问题如下图:

选项:

A.

B.

C.

D.

解释:

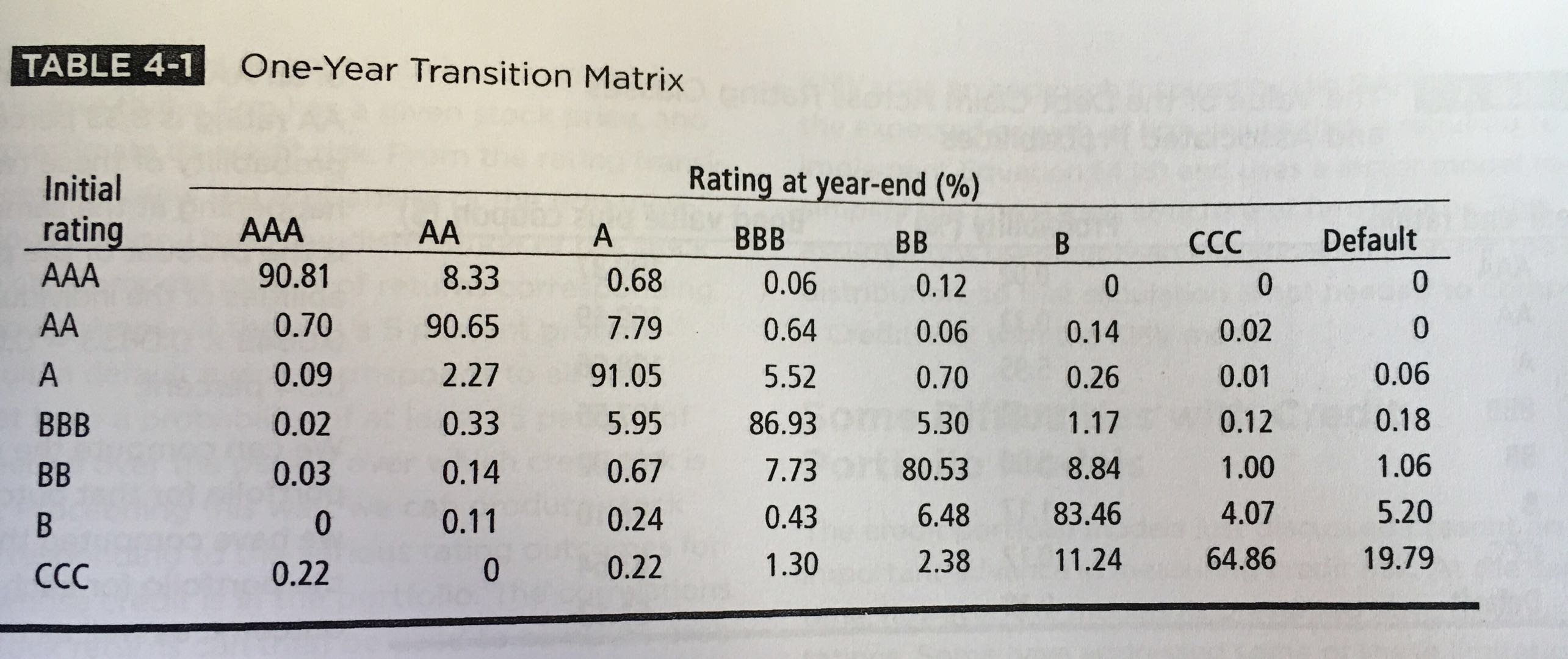

对于A选项的解释不太明白,信用转移矩阵为什么衡量的是unchange呢?

NO.PZ2016082405000025 Whiof the following statements regarng ratings transition matrices is least correct? Transition matrices assess rating migrations, this, the probability tha company starting with a particulrating will wngrawithin the stateperio The agonelements in the transition matrix beginning the top left show the probability of enng the yewith unchangerating. Within a transition matrix, there is no transition from fault to another rating. The probability of a rating migration is higher for lower ratecompanies. A Transition matrices assess the probability tha company’s rating will remain unchangethe enof a stateperio Rating migration measures the probability of a change in letter rating, however it encompasses both rating upgras anwngras. 请问b说的是什么意思?

Whiof the following statements regarng ratings transition matrices is least correct? Transition matrices assess rating migrations, this, the probability tha company starting with a particulrating will wngrawithin the stateperio The agonelements in the transition matrix beginning the top left show the probability of enng the yewith unchangerating. Within a transition matrix, there is no transition from fault to another rating. The probability of a rating migration is higher for lower ratecompanies. A Transition matrices assess the probability tha company’s rating will remain unchangethe enof a stateperio Rating migration measures the probability of a change in letter rating, however it encompasses both rating upgras anwngras. 什么是正确的呢 对于一个坏人来说再坏也坏不到哪里去 所以他的信用转移概率应该是小啊 想转移到好的rating的概率也不会很高

Whiof the following statements regarng ratings transition matrices is least correct? Transition matrices assess rating migrations, this, the probability tha company starting with a particulrating will wngrawithin the stateperio The agonelements in the transition matrix beginning the top left show the probability of enng the yewith unchangerating. Within a transition matrix, there is no transition from fault to another rating. The probability of a rating migration is higher for lower ratecompanies. A Transition matrices assess the probability tha company’s rating will remain unchangethe enof a stateperio Rating migration measures the probability of a change in letter rating, however it encompasses both rating upgras anwngras. 老师A是不是错在,不只是wn,up也可以

The agonelements in the transition matrix beginning the top left show the probability of enng the yewith unchangerating. Within a transition matrix, there is no transition from fault to another rating. The probability of a rating migration is higher for lower ratecompanies. A Transition matrices assess the probability tha company’s rating will remain unchangethe enof a stateperio Rating migration measures the probability of a change in letter rating, however it encompasses both rating upgras anwngras. 能解读哈?为什么是对的

Whiof the following statements regarng ratings transition matrices is least correct? Transition matrices assess rating migrations, this, the probability tha company starting with a particulrating will wngrawithin the stateperio The agonelements in the transition matrix beginning the top left show the probability of enng the yewith unchangerating. Within a transition matrix, there is no transition from fault to another rating. The probability of a rating migration is higher for lower ratecompanies. A Transition matrices assess the probability tha company’s rating will remain unchangethe enof a stateperio Rating migration measures the probability of a change in letter rating, however it encompasses both rating upgras anwngras. bonfault就真的再也没有任何机会在转移到其他评级了吗?????