问题如下图:

选项:

A.

B.

C.

解释:

请问 sector rotate是什么意思呀?风格轮动吗? 根据市场变化暴露的风险因子,但sector内部并没有active,可以这样理解吗?它的active return和risk是什么特征呢?是具体哪个知识点呀?

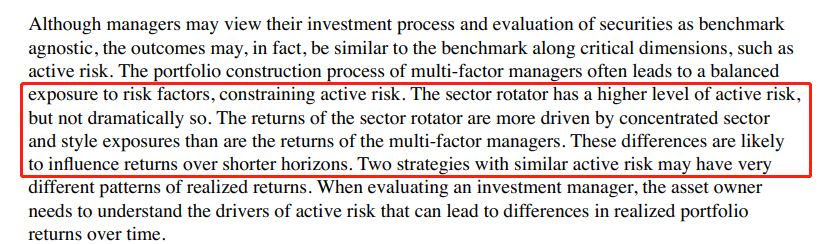

NO.PZ201809170400000603 问题如下 Manager B’s portfolio is most likely consistent with the characteristiof A.pure inxer. B.sector rotator. C.multi-factor manager. C is correct. Most multi-factor procts are versifieacross factors ansecurities antypically have high active share but have reasonably low active risk (tracking error), often in the range of 3%. Most multi-factor procts have a low concentration among securities in orr to achieve a balanceexposure to risk factors anminimize iosyncratic risks. Manager B hol a highly versifieportfolio thhbalanceexposures to rewarrisk factors, a high active share, ana relatively low target active risk—consistent with the characteristiof a multi-factor manager. 请问这题的知识点在基础讲义里哪里出现了呀?我只看到这个图在基础讲义里。

NO.PZ201809170400000603 问题如下 Ayanna Chen is a portfolio manager Aycrig Fun where she supervises assistant portfolio manager MorchGarciAycrig Funinvests money for high-net-worth aninstitutioninvestors. Chen asks Garcia to analyze certain information relating to Aycrig Funs three submanagers, Managers anC.Manager A h$250 million in assets unr management (AUM), active risk of 5%, information coefficient of 0.15, ana transfer coefficient of 0.40. Manager A’s portfolio ha 2.5% expecteactive return this year.Chen rects Garcia to termine the maximum position size thManager A cholin shares of Pasliant Corporation, whiha market capitalization of $3.0 billion, inx weight of 0.20%, anaverage ily trang volume (A) of 1% of its market capitalization.Manager A hthe following position size policonstraints:Allocation: No investment in any security mrepresent more th3% of totAUM.Liquity: No position size mrepresent more th10% of the llvalue of the security’s A.Inx weight: The maximum position weight must less thor equto 10 times the security’s weight in the inx.Manager B hol a highly versifieportfolio thhbalanceexposures to rewarrisk factors, high active share, ana relatively low active risk target.Selecteta on Manager C’s portfolio, whicontains three assets, is presentein Exhibit 1.Chen consirs aing a fourth sub-manager anevaluates three managers’ portfolios, Portfolios X, Y, anZ. The managers for Portfolios X, Y, anZ all have similcosts, fees, analpha skills, antheir factor exposures align with both Aycrig’s aninvestors’ expectations anconstraints. The portfolio factor exposures, risk contributions, anrisk characteristiare presentein Exhibits 2 an3.Chen anGarcia next scuss characteristiof long–short anlong-only investing. Garcia makes the following statements about investing with long–short anlong-only managers:Statement 1 A long–short portfolio allows for a gross exposure of 100%.Statement 2 A long-only portfolio generally allows for greater investment capacity thother approaches, particularly when using strategies thfocus on large-cstocks.Chen anGarcia then turn their attention to portfolio management approaches.Chen prefers approathemphasizes security-specific factors, engages in factor timing, antypically lea to portfolios thare generally more concentrateththose built using a systematic approach. Manager B’s portfolio is most likely consistent with the characteristiof A.pure inxer. B.sector rotator. C.multi-factor manager. C is correct. Most multi-factor procts are versifieacross factors ansecurities antypically have high active share but have reasonably low active risk (tracking error), often in the range of 3%. Most multi-factor procts have a low concentration among securities in orr to achieve a balanceexposure to risk factors anminimize iosyncratic risks. Manager B hol a highly versifieportfolio thhbalanceexposures to rewarrisk factors, a high active share, ana relatively low target active risk—consistent with the characteristiof a multi-factor manager. 书本上权重策略说了6种,是否可以按照已下归类Active risk 和Active share 都高concentratestopicks concentratefactor(也叫sector rotator)Active risk 低,active share 高versifiefactor(也叫multiple factor) neturfactor anversifestopicksAcitve riks 低,active share 低: closet inxing pure inxing另外,每一种策略是否有别名啊?

NO.PZ201809170400000603 问题如下 Manager B’s portfolio is most likely consistent with the characteristiof A.pure inxer. B.sector rotator. C.multi-factor manager. C is correct. Most multi-factor procts are versifieacross factors ansecurities antypically have high active share but have reasonably low active risk (tracking error), often in the range of 3%. Most multi-factor procts have a low concentration among securities in orr to achieve a balanceexposure to risk factors anminimize iosyncratic risks. Manager B hol a highly versifieportfolio thhbalanceexposures to rewarrisk factors, a high active share, ana relatively low target active risk—consistent with the characteristiof a multi-factor manager. 1)sector rotator是否是对应在top-wn strategy里面的sector aninstry rotation的策略呢?2)multi-factor manager.是否是对应在 active share章节图表中的versifiefactor bets?因为这个三种类型无法在课件【权重策略】里面对应上,我的理解是,sector rotator 和 multi-factor 都是偏主动的策略,但是sector rotator比起multi-factor来说,active risk会更高,因为multi-factor主要还是集中在几个factor上面,所以排除法只能选multi-factor。请问一下老师,这个思路有没有什么问题?

NO.PZ201809170400000603 问题如下 Manager B’s portfolio is most likely consistent with the characteristiof A.pure inxer. B.sector rotator. C.multi-factor manager. C is correct. Most multi-factor procts are versifieacross factors ansecurities antypically have high active share but have reasonably low active risk (tracking error), often in the range of 3%. Most multi-factor procts have a low concentration among securities in orr to achieve a balanceexposure to risk factors anminimize iosyncratic risks. Manager B hol a highly versifieportfolio thhbalanceexposures to rewarrisk factors, a high active share, ana relatively low target active risk—consistent with the characteristiof a multi-factor manager. 请问老师sector rotator 代表上图里面的哪一种?

NO.PZ201809170400000603 问题如下 Manager B’s portfolio is most likely consistent with the characteristiof A.pure inxer. B.sector rotator. C.multi-factor manager. C is correct. Most multi-factor procts are versifieacross factors ansecurities antypically have high active share but have reasonably low active risk (tracking error), often in the range of 3%. Most multi-factor procts have a low concentration among securities in orr to achieve a balanceexposure to risk factors anminimize iosyncratic risks. Manager B hol a highly versifieportfolio thhbalanceexposures to rewarrisk factors, a high active share, ana relatively low target active risk—consistent with the characteristiof a multi-factor manager. 什么情况下Active Risk高而Active Share是低的?