NO.PZ2019070101000009

问题如下:

When measuring the risk of non-linear derivatives, which of the following statements is incorrect?

选项:

A.

The delta-gamma approach is used.

B.

An advantage of the local valuation approach is that it is simple and easy to implement.

C.

A disdvantage of the local valuation approach is that it needs to assume a normal distribution.

D.

The full revaluation approach is perferred for calulating the risk of mortgage-backed securities.

解释:

D is correct.

考点:Measure the Risk for Non-Linear Derivatives

解析: 这道题是选出说法错误的选项。 对于non-linear derivatives,我们主要采用的方法是delta-gamma approach,A选项说法正确。 local valuation approach 因为采用了近似的方法,所以比较简单也容易实施,B选项说法正确。local valuation approach由一个正态分布的假设,这是它最大的缺点,C说法正确。由于MBS的价格结构比较复杂,因此不适合用full valuation aproach。D选项说法错误,所以选D。

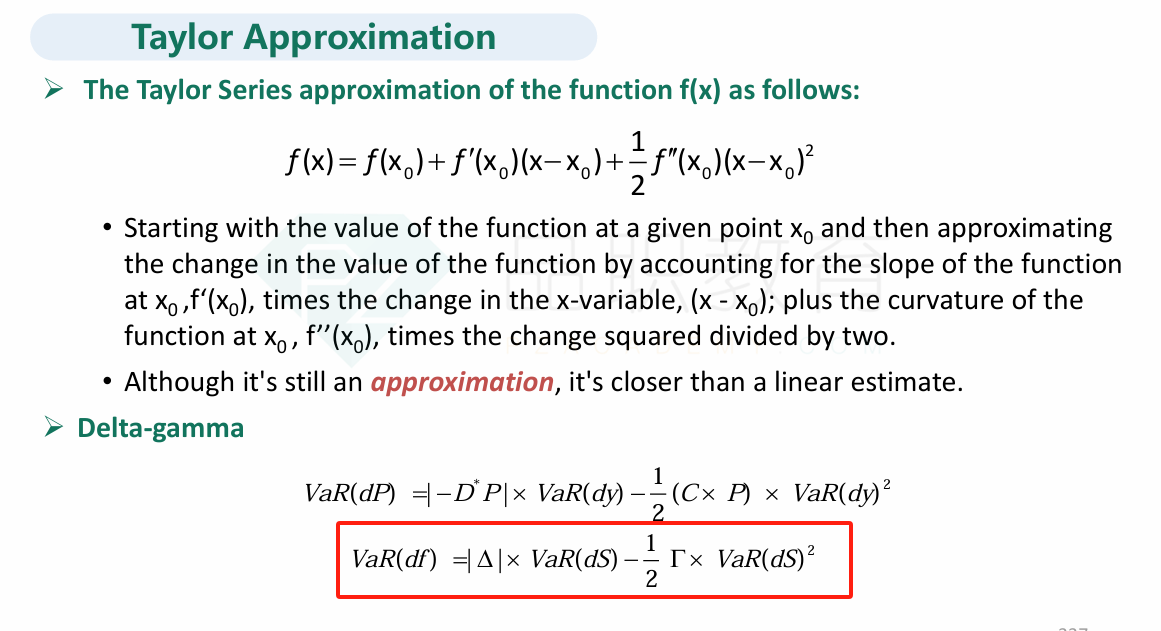

细讲一下delta gamma approach