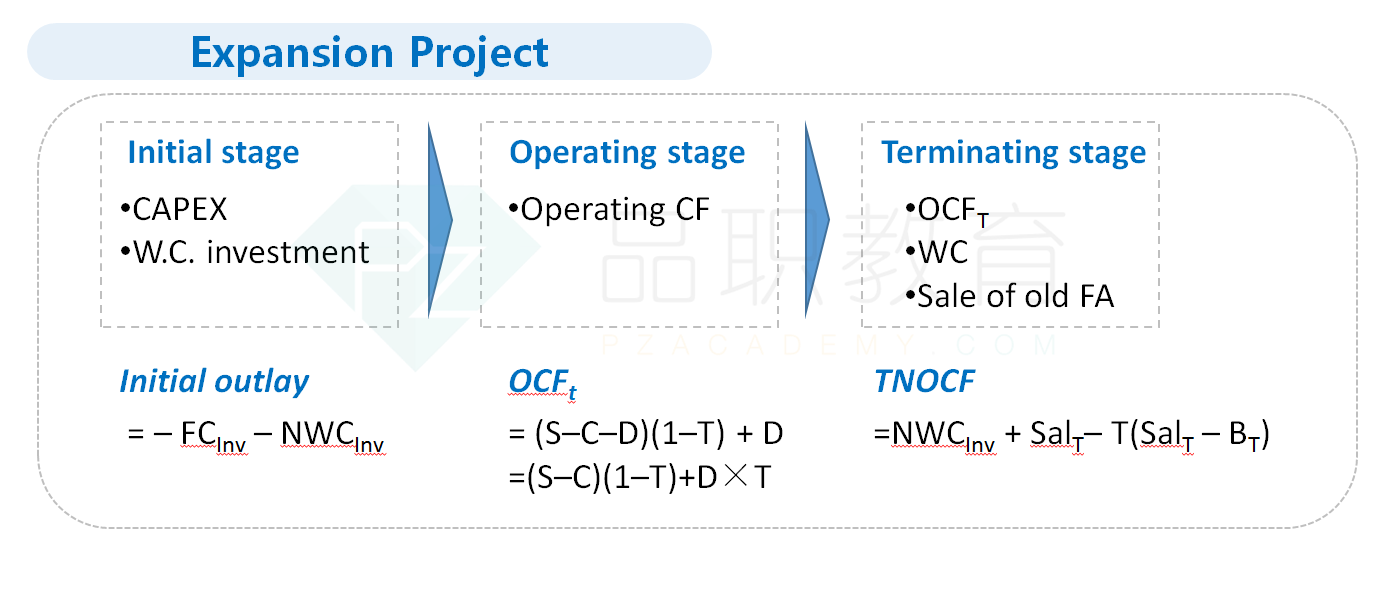

FCFF=(EBITDA-DEP)*(1-T)+DEP-WC-FC。因为只是调增了期初的FC支出,所以OCF=(-100000/8)*(1-40%)+100000/8=7500,然后在此基础上折现,得出结果C。

请问我的过程哪里有问题呢?谢谢!

NO.PZ2016012005000002 问题如下 After estimating a project’s NPV, the analyst is aiseththe fixecapitoutlwill reviseupwar$100,000. The fixecapitoutlis preciatestraight-line over eight-yelife. The trate is 40 percent anthe requirerate of return is 10 percent. No changes in cash operating revenues, cash operating expenses, or salvage value are expecte Whis the effeon the projeNPV? A.$100,000 crease. B.$73,325 crease. C.$59,988 crease. B is correct.The aitionannupreciation is $100,000/8 = $12,500. The preciation tsavings is 0.40 ($12,500) = $5,000. The change in projeNPV is−100,000+∑t=185,000(1.10)t=−100,000+26,675=−$73,325-100,000+\sum_{t=1}^8\frac{5,000}{{(1.10)}^t}=-100,000+26,675=-\$73,325−100,000+∑t=18(1.10)t5,000=−100,000+26,675=−$73,325 如题

NO.PZ2016012005000002 辅导员好,根据公式(S-C-*(1-t) + 5000只是每年的折旧的金额12500*40%后得到的吧,为什么后面不需要再+12500

$73,325 crease. $59,988 crease. B is correct. The aitionannupreciation is $100,000/8 = $12,500. The preciation tsavings is 0.40 ($12,500) = $5,000. The change in projeNPV is −100,000+∑t=185,000(1.10)t=−100,000+26,675=−$73,325-100,000+\sum_{t=1}^8\frac{5,000}{{(1.10)}^t}=-100,000+26,675=-\$73,325−100,000+∑t=18(1.10)t5,000=−100,000+26,675=−$73,325计算器怎么算5000的8年折现。麻烦问怎么按计算器

本题数据都算的明白,问题出现在符号上。 我的理解是 开始的CAPEX加回100,000。那刚开始减多了,现在加回,对应的NPV不应该是增加吗? 同样,放开始CAPEX多了,我算的p多了,实际没有那么多,所以我的那些p的折现求和不应该是减去吗? 所以正好和题目的符号是反着的,想问问逻辑上存在什么错误。谢谢~~

最后一期变卖固定资产的时候,不用增加额外的现金流吗?虽然说残值不变,但是只是影响BV,MV也应该增加100000才合适吧?还是默认没有处置?