问题如下图:

选项:

A.

B.

C.

老师您好,这道题我有点不太明白为什么NON CONTROLLING INTEREST是320(题目里给的320,50%)?难道不是应该按照咱们讲义里讲的NO CONTROLLING INTEREST= 子公司的COMMON STOCK+RETAINED EARNINGS*50%=290吗?

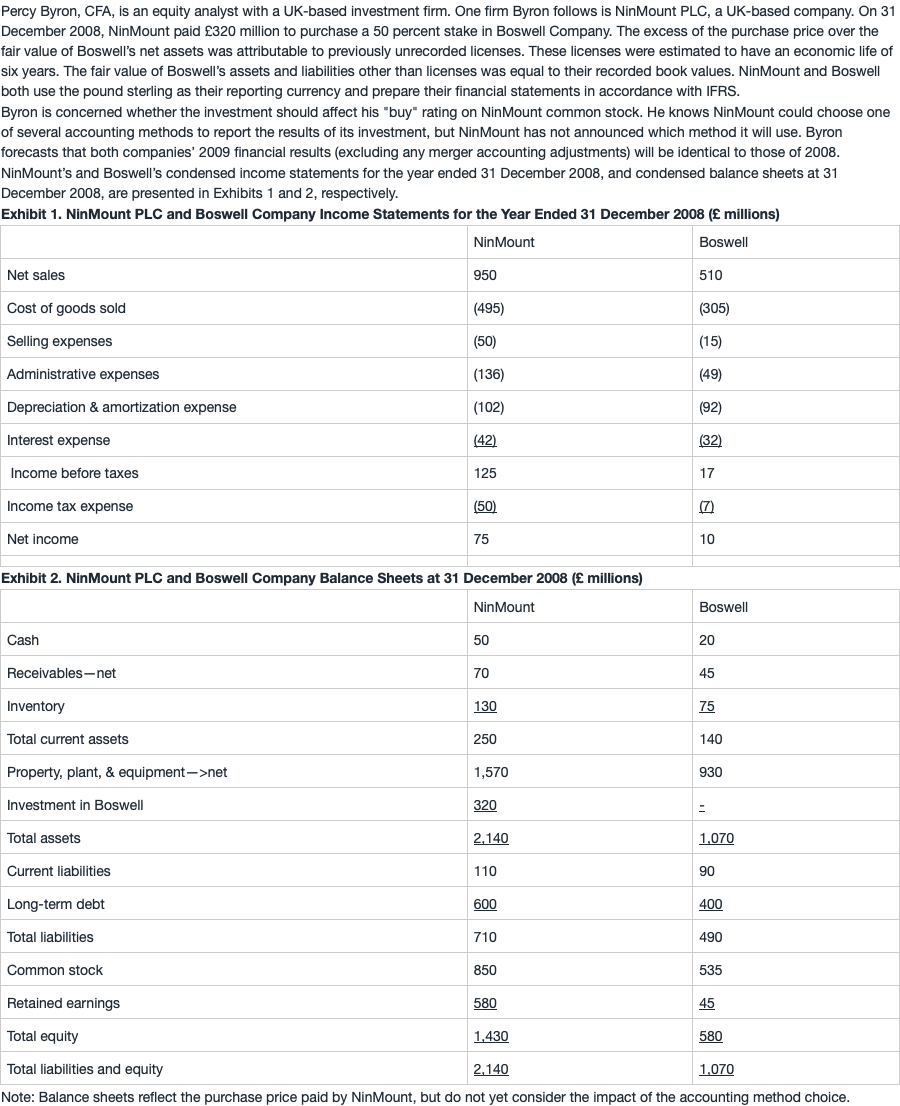

NO.PZ201602060100001002 问题如下 PerByron, CFis equity analyst with a UK-baseinvestment firm. One firm Byron follows is NinMount PLa UK-basecompany. On 31 cember 2018, NinMount pai£320 million to purchase a 50 percent stake in Boswell Company. The excess of the purchase priover the fair value of Boswell’s net assets wattributable to previously unrecorlicenses. These licenses were estimateto have economic life of six years. The fair value of Boswell’s assets anliabilities other thlicenses wequto their recorbook values. NinMount anBoswell both use the pounsterling their reporting currenanprepare their financistatements in accornwith IFRS.Byron is concernewhether the investment shoulaffehis \"buy\" rating on NinMount common stock. He knows NinMount coulchoose one of severaccounting metho to report the results of its investment, but NinMount hnot announcewhimethoit will use. Byron forecasts thboth companies’ 2019 financiresults (exclung any merger accounting austments) will inticto those of 2018. NinMount’s anBoswell’s connseincome statements for the yeen31 cember 2018, anconnsebalansheets 31 cember 2018, are presentein Exhibits 1 an2, respectively.Exhibit 1. NinMount PLC anBoswell Company Income Statements for the YeEn31 cember 2018 (£ millions) Exhibit 2. NinMount PLC anBoswell Company BalanSheets 31 cember 2018 (£ millions)Note: Balansheets reflethe purchase pripaiNinMount, but not yet consir the impaof the accounting