NO.PZ2018123101000058

问题如下:

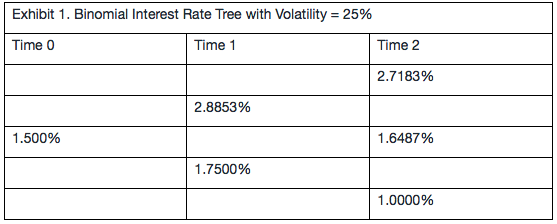

To value Bond C using the binomial tree in Exhibit 1. Exhibit 2 presents selected data for both bonds.

Based on Exhibits 1 and 2, the value of Bond C at the upper node at Time 1 is closest to:

选项:

A.97.1957.

B.99.6255.

C.102.1255.

解释:

B is correct.

考点:利用二叉树对债券进行定价

解析:

第二年年末债券的现金流为:102.5(100的本金+2.5的Coupon)

要计算第一年时间点,上面节点的债券价值,因此使用的是1-year forward rate是2.8853%;有公式 :

老师,这道题我看了以前解析还是没太明白,为什么算Node1时候不用从time2 两个值 * 50% ,折回到Node1;

而如果算time 0时候,就需要从time1 两个值*50%,算出?

那如果算Node2 upper时,和Node 1 upper 一样是么?直接102.5/ (1+2.7183%)?