请问为何我用E2的两个二叉树分别计算callable的V+/V-,却怎么样也算不出答案的数据是怎么回事呢?

问题如下图:

选项:

A.

B.

C.

发亮_品职助教 · 2019年02月26日

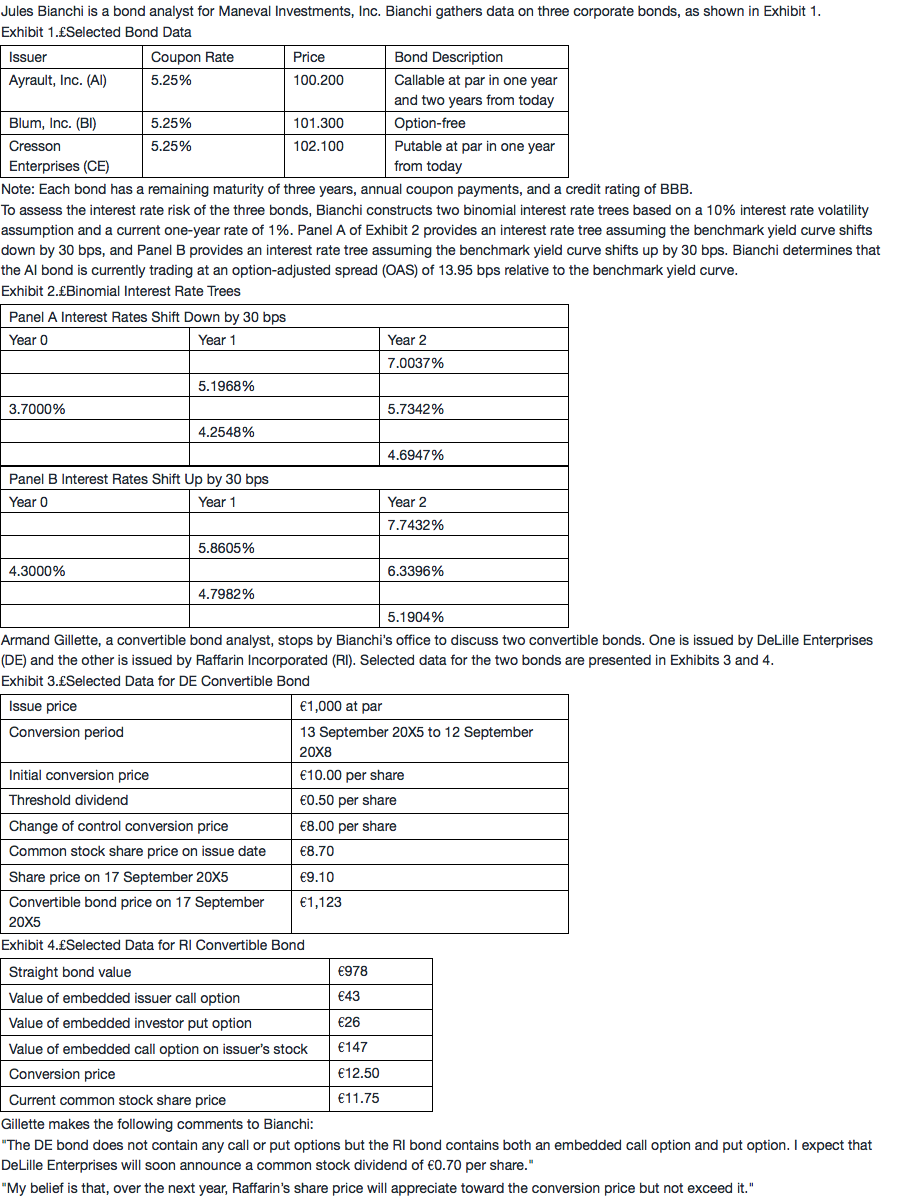

Exhibit 2给定的是benchmark的二叉树。

题干的信息是: Panel A of Exhibit 2 provides an interest rate tree assuming the benchmark yield curve shifts down by 30 bps, and Panel B provides an interest rate tree assuming the benchmark yield curve shifts up by 30 bps.

但注意这个AI bond还有一个OAS是13.95 bps,所以对AI bond的折现率,应该是Benchmark二叉树的基础上加上13.95 bps; 给二叉树所有的利率都加上13.95bps,然后用新的二叉树算callable bond的V+和V-。

NO.PZ201712110200000401 问题如下 Baseon Exhibits 1 an2, the effective ration for the bonis closest to: A.1.98. B.2.15. C.2.73. B is correct. The bons value if interest rates shift wn 30 bps (PV–) is 100.78. The bons value if interest rates shift up 30 bps (PV+) is 99.487.Effective ration=[(PV-)-(PV+)]/[2× (ΔCurve) × (PV0)]= (100.780 - 99.487)/ (2 × 0.003 × 100.200)=2.15 bons value if interest rates shift wn 30 bps (PV–) 我算的不是 100.78,而是101.03854,算了两次都是这样,请问我哪里出错了?

NO.PZ201712110200000401 问题如下 Baseon Exhibits 1 an2, the effective ration for the bonis closest to: A.1.98. B.2.15. C.2.73. B is correct. The bons value if interest rates shift wn 30 bps (PV–) is 100.78. The bons value if interest rates shift up 30 bps (PV+) is 99.487.Effective ration=[(PV-)-(PV+)]/[2× (ΔCurve) × (PV0)]= (100.780 - 99.487)/ (2 × 0.003 × 100.200)=2.15 老师您好,我看原教材解析里面都懒得写计算全过程了...... 一般考试中会出现这么繁琐的计算么

NO.PZ201712110200000401问题如下Baseon Exhibits 1 an2, the effective ration for the bonis closest to:A.1.98.B.2.15.C.2.73.B is correct. The bons value if interest rates shift wn 30 bps (PV–) is 100.78. The bons value if interest rates shift up 30 bps (PV+) is 99.487.Effective ration=[(PV-)-(PV+)]/[2× (ΔCurve) × (PV0)]= (100.780 - 99.487)/ (2 × 0.003 × 100.200)=2.15对于含权债券如何判断题目给的现金流是否含权,什么时候需要在分母加oas

NO.PZ201712110200000401 问题如下 Baseon Exhibits 1 an2, the effective ration for the bonis closest to: A.1.98. B.2.15. C.2.73. B is correct. The bons value if interest rates shift wn 30 bps (PV–) is 100.78. The bons value if interest rates shift up 30 bps (PV+) is 99.487.Effective ration=[(PV-)-(PV+)]/[2× (ΔCurve) × (PV0)]= (100.780 - 99.487)/ (2 × 0.003 × 100.200)=2.15 老师上课说过,OAS是剔除了权利影响的sprea分子的现金流已经包含了权利影响了。那为什么还可以在二叉树的利率上直接加OAS,但是现金流又还是按照初始的coupon rate来计算呢?

NO.PZ201712110200000401 问题如下 Baseon Exhibits 1 an2, the effective ration for the bonis closest to: A.1.98. B.2.15. C.2.73. B is correct. The bons value if interest rates shift wn 30 bps (PV–) is 100.78. The bons value if interest rates shift up 30 bps (PV+) is 99.487.Effective ration=[(PV-)-(PV+)]/[2× (ΔCurve) × (PV0)]= (100.780 - 99.487)/ (2 × 0.003 × 100.200)=2.15 例如上图是辅导老师的解题过程,V+在year2,既然折现率4.9377%小于coupon rate,作为callable,为什么不直接取100呢而是99.7114?