31:29 (1X)

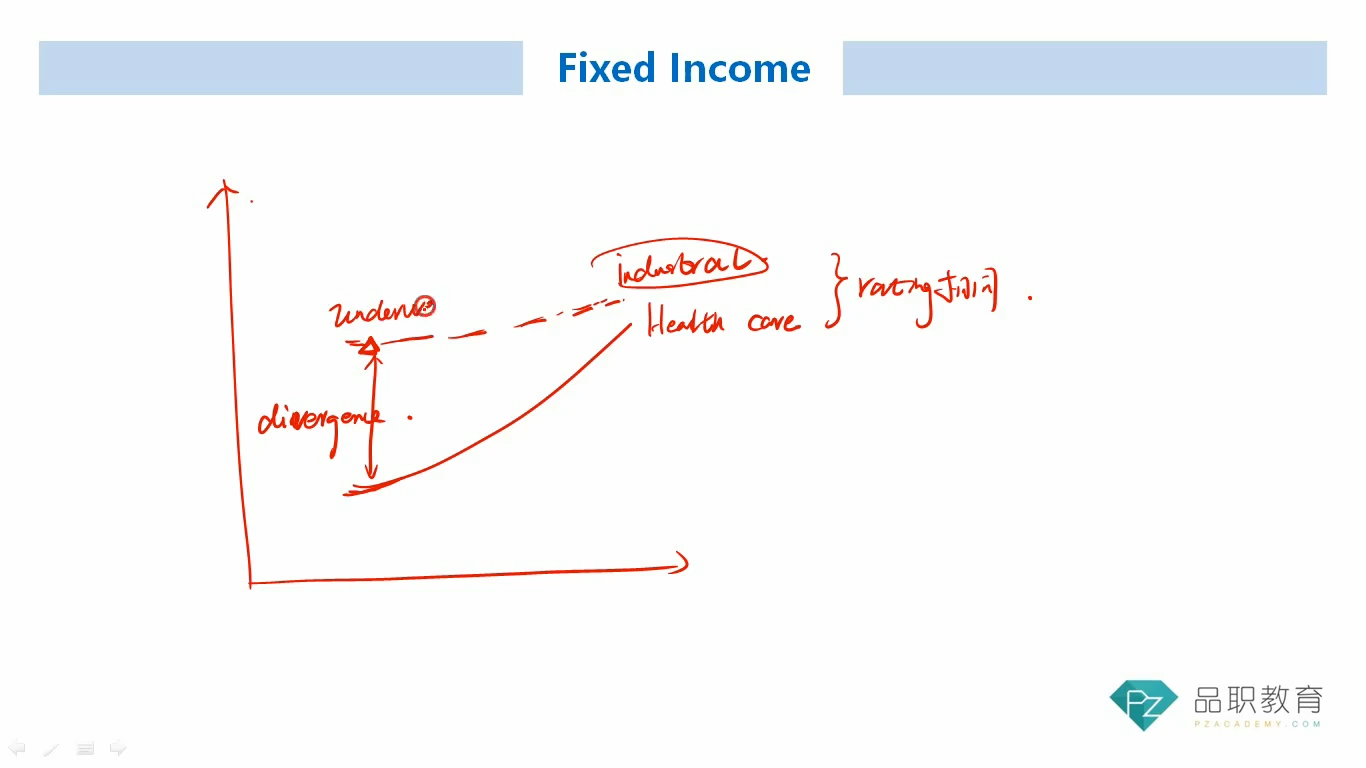

为什么spread高的sector反而underweight?

发亮_品职助教 · 2025年06月18日

分析的时间点不一样。这块何老师的视频没有把前提条件区分开,有点歧义。

原本讲义是说,要基于对未来spread的改变预期做策略。E.g.,expects the credit curve will flatten or steepen, or two spread curves will converge or diverge

所以是这里的diverge还未发生。预测将来will diverge,即industrial的spread将来上升,那么我们提前做好underweight。同理health care的spread将来下降,我们提前做好overweight。

当然如果diverge已经发生了,我们会预测将来他们会趋同converge,即industrial的spread将来下降,我们提前做好overweight;同理health care的spread将来上升,提前做好underweight。

总之是基于未来的变动方向做策略。视频这块的背景是说diverge还未发生,是预测将要发生。