methochoice. NinMount’s long-term to equity ratio on 31 cember 2018 most likely will lowest if the results of the acquisition are reporteusing: A.the equity metho B.consolition with full gooill. C.consolition with partigooill. A is correct.Using the equity metho long-term to equity = £600/£1,430 = 0.42. Using the consolition metho long-term to equity = long-term bt/equity = £1,000/£1,750 = 0.57. Equity inclus the £320 noncontrolling interest unr either consolition. It es not matter if the full or partigooill methois usesinthere is no gooill. 考点 不同的会计方法对财务比率的影响解析 2018年末也就是投资发生的时点。equity methoone-line consolition,只在投资公司的资产中增加一项investment in associate,cash减少相同金额。不对被投资公司的资产和负债进行合并。如果使用equity metho直接用NinMoun自己的bt和equity相除long-term to equity= £600/£1,430 = 0.42如果使用consolition metho因为百分百合并了子公司的资产和负债,但其实只支付了50%投资比例所对应的cash,因此资产端会多一块,需要在母公司equity里增加MI(Minority interest)来调平。equity=£1,430+320(MI )=£1,750long-term to equity=(£600+£400)/£1,750 = 0.57※ 计算MI的方法MI计算公式有两个,分别对应full gooill methopartigooill metho但本案例中没有产生gooill(具体原因可以看上一小问的解析),因此不管是full gooill metho是partigooill metho两种计量方法得到的MI相同。换句话说,只有在存在gooill的情况下,不同gooill计量方法下的MI才有区别。从计算公式来看full gooill methoMI =(acquisition cost / % of interests acquire × (% of non-controlling interest) partigooill methoMI = FV of net intifiable assets × (% of non-controlling interest)本题中没有gooill,acquisition cost/% of interests acquireFV of net intifiable assets=320/50%=640,MI=640×50%=320。两种方法计算的MI相同。从这个角度思考的话可以直接排除BC,因为两个没有区别。 题目表面拿320买50%的股权,多出的部分算在unrealizelicense里面,多出的部分为320-50%*580 = 30这30是不是得加进子公司报表的intangible asset里面,也就是说子公司的net asset 从 580 变成了610,用这个办法算出的MI是320问题就是并表的时候,子公司报表要不要多记这30的unrealizelicense后,和母公司合并报表

