05:58 (1.3X)

rolling down策略是maturity>investment horizon,buy-and-hold策略是maturity=investment horizon。那么感觉选项A是rolling down策略?

发亮_品职助教 · 2025年05月27日

也可以理解成roll down strategy,不影响这道题的分析。

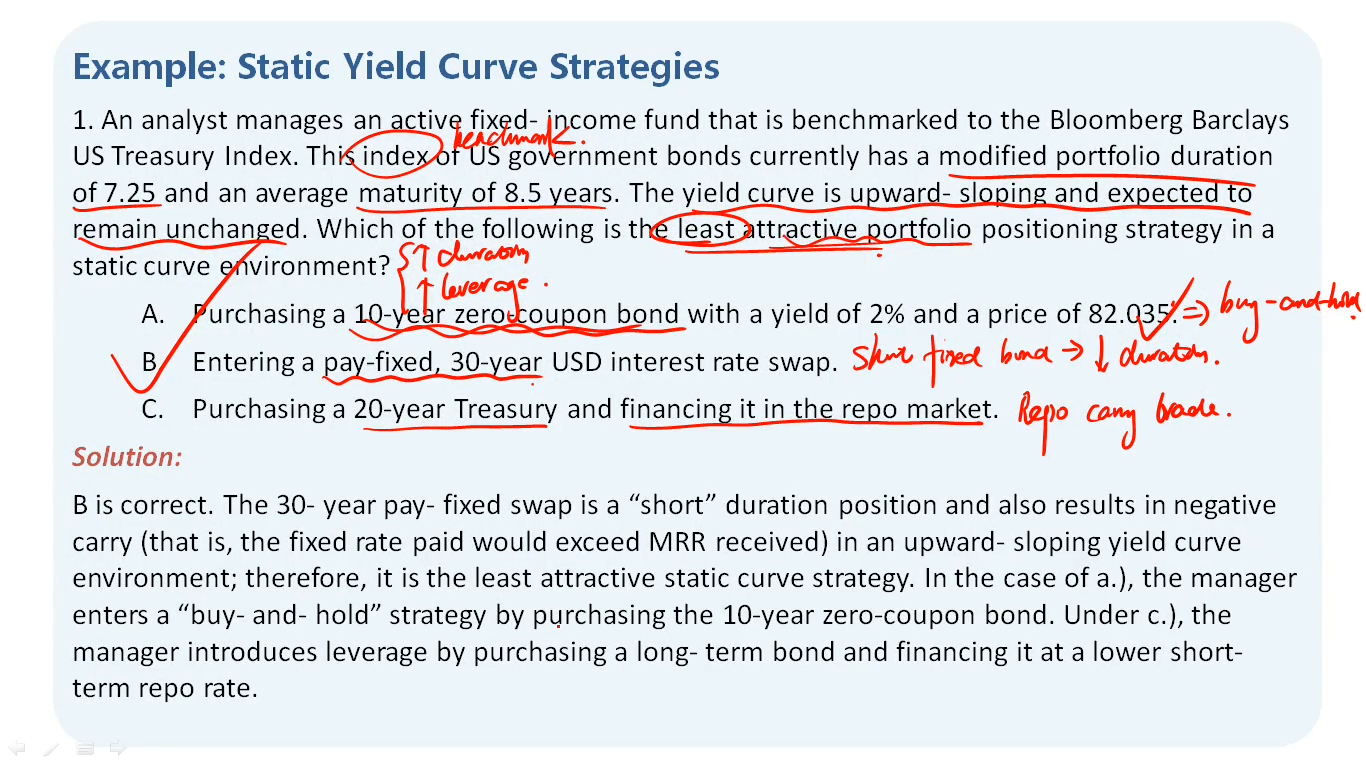

在stable yield curve下,策略的核心理念是2个,extend duration与increase leverage。

其中extend duration理念下,具体的策略有Buy-and-hold与roll down strategy。

这个extend duration里面的duration可以理解成债券期限。即,买入更长期的债券。

因为利率曲线stable且upward sloping,所以长期债券的收益率更大,我们可以人为延长投资期,如把原来7-year investment horizon延长至10-year investment horizon,现在做10年期债券的buy-and-hold增加组合收益。

第二个roll down strategy,在投资期不变的背景下,依然保持原来7年期的投资期,但买入更长期的债券如10年期,赚roll down stratetgy的收益。

这道题的A选项不管从哪个策略分析,都会使得组合会持有更长期的债券,本质都是extend duration,符合stable yield curve的策略核心理念。