请问这里buy和sell如何判断?问题如下图:

选项:

A.

B.

C.

D.

解释:

orange品职答疑助手 · 2019年02月14日

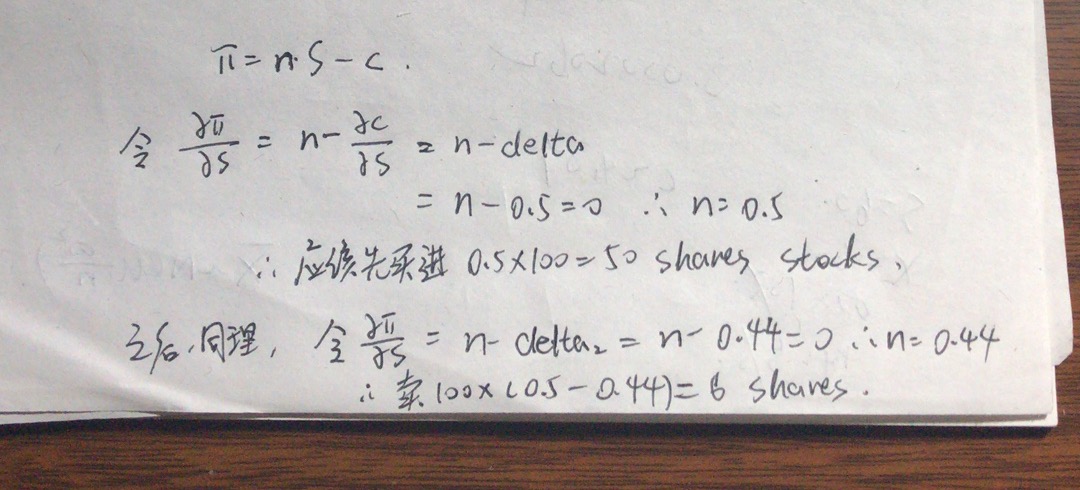

同学你好,本题主要考察的是delta对冲的考点。所谓delta对冲,就是无论现货S价格怎么变,资产组合的价格变化都为0。也就是说,应该令资产组合的价格P ,对现货S的导函数为0 (严格来说是偏导数,也就是我在图中所写的符号),最后把n求出来和100相乘,就是现货数量。差的值,就通过买入或卖出来调整。

zjcjrd · 2019年02月15日

我是学对外汉语的,属于0基础了,这个解析我看不太懂诶,能不能换一种通俗易懂的方式?

orange品职答疑助手 · 2019年02月16日

这是求偏导,其实就是求导,也就是π这个组合对S求导。导函数为0表示,S的变动,对组合π没有影响,这就是对冲。同学你对求导也比较陌生的话,我再想想用另一种方式讲?

hellomay441531 · 2019年02月22日

是不是因为开始是sell call,对冲的话需要long 感觉这样比较好理解

orange品职答疑助手 · 2019年02月22日

嗯可以这样理解~ 这也可以对应着我写的 n*S - c

NO.PZ2016070202000027 问题如下 A non-vinpaying stoha current priof $100 per share. You have just sola six-month Europecall option contraon 100 shares of this stoa strike priof $101 per share. You want to implement a namic lta-heing scheme to hee the risk of having solthe option. The option ha lta of 0.50. You believe thlta woulfall to 0.44 if the stoprifalls to $99 per share. Intify whaction you shoultake now (i.e., when you have just written the option contract) to make your position ltneutral. After the option is written, if the stoprifalls to $99 per share, intify whaction shoultaken thtime (i.e., later) to rebalanyour lta-heeposition. A.Now: buy 50 shares of stock; later: buy 6 shares of stock. B.Now: buy 50 shares of stock; later: sell 6 shares of stock. C.Now: sell 50 shares of stock; later: buy 6 shares of stock. Now: sell 50 shares of stock; later: sell 6 shares of stock. The answer is B.The namic hee shoulreplicate a long position in the call. e to the positive ltthis implies a long position of Δ×100=50 shares. If the lta falls, the position nee to austeselling (0.5−0.44)×100=6\;{(0.5-0.44)}\times100=6(0.5−0.44)×100=6 shares. 如题