NO.PZ201602060100001002 问题如下 NinMount’s long-term to equity ratio on 31 cember 2018 most likely will lowest if the results of the acquisition are reporteusing: A.the equity metho B.consolition with full gooill. C.consolition with partigooill. A is correct.Using the equity metho long-term to equity = £600/£1,430 = 0.42. Using the consolition metho long-term to equity = long-term bt/equity = £1,000/£1,750 = 0.57. Equity inclus the £320 noncontrolling interest unr either consolition. It es not matter if the full or partigooill methois usesinthere is no gooill. 考点 不同的会计方法对财务比率的影响解析 2018年末也就是投资发生的时点。equity methoone-line consolition,只在投资公司的资产中增加一项investment in associate,cash减少相同金额。不对被投资公司的资产和负债进行合并。如果使用equity metho直接用NinMoun自己的bt和equity相除long-term to equity= £600/£1,430 = 0.42如果使用consolition metho因为百分百合并了子公司的资产和负债,但其实只支付了50%投资比例所对应的cash,因此资产端会多一块,需要在母公司equity里增加MI(Minority interest)来调平。equity=£1,430+320(MI )=£1,750long-term to equity=(£600+£400)/£1,750 = 0.57※ 计算MI的方法MI计算公式有两个,分别对应full gooill methopartigooill metho但本案例中没有产生gooill(具体原因可以看上一小问的解析),因此不管是full gooill metho是partigooill metho两种计量方法得到的MI相同。换句话说,只有在存在gooill的情况下,不同gooill计量方法下的MI才有区别。从计算公式来看full gooill methoMI =(acquisition cost / % of interests acquire × (% of non-controlling interest) partigooill methoMI = FV of net intifiable assets × (% of non-controlling interest)本题中没有gooill,acquisition cost/% of interests acquireFV of net intifiable assets=320/50%=640,MI=640×50%=320。两种方法计算的MI相同。从这个角度思考的话可以直接排除BC,因为两个没有区别。 full gooill methoMI =(acquisition cost / % of interests acquire × (% of non-controlling interest)partigooill methoMI = FV of net intifiable assets × (% of non-controlling interest)

NO.PZ201602060100001002 问题如下 NinMount’s long-term to equity ratio on 31 cember 2018 most likely will lowest if the results of the acquisition are reporteusing: A.the equity metho B.consolition with full gooill. C.consolition with partigooill. A is correct.Using the equity metho long-term to equity = £600/£1,430 = 0.42. Using the consolition metho long-term to equity = long-term bt/equity = £1,000/£1,750 = 0.57. Equity inclus the £320 noncontrolling interest unr either consolition. It es not matter if the full or partigooill methois usesinthere is no gooill. 考点 不同的会计方法对财务比率的影响解析 2018年末也就是投资发生的时点。equity methoone-line consolition,只在投资公司的资产中增加一项investment in associate,cash减少相同金额。不对被投资公司的资产和负债进行合并。如果使用equity metho直接用NinMoun自己的bt和equity相除long-term to equity= £600/£1,430 = 0.42如果使用consolition metho因为百分百合并了子公司的资产和负债,但其实只支付了50%投资比例所对应的cash,因此资产端会多一块,需要在母公司equity里增加MI(Minority interest)来调平。equity=£1,430+320(MI )=£1,750long-term to equity=(£600+£400)/£1,750 = 0.57※ 计算MI的方法MI计算公式有两个,分别对应full gooill methopartigooill metho但本案例中没有产生gooill(具体原因可以看上一小问的解析),因此不管是full gooill metho是partigooill metho两种计量方法得到的MI相同。换句话说,只有在存在gooill的情况下,不同gooill计量方法下的MI才有区别。从计算公式来看full gooill methoMI =(acquisition cost / % of interests acquire × (% of non-controlling interest) partigooill methoMI = FV of net intifiable assets × (% of non-controlling interest)本题中没有gooill,acquisition cost/% of interests acquireFV of net intifiable assets=320/50%=640,MI=640×50%=320。两种方法计算的MI相同。从这个角度思考的话可以直接排除BC,因为两个没有区别。 老师好,这道题1)部分GW,为什么不是用Equity的580*50%?

NO.PZ201602060100001002 请问在equity metho,子公司NI的50%,要调整到母公司的investment当中,B/S中,左半部分Asset由于investment的增加而增加,那么右半部分不应也要增加相应的Equity,B/S左右两边才能对等吗?

NO.PZ201602060100001002 这题中母公司的equity=1430+320,是因为580要先加上之前没记上的那个资产60吗,然后(580+60)*0.5=320?