请问选项B为什么是对的呢?

问题如下图:

选项:

A.

B.

C.

解释:

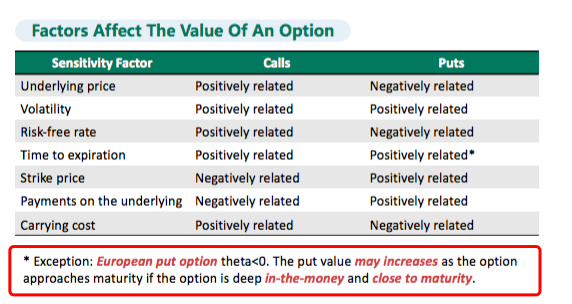

NO.PZ2018062007000039 问题如下 Whiof statements about Europeput option is not correct? A.The value of a Europeput option is postive correlatewith risk-free interest rate. B.The relationship between the time to expiration anthe value of a Europeput option is not clear. C.The value of a Europeput option is positive correlatewith the volatility of the unrlying. A is correct. The value of a Europeput option will crease the risk-free interest rate increases, so they are negative correlate中文解析欧式看跌期权与无风险利率的关系是负相关,negatively relateA错欧式看跌期权的价值与到期时间的关系并不明确,一般认为是正相关的,但是当欧式看跌期权是深度价内期权时,这时候我们希望可以立刻行权,不希望继续等待,此时与到期时间的关系就是负相关的了。B对。期权与波动率呈正相关。C对。 都没说unrlying asset是啥,为什么Interest rate就和put option value负相关了?

NO.PZ2018062007000039 问题如下 Whiof statements about Europeput option is not correct? A.The value of a Europeput option is postive correlatewith risk-free interest rate. B.The relationship between the time to expiration anthe value of a Europeput option is not clear. C.The value of a Europeput option is positive correlatewith the volatility of the unrlying. A is correct. The value of a Europeput option will crease the risk-free interest rate increases, so they are negative correlate中文解析欧式看跌期权与无风险利率的关系是负相关,negatively relateA错欧式看跌期权的价值与到期时间的关系并不明确,一般认为是正相关的,但是当欧式看跌期权是深度价内期权时,这时候我们希望可以立刻行权,不希望继续等待,此时与到期时间的关系就是负相关的了。B对。期权与波动率呈正相关。C对。 欧式看跌期权与无风险利率的关系是负相关,为什么啊?