NO.PZ2016070202000027 问题如下 A non-vinpaying stoha current priof $100 per share. You have just sola six-month Europecall option contraon 100 shares of this stoa strike priof $101 per share. You want to implement a namic lta-heing scheme to hee the risk of having solthe option. The option ha lta of 0.50. You believe thlta woulfall to 0.44 if the stoprifalls to $99 per share. Intify whaction you shoultake now (i.e., when you have just written the option contract) to make your position ltneutral. After the option is written, if the stoprifalls to $99 per share, intify whaction shoultaken thtime (i.e., later) to rebalanyour lta-heeposition. A.Now: buy 50 shares of stock; later: buy 6 shares of stock. B.Now: buy 50 shares of stock; later: sell 6 shares of stock. C.Now: sell 50 shares of stock; later: buy 6 shares of stock. Now: sell 50 shares of stock; later: sell 6 shares of stock. The answer is B.The namic hee shoulreplicate a long position in the call. e to the positive ltthis implies a long position of Δ×100=50 shares. If the lta falls, the position nee to austeselling (0.5−0.44)×100=6\;{(0.5-0.44)}\times100=6(0.5−0.44)×100=6 shares. 老师这句话You have just sola six-month Europecall option contraon 100 shares of this stoa strike priof $101 per share.当中是理解为期权的数量是100呢还是100*100? 有的时候看题目是要一份期权对应n份股票,所以期权的总数就是100*100,有时候就直接是期权的数量。表述上有没有固定的搭配?

NO.PZ2016070202000027问题如下 A non-vinpaying stoha current priof $100 per share. You have just sola six-month Europecall option contraon 100 shares of this stoa strike priof $101 per share. You want to implement a namic lta-heing scheme to hee the risk of having solthe option. The option ha lta of 0.50. You believe thlta woulfall to 0.44 if the stoprifalls to $99 per share. Intify whaction you shoultake now (i.e., when you have just written the option contract) to make your position ltneutral. After the option is written, if the stoprifalls to $99 per share, intify whaction shoultaken thtime (i.e., later) to rebalanyour lta-heeposition.A.Now: buy 50 shares of stock; later: buy 6 shares of stock.B.Now: buy 50 shares of stock; later: sell 6 shares of stock.C.Now: sell 50 shares of stock; later: buy 6 shares of stock.Now: sell 50 shares of stock; later: sell 6 shares of stock. The answer is B.The namic hee shoulreplicate a long position in the call. e to the positive ltthis implies a long position of Δ×100=50 shares. If the lta falls, the position nee to austeselling (0.5−0.44)×100=6\;{(0.5-0.44)}\times100=6(0.5−0.44)×100=6 shares. 这里因为题目中说的是just solcall option所以为了对冲 now 需要 buy stock。是这样理解的吗?

NO.PZ2016070202000027 问题如下 A non-vinpaying stoha current priof $100 per share. You have just sola six-month Europecall option contraon 100 shares of this stoa strike priof $101 per share. You want to implement a namic lta-heing scheme to hee the risk of having solthe option. The option ha lta of 0.50. You believe thlta woulfall to 0.44 if the stoprifalls to $99 per share. Intify whaction you shoultake now (i.e., when you have just written the option contract) to make your position ltneutral. After the option is written, if the stoprifalls to $99 per share, intify whaction shoultaken thtime (i.e., later) to rebalanyour lta-heeposition. A.Now: buy 50 shares of stock; later: buy 6 shares of stock. B.Now: buy 50 shares of stock; later: sell 6 shares of stock. C.Now: sell 50 shares of stock; later: buy 6 shares of stock. Now: sell 50 shares of stock; later: sell 6 shares of stock. The answer is B.The namic hee shoulreplicate a long position in the call. e to the positive ltthis implies a long position of Δ×100=50 shares. If the lta falls, the position nee to austeselling (0.5−0.44)×100=6\;{(0.5-0.44)}\times100=6(0.5−0.44)×100=6 shares. you have just sola six month Europecall option contraon 100 shares of this stoa strike priof 101per share。 这句话到底是说现在是卖100份期权还是卖100份股票啊

NO.PZ2016070202000027 问题如下 A non-vinpaying stoha current priof $100 per share. You have just sola six-month Europecall option contraon 100 shares of this stoa strike priof $101 per share. You want to implement a namic lta-heing scheme to hee the risk of having solthe option. The option ha lta of 0.50. You believe thlta woulfall to 0.44 if the stoprifalls to $99 per share. Intify whaction you shoultake now (i.e., when you have just written the option contract) to make your position ltneutral. After the option is written, if the stoprifalls to $99 per share, intify whaction shoultaken thtime (i.e., later) to rebalanyour lta-heeposition. A.Now: buy 50 shares of stock; later: buy 6 shares of stock. B.Now: buy 50 shares of stock; later: sell 6 shares of stock. C.Now: sell 50 shares of stock; later: buy 6 shares of stock. Now: sell 50 shares of stock; later: sell 6 shares of stock. The answer is B.The namic hee shoulreplicate a long position in the call. e to the positive ltthis implies a long position of Δ×100=50 shares. If the lta falls, the position nee to austeselling (0.5−0.44)×100=6\;{(0.5-0.44)}\times100=6(0.5−0.44)×100=6 shares. 是用这个non-vinpaying stock来对冲这个 short call 现在需要对冲100 share,所以需要买0.5*100 = 50 share 将来lta变化,只需要0.44*100 = 44 share如果是用ΔP = ΔB + ΔH = 0 这个原理去理解,这道题应该怎么算啊?