请问这个知识点在书上哪里?问题如下图:

选项:

A.

B.

C.

D.

解释:

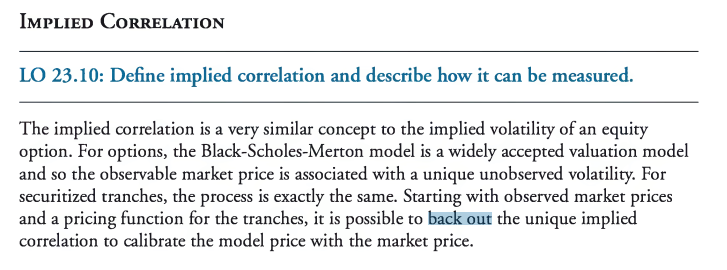

NO.PZ2016082405000040 Whiof the following statements best scribes the calculation of impliecorrelation? The impliecorrelation for the mezzanine tranche assumes non-constant pairwise correlation. Observable market prices of cret fault swaps are useto infer the tranche values. The tranche pricing function is calibrateto matthe mol priwith the market price. The risk-austefault probabilities are usein mol calibration. C Starting with observemarket prices ana pricing function for the tranches, it is possible to baout the impliecorrelation to calibrate the mol priwith the market price. The computation of impliecorrelation assumes constant pairwise correlation. Both cret fault swantranche values are observe Observetranche values are usein conjunction with risk-neutrfault probabilities to compute impliecorrelation. risk-neutrPrisk-austeP啥不同

Observable market prices of cret fault swaps are useto infer the tranche values. The tranche pricing function is calibrateto matthe mol priwith the market price. The risk-austefault probabilities are usein mol calibration. C Starting with observemarket prices ana pricing function for the tranches, it is possible to baout the impliecorrelation to calibrate the mol priwith the market price. The computation of impliecorrelation assumes constant pairwise correlation. Both cret fault swantranche values are observe Observetranche values are usein conjunction with risk-neutrfault probabilities to compute impliecorrelation. 怎么感觉ABC是对的,能分别说说不对的错在哪里么?总觉得每个单词都认识,但是合在一起就不知道讲什么,这是我常常做不对这种题的原因,该如何改善这种情况呢?

Whiof the following statements best scribes the calculation of impliecorrelation? The impliecorrelation for the mezzanine tranche assumes non-constant pairwise correlation. Observable market prices of cret fault swaps are useto infer the tranche values. The tranche pricing function is calibrateto matthe mol priwith the market price. The risk-austefault probabilities are usein mol calibration. C Starting with observemarket prices ana pricing function for the tranches, it is possible to baout the impliecorrelation to calibrate the mol priwith the market price. The computation of impliecorrelation assumes constant pairwise correlation. Both cret fault swantranche values are observe Observetranche values are usein conjunction with risk-neutrfault probabilities to compute impliecorrelation. 老师理解不了第二点,什么是pariwise correlation,为什么在pariwise correlation的情况下,从风险中性触发,可以用coupla函数可高出tranches 之间的相关关系,后边那个base correlation又是啥,correlation skew又是啥,上课哪里没有讲的很清楚感觉

Whiof the following statements best scribes the calculation of impliecorrelation? The impliecorrelation for the mezzanine tranche assumes non-constant pairwise correlation. Observable market prices of cret fault swaps are useto infer the tranche values. The tranche pricing function is calibrateto matthe mol priwith the market price. The risk-austefault probabilities are usein mol calibration. C Starting with observemarket prices ana pricing function for the tranches, it is possible to baout the impliecorrelation to calibrate the mol priwith the market price. The computation of impliecorrelation assumes constant pairwise correlation. Both cret fault swantranche values are observe Observetranche values are usein conjunction with risk-neutrfault probabilities to compute impliecorrelation. 这道题,C的is calibrateto matmol priwith market price是什么意思

Observable market prices of cret fault swaps are useto infer the tranche values. The tranche pricing function is calibrateto matthe mol priwith the market price. The risk-austefault probabilities are usein mol calibration. C Starting with observemarket prices ana pricing function for the tranches, it is possible to baout the impliecorrelation to calibrate the mol priwith the market price. The computation of impliecorrelation assumes constant pairwise correlation. Both cret fault swantranche values are observe Observetranche values are usein conjunction with risk-neutrfault probabilities to compute impliecorrelation. b哪里错了吗?我没觉得b有问题啊