NO.PZ2024010508000012

问题如下:

Which of the following considers ESG risk as a bottom-up risk factor for ESG integration in strategic asset allocation?

选项:

A.Factor risk allocation

B.Total portfolio analysis

C.Dynamic asset allocation

解释:

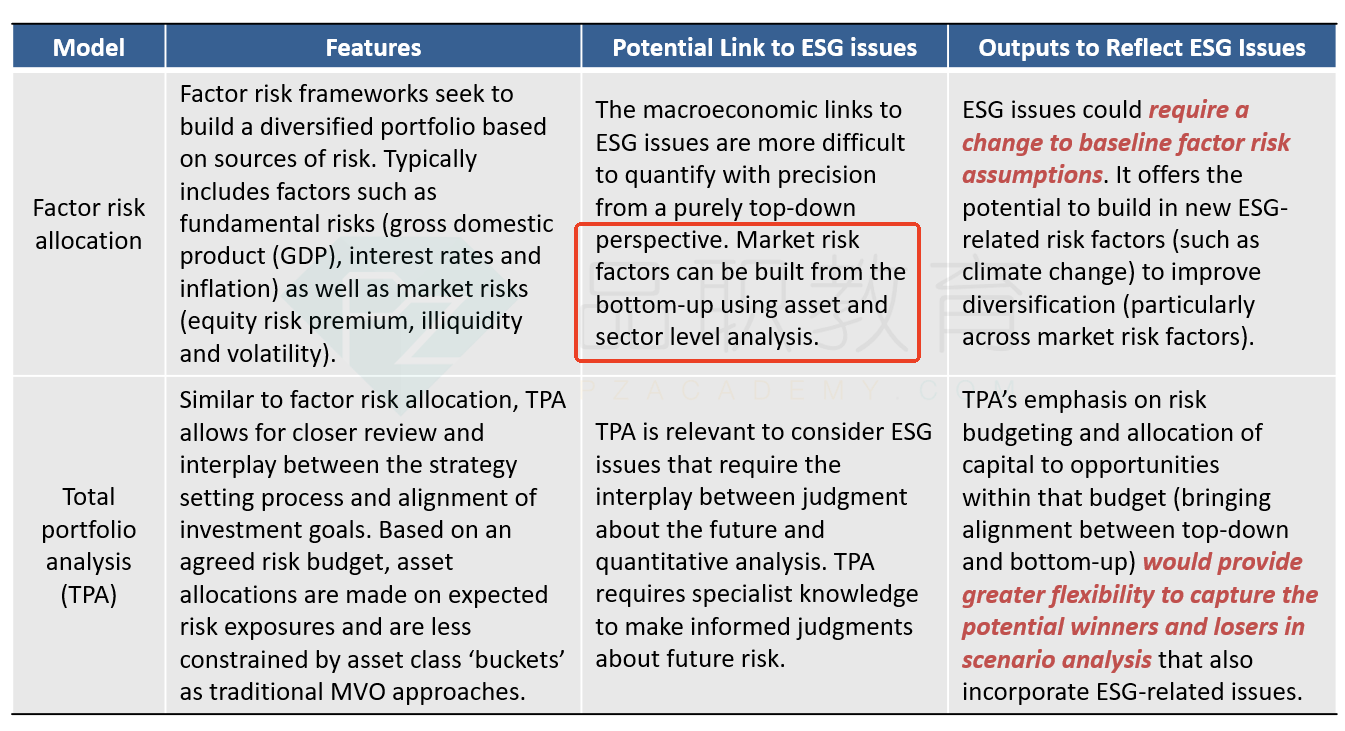

A is correct. If the investor believes that ESG risk primarily resides at the underlying security-selection level, then ESG integration at that level is sensible. But if the investor believes that ESG risk represents a more top-down risk factor affecting most or all securities—which may be the case with climate change—then it may better serve the investor to integrate ESG analysis at the asset allocation level. The macroeconomic links to ESG issues are more difficult to quantify with precision from a purely top-down perspective. Market risk factors can be built from the bottom up using asset- and sector-level analysis under the factor risk allocation model.讲义哪里提到这个知识点呀?