问题如下图:

选项:

A.

B.

C.

解释:

根据题目,investment1都是两年期的投资,并没有说明要买一个年限更长的bond,所以就算要riding the yield curve,它的return不是和一个maturity matching的return一样吗?选B才对?

根据题目,investment1都是两年期的投资,并没有说明要买一个年限更长的bond,所以就算要riding the yield curve,它的return不是和一个maturity matching的return一样吗?选B才对?

吴昊_品职助教 · 2019年03月25日

a two-year investment这代表的是一个两年期的投资,a combination of two one-year investment,代表的是两个一年期投资的组合。

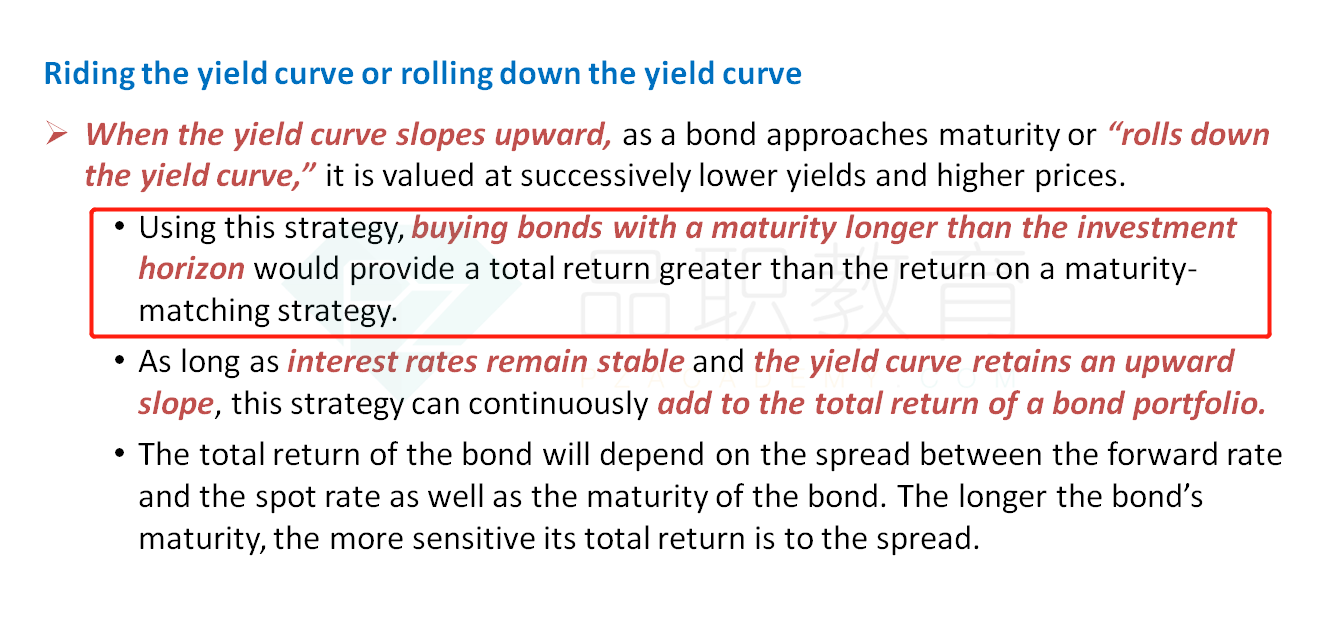

其实这道题目就是让我们基于S同学对于利率的看法,判断一下riding the yield curve策略和maturity-matching策略哪一个的收益更大。根据表1可以看到收益率曲线是向上倾斜的。同时题干第一段最后一句S同学预期收益率曲线是stable的,这两点就满足了riding the yield curve。而riding the yield curve策略相比maturity-matching策略,capital gain会更大,因此收益更大。

比如投资期为五年,我们做期限匹配策略,购买一个五年期债券并持有至到期,capital gain为0.

riding the yield curve策略,我们购买一个30年期债券并在第5年末卖出。第五年年末的时候,30年债券就变成了一个25年期债券,因此做这个策略的capital gain=P(25)-P(30)>0,25年期相比30年期的收益率更低,价格更高。所以两个价格做差是大于0的。

因此,riding the yield curve策略相比maturity-matching策略,capital gain会更大,因此收益更大。具体参考基础班讲义P21页。

NO.PZ201701230200000202 问题如下 2. In presenting Investment 1, using Shire Gate Aisers’ interest rate outlook, Smith coulshow thring the yielcurve provis a totreturn this most likely: A.lower ththe return on a maturity-matching strategy. B.equto the return on a maturity-matching strategy. C.higher ththe return on a maturity-matching strategy. C is correct.When the spot curve is upwarsloping anits level anshape are expecteto remain constant over investment horizon (Shire Gate Aisers’ view), buying bon with a maturity longer ththe investment horizon (i.e., ring the yielcurve) will provi a totreturn greater ththe return on a maturity-matching strategy. Shire Gate Aisers recently publishea report for its clients stating its belief that, baseon the weakness in the financimarkets, interest rates will remain stable, the yielcurve will not change its level or shape for the next two years, answsprea will also remain unchange这段描述哪里提到收益率曲线向上倾斜?

NO.PZ201701230200000202 我以为是yielcurve 不会upwar会是flat的,所以就选择return 低于。所以stable unchange的意思就是upwar嘛

我觉得这道题和上课讲的例题原理是不一样的。 上课讲的题,是把 A.投资期 5 年,持有 5 年,和 投资期 30 年,持有 5 年对比,这样ring the yielcurve 就有更多收益 这道题是,把 A.投资期 2 年,持有 2 年,和 投资期 2 年,持有 1 年对比.投资期其实是一样长的,根据无套利原理,其实这种情况下 ring the yielcurve 和 matching-maturity 收益应该是一样的。 所以这道题应该选 B 不是吗

请问这个知识点在强化班哪个视频里提到的?

请问这个知识点在强化班哪个视频里?