NO.PZ2025022502000014

问题如下:

The carbon risk premium is best described as a:

选项:

A.higher price consumers pay for carbon-neutral products.

B.higher return required for investments in high-carbon companies.

C.discount applied to risky company cash flows when valuing green bonds.

解释:

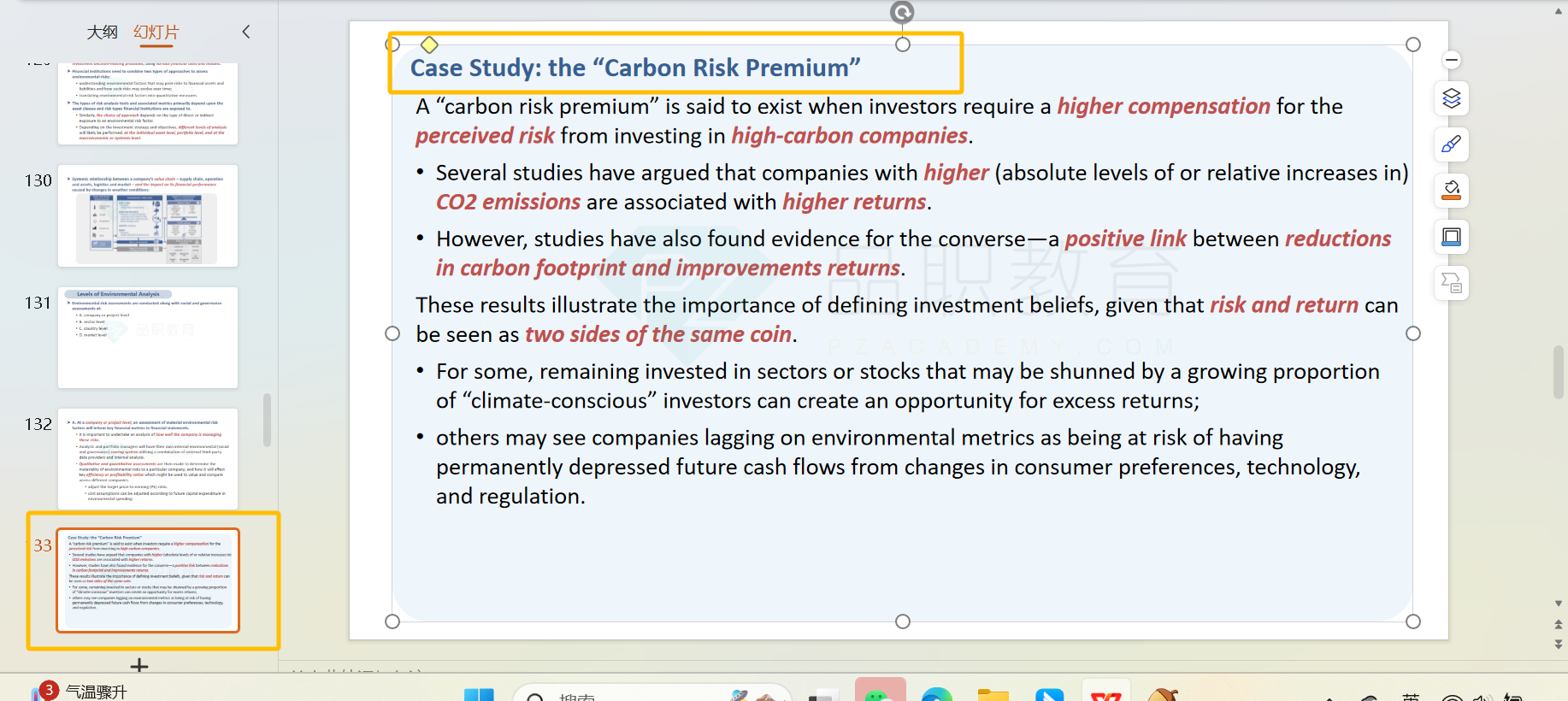

B is correct because a carbon risk premium is said to exist when investors require a higher compensation for the perceived risk from investing in high-carbon companies. Several studies have argued that companies with higher (absolute levels of or relative increases in) CO2 emissions are associated with higher returns; however, studies have also found evidence for the converse—a positive link between reductions in carbon footprint and improvements returns.可以再解释一下A和C吗 没理解