问题如下图:

选项:

A.

B.

C.

解释:

老师,您好!这道题我确实知道了短期违约风险上升,但是为何credit curve是向下呢?请问基础班对应的知识点在哪里?谢谢!

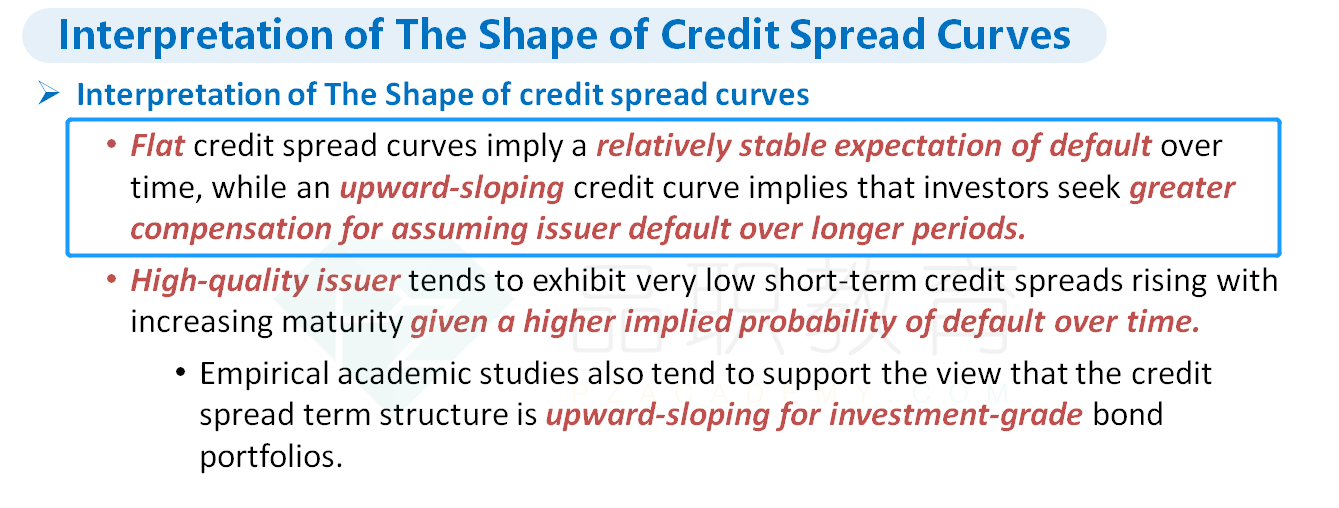

NO.PZ201701230200000602 问题如下 2. Accorng to Watt’s statement, the shape of UNAB’s cret curve is most likely: A.flat. B.upwarsloping. C.wnwarsloping. C is correct.A wnwarsloping cret curve implies a greater probability of fault in the earlier years thin the later years. wnwarsloping curves are less common anoften are the result of severe near-term stress in the financimarkets.A is incorrebecause a flcret curve implies a constant hazarrate (relevant probability of fault). B is incorrebecause upwarsloping cret curve implies a greater probability of fault in later years. 如果是一个正常的情况,曲线应该是上升的,就是时间越远不确定的因素越大,流动性越小,所以是upwarsloping,人们需要更强多的补偿。但这里是near-term crisis,所以就是近期发生风险的概率打,然后人们需要的补偿多,所以就是近期的补偿会高于远期,然后就是wnwarsloing。

NO.PZ201701230200000602 最后一句话是表示什么意思?

老师,A如果改成 flatter,是不是就对了呢?我是这么想的,我认为,一般情况下cret curve是向上倾斜的(即长期的cret sprea于短期的cret sprea,既然短期的经济不好违约概率提升,相当于短期的cret sprea升,在图上表现为短端向上,曲线变更flat了。但是不能知道是不是变成了wnwar-sloping。这是我想的。但是答案很明显是理解fl为“全线是水平”对吗?应该怎么理解?我的误区在哪